{kind=link}

Dollar pares back some of today’s gain in early US session. The better than expected ADP employment data provides no lift to the greenback. Focus will be turning to ISM manufacturing and FOMC rate decision. Nonetheless, as at the time of writing, Dollar is still the second strongest one for today, just next to Sterling. The Pound is apparently supported by not-too-bad UK PMI manufacturing data. Sterling’s fate will depend on whether there will be a “dovish hike” by BoE tomorrow. Euro follows as the third strongest. On the other hand, commodity currencies are generally lower, with New Zealand, Australian Dollar and Canadian Dollar as the weakest three.

On development to note is the strong and immediate reaction in Chinese stocks to renewed threat of US-China trade war. It’s reported that Trump is considering to impose 25% tariffs on USD 200B in Chinese imports, rather than 10%. The announcement could be made as soon as today. The China Shanghai SSE composite closed down -1.8% to 2824.53. The development argues that recent rebound is completed and the index might be ready to head south to retest 2016 low at 2638.30. This will be a key development to watch given that there is still no sign of either side backing down.

US ADP grew 216k, tariffs have yet to materially impact jobs

US ADP report showed private sector jobs grew 216k in July, above expectation of 186k. Prior month’s figure was also revised up from 177k to 181k. Commenting in the release, Ahu Yildirmaz, vice president and co-head of the ADP Research Institute, said “the labor market is on a roll with no signs of a slowdown in sight.” And, “nearly every industry posted strong gains and small business hiring picked up.” Mark Zandi, chief economist of Moody’s Analytics, said, “The job market is booming, impacted by the deficit-financed tax cuts and increases in government spending. Tariffs have yet to materially impact jobs, but the multinational companies shed jobs last month, signaling the threat.”

FOMC rate decision is a major event ahead. But we’re not expecting any surprise from Fed. The central bank is on course for two more rate hikes this year, one in September and another in December. There is no press conference today. Focus will be quickly turned to minutes to be released later on August 22.

More on FOMC:

- Fed to Hold Rates But Will Trump Criticism Restrain a More hawkish Message?

- Is the FOMC Overly-Optimistic?

- FOMC Preview: Fed on Holiday

- Fed Prepares for Rate Hike in September

UK PMI manufacturing dropped to 54.2, BoE could find some cause for pause

UK PMI manufacturing dropped to 54.0 in July, down from 54.3 and missed expectation of 54.2. Markit noted weaker increases in both output and new orders. Also, intermediate goods production falls for first time in two years. Rob Dobson, Director at IHS Markit, said in the release that UK manufacturing “started the third quarter on a softer footing, with rates of expansion in output and new orders losing steam”, and ” failed to provide any meaningful boost to headline GDP growth through the year-so-far.”

Also he noted that “the financial markets still seem to have an interest rate increase nailed on for August.” But, “if the combination of weaker growth and a softening of pipeline cost pressures at manufacturers is mirrored in the larger service sector, the Bank of England’s decision will be far from unanimous and they may even yet find some cause for pause.”

UK NIESR urges BoE to stand ready to move in either direction should circumstances change

The UK National Institute of Economic and Social Research release an article “Prospects for the UK Economy” yesterday. It warned that the economy is “facing an unusual level of uncertainty because of Brexit”. Such “uncertainty primarily stems from the yet to be defined relationship between the UK and the EU”, as well as “the economy’s response to the new framework once it emerges.” And it criticized Prime Minister Theresa May’s Brexit white paper for failing to “unite the government or Parliament”, thus “leaving open an entire spectrum of possible outcomes.”

The NIESR conditioned its economic forecast with a 25bps BoE rate hike this month, that is, tomorrow. That’s also under the assumption of a “soft Brexit”. The economic is expected to grow at potential with GDP up 1.4% this year, and 1.7% next year. But “risks to our GDP growth forecast are wider than before and tilted to the downside.”

NIESR also urged BoE to take account of the uncertainty of Brexit when setting policy and “also weigh the consequences of ‘getting it wrong’.” That is, It urged BoE to “stand ready to move in either direction should circumstances change.” BoE should “emphasise the uncertainty (rather than the certainty) of its future policy stance in its communications and its willingness to reverse its decisions.”

