{kind=link}

Canadian Dollar makes a massive strike back as boosted by very strong inflation reading. The Loonie is now trading as the biggest gainer for today. While Yen’s no.1 place is taken, it’s staying the second strongest as supported by risk aversion. Dollar is trading as the weakest one for today, but it’s holding above yesterday’s low against all but Yen and Canadian. Sterling follows as the second weakest one.

At the time of writing, FTSE is down -0.47%, DAX down -0.80% and CAC is down -0.54%. Turkish Lira is back in the spotlight on worries of further US sanction, if American pastor Andrew Brunson is not released. Also, S&P Global Ratings is set to announce a review on Turkey and another downgrade looks inevitable. USD/TRY hit as high as 6.3467 earlier today and it’s now up more than 4.5% at 6.1040.

Weakness in Chinese stocks is another source of concerns for investors. Asian markets closed generally up today. Nikkei gained 0.35%, Hong Kong HSI rose 0.42%. However, the Shanghai SSE closed down -1.35% at 2668.97. The SSE has indeed broke July’s low at 2691.02, and it’s on course for 2638.30 (2016 low). More importantly, the selloff happened despite news of resumption of US-China trade talks. This highlights underlying vulnerable in the Chinese stocks markets. A break of 2638.30 could trigger some downside acceleration and spread to other parts markets, at least to Asia.

Canada CPI surges to 3.0% in July, a big step to October BoC hike

Canadian consumer inflation data comes in much stronger than expected. Headline CPI rose 0.5% mom, 3.0% yoy versus expectation of -0.1% mom, 2.4% yoy. It’s also much stronger than June’s reading of 0.1% mom, 2.5% yoy. CPI core Common was unchanged at 1.9% yoy. CPI core Median was unchanged at 2.0% yoy. CPI core Trim rose to 2.1% yoy, up from 2.0% yoy.

“While continued strength in energy prices contributed most to the year-over-year increase, higher prices for various services, including air transportation and travel tours, also contributed to consumer price growth in July,” Statistics Canada said.

The strong inflation reading certainly pushes BoC a big step closer to an October rate hike.

Also from Canada, international securities transactions rose to CAD 11.5B in June versus expectation of CAD 4.9B.

Eurozone CPI finalized at 2.1%, core CPI at 1.1%

Eurozone CPI was finalized at 2.1% in July, up from June’s 2.0% and compares with 1.3% a year earlier. EU CPI was finalized at 2.2% in July, up from June’s 2.1%, compares with 1.5% a year earlier. Core CPI was finalized at 1.1%.

Geographically, CPI ranged from 0.8% in Greece, 0.9% in Denmark and 1.0% in Ireland, to Romania (4.3%), Bulgaria (3.6%), Hungary (3.4%) and Estonia (3.3%). CPI in Germany was at 2.1%, France at 2.6% and Italy at 1.9%. Composition-wise, highest contribution came from energy at 0.89%, services at 0.64%, food alcohol and tobacco at 0.49%.

Also from Eurozone, current account surplus narrowed to EUR 23.5B in June, below expectation of EUR 23.2B.

Australia Trade Minister Ciobo: Countries double down on trade pacts due to protectionist Trump

Australia’s Trade Minister Steven Ciobo said today that the country is going to conclude free trade agreement with Hong Kong and Indonesia by the end of the year. Hong Kong is Australia’s 12th largest trading partner with two-way trade at roughly AUD 16B. The two-way trade with Indonesia is at roughly the same size. And indeed, the FTA with Indonesia could come as soon as next month during Prime Minister Malcolm Turnbull’s visit.

Ciobo also said that he’s hopeful of signing FTA with Pacific Alliance, a Latin American trade bloc, this year. In addition, agreement with China-led Regional Comprehensive Economic Partnership could be in place too.

Ciobo added that due to Trump’s protectionist rhetoric and policies, there has been a “desire from a number of countries to double down” on trade pacts. And that helps him seal deals.

RBA Lowe warned of trade tension and highly unusual US fiscal stimulus

RBA Governor Philip Lowe appeared before the House of Representatives Standing Committee on Economics today. He reiterated the three points in communications about monetary policy. Firstly, employment and inflation are “moving in the right direction”. Secondly, the next move is interest rates is “to be up”. Thirdly, progresses is expected to be “gradual” and there is “not a strong case for near term adjustment in interest rates.

Lowe also highlighted a few global risks. Firstly, in some countries, businesses are delaying investment due to rising trade tensions. If it become a “more general story”, it’s the channel through which trade tensions would “sap the current positive momentum” in the global economy.

Secondly, it’s “highly unusual” for the US to have “sizeable fiscal stimulus” at a time of “limited capacity”. Growth could “surprise on the upside. And Lowe is “less relaxed” than others on the implications on inflation. He warned that Fed could have to withdraw monetary accommodation “more quickly than currently projected”with possibly disruptive consequences in financial markets.

A third set of global risks are from individual economies with “country-specific structural and/or institutional vulnerabilities”, including Argentina, Brazil, Italy and Turkey.

Japan manufacturers sentiment hit 7-month high, but non-manufacturing at 1.5 year low

Reuters Tankan manufacturers index rose to 30 in August, up from 25. However, the non-manufacturers index dropped sharply to 25, down from 34.

With the sharp 5 pts rise in index, manufacturer’s sentiment, hit the highest level since January. Back then it was an 11-year high of 35. The index is expected to improve further in the new few months. It highlights the robustness of the manufacturing sector despite rising global trade tension and emerging markets risks.

On the other hand, services sentiments tumbled sharply by -9 to the lowest level since December 2016. It’s partly due to once-off factors including abnormal whether including flood rains and heat waves. But the deterioration still indicates fragility in the sector and thus casts doubt on domestic demand. Domestic weakness could amply should there be deterioration in global trade tensions.