Eurozone PMI manufacturing finalized at 55.1, slowdown reflects worries on trade wars, tariffs and rising prices

Eurozone manufacturing PMI is finalized at 55.1 in July, unrevised. That was a touch higher than June’s final reading of 54.9. Market noted in the release that growth of both output and new orders remain subdued compared to earlier in the year. Also, new export order growth at near-two year low amid concerns about tariffs and trade wars. Among the countries, the Netherlands scored 58.0, but hit a 14 month low. Germany came second at 56.9 (revised down from 57.3). Italy hit a 21-month low at 51.5.

Chris Williamson, Chief Business Economist at IHS Markit said “the survey responses indicate that the slowdown likely reflects worries about trade wars, tariffs and rising prices, as well as general uncertainty about the economic outlook. Optimism about the future remained at one of the lowest levels seen over the past two years.”

Japan Nishimura: Meeting with USTR Lighthizer not prelude to bilateral FTA

Japanese Deputy Chief Cabinet Secretary Yasutoshi Nishimura emphasized today that the meeting between Economy Minister Toshimitsu Motegi and US Trade Representative Robert Lighthizer next week is not a prelude to a bilateral free trade agreement.

Nishimura reiterated the government’s stance that “Japan does not desire an FTA and these talks are not at all preliminary discussions on an FTA.” Though he noted that “We will be looking for the best path for both the United States and Japan.”

In additional he also ruled out setting a quantitative limit on auto exports to the US. He said “whether it’s exports or imports, we will not set numerical targets.” And, “the fundamental thing is to maintain free and fair trade.”

Regarding the threat of auto tariffs from Trump, Nishimura said “raising tariffs on autos would have a big impact on the world economy and would be a big minus for the American economy, so we want to talk firmly so that does not happen.”

Japan has been very clear on their intention to bring the US back to the multilateral Trans-Pacific Partnership pact which Trump quitted as one of the first things he did after taking office.

Japan PMI manufacturing finalized at 52.3, export sales stalled for second month

Japan PMI manufacturing was finalized at 52.3, revised up from 51.6. But the reading was still the lowest in 11 months. Joe Hayes, Economist at IHS Markit noted in the release that “latest survey data signalled a slowdown to manufacturing sector growth at the beginning of Q3. Output growth eased and there was a noticeable softening of demand, while export sales failed to record any upswing for a second month running.” “Input price inflation accelerated to an 88-month high, resulting in the strongest rate of increase in selling charges for almost a decade”. But the rise was “primarily cost-pus”. Hence, “further weakness in total new business growth could skew the inflationary outlook to the downside.”

China Caixin PMI manufacturing dropped to 50.8, export market continued to deteriorate

China Caixin PMI manufacturing dropped -0.2 to 50.8 in July, down from 51.0, slightly below expectation of 50.9. It’s also the lowest since November 2017. The key points in the release are slower increase in output and new orders, fastest decline in new export sales for over two years and solid rise in input costs. Looking at the details, new export orders shrunk at the fastest pace since June 2016, indicating the export market continued to deteriorate. Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group, said in the release that “in general, the survey signaled a weakening manufacturing trend as a grim export market dragged on the sector’s performance. The positive drivers were the increase in stocks of purchases and easing pressure on capital turnover.”

New Zealand employment grew 0.5%, unemployment rate edged higher to 4.5%

New Zealand employment grew 0.5% qoq in Q2, down from prior quarter’s 0.6% qoq, but beat expectation of 0.4% qoq. Unemployment rate rose 0.1% to 4.5%, above expectation of 4.4%. Participation rate rose 0.1% to 70.9%. All sector wage inflation rose 0.5%. From Australia, AiG performance of manufacturing index dropped notable 52 in July, down from 57.4.