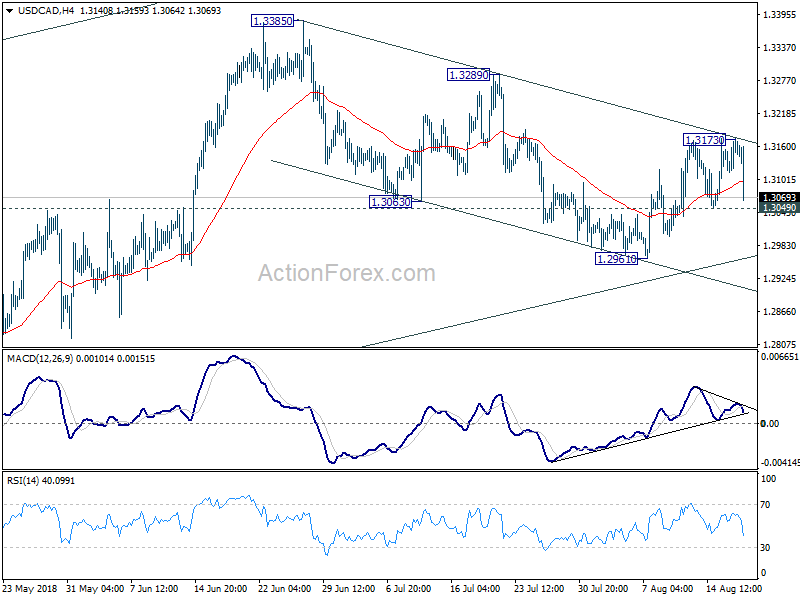

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3123; (P) 1.3149; (R1) 1.3185; More…

UD/CAD was rejected by near term falling channel resistance and drops sharply in early US session. Nonetheless, it’s staying above 1.3049 minor support and intraday bias remains neutral. While the view is looking shaky, we’re still favoring that corrective pull back from 1.3385 has completed at 1.2916. Rebound from 1.2961 should extend higher and above 1.3173 will target 1.3289 resistance. However, on the downside, break of 1.3049 minor support will dampen this bullish view and turn focus back to 1.2961 low instead.

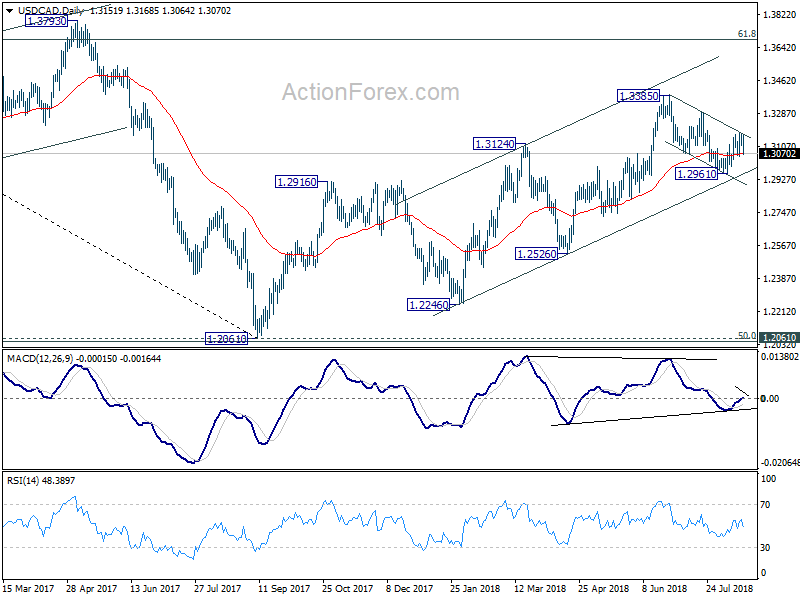

In the bigger picture, as long as channel support (now at 1.2958) holds, we’re holding to the bullish view. That is, fall from 1.4689 (2015 high) has completed at 1.2061, ahead of 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen for 61.8% retracement of 1.4689 to 1.2061 at 1.3685 and above. However, sustained break of the channel support will argue that rise from 1.2061 has completed and will bring deeper fall to 1.2526 support to confirm.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | PPI Input Q/Q Q2 | 1.00% | 0.20% | 0.60% | |

| 22:45 | NZD | PPI Output Q/Q Q2 | 0.90% | 0.10% | 0.20% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Jun | 23.5B | 23.2B | 22.4B | 24.4B |

| 09:00 | EUR | Eurozone CPI M/M Jul | -0.30% | 0.10% | 0.10% | |

| 09:00 | EUR | Eurozone CPI Y/Y Jul F | 2.10% | 2.00% | 2.00% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jul F | 1.10% | 1.10% | 1.10% | |

| 12:30 | CAD | International Securities Transactions (CAD) Jun | 11.5B | 4.91B | 2.18B | 3.0B |

| 12:30 | CAD | CPI M/M Jul | 0.50% | -0.10% | 0.10% | |

| 12:30 | CAD | CPI Y/Y Jul | 3.00% | 2.40% | 2.50% | |

| 12:30 | CAD | CPI Core – Common Y/Y Jul | 1.90% | 1.90% | ||

| 12:30 | CAD | CPI Core – Median Y/Y Jul | 2.00% | 2.00% | ||

| 12:30 | CAD | CPI Core – Trim Y/Y Jul | 2.10% | 2.00% | ||

| 14:00 | USD | Leading Index Jul | 0.40% | 0.50% | ||

| 14:00 | USD | U. of Mich. Sentiment Aug P | 98.1 | 97.9 |