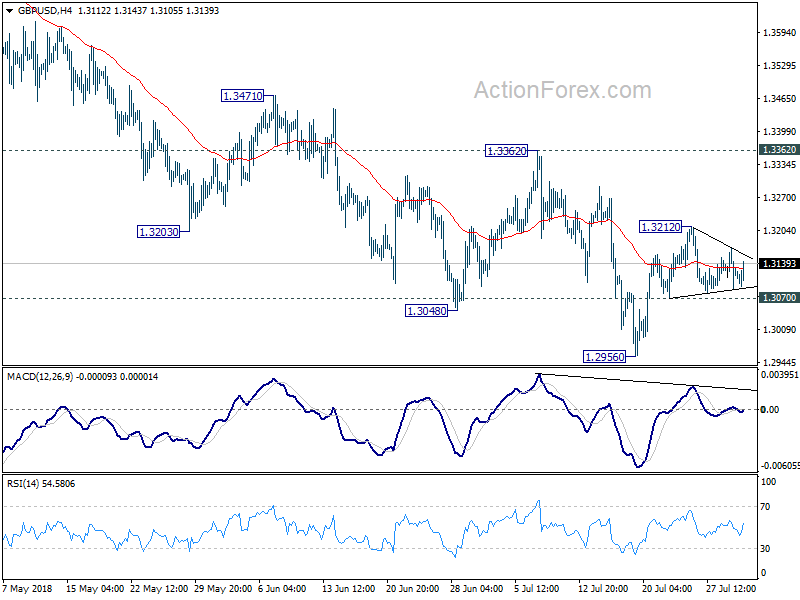

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3086; (P) 1.3129; (R1) 1.3168; More…

GBP/USD continues to stay in tight range between 1.3070/3212 and intraday bias stays neutral. Outlook is unchanged that price actions from 1.2956 are viewed as a corrective pattern. On the downside, break of 1.3070 minor support will indicate completion of rebound form 1.2956 and turns bias back to the downside for retesting this low. Firm break there will resume larger decline from 1.4376 for 1.2874 fibonacci level next. On the upside, above 1.3212 will bring further recovery. But upside should be limited by 1.3362 resistance to bring larger decline resumption eventually.

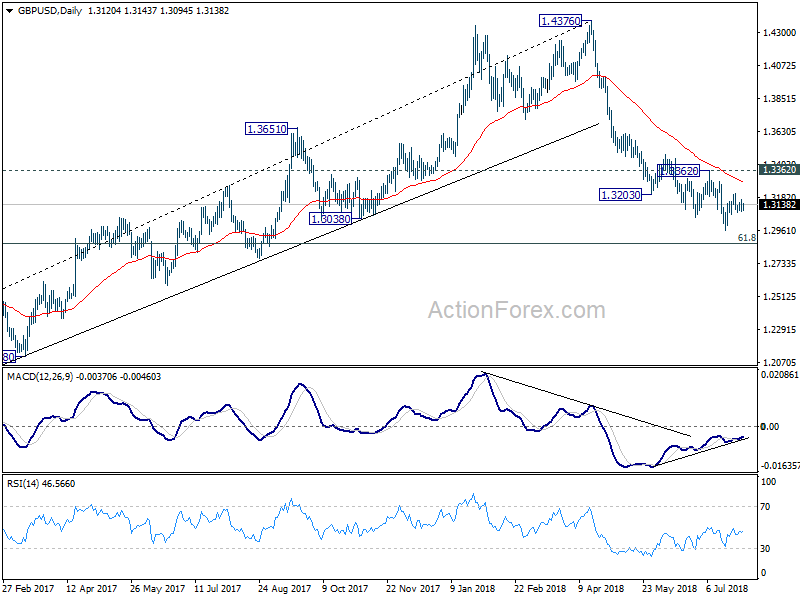

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4179). Fall from 1.4376 should extend to 61.8% retracement of 1.1946 (2016 low) to 1.4376 at 1.2874 next. Decisive break of 1.2874 will raise the chance of long term down trend resumption through 1.1946 low. On the upside, break of 1.3362 resistance is needed to be the first indication of medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Manufacturing Index Jul | 52 | 57.4 | ||

| 22:45 | NZD | Unemployment Rate Q2 | 4.50% | 4.40% | 4.40% | |

| 22:45 | NZD | Employment Change Q/Q Q2 | 0.50% | 0.40% | 0.60% | |

| 23:01 | GBP | BRC Shop Price Index Y/Y Jul | -0.30% | -0.50% | ||

| 00:30 | JPY | PMI Manufacturing Jul F | 52.3 | 51.6 | 51.6 | |

| 01:45 | CNY | Caixin China PMI Mfg Jul | 50.8 | 50.9 | 51 | |

| 06:30 | AUD | RBA Commodity Index SDR Y/Y Jul | 7.60% | 6.60% | ||

| 07:45 | EUR | Italy Manufacturing PMI Jul | 51.5 | 53 | 53.3 | |

| 07:50 | EUR | France Manufacturing PMI Jul F | 53.3 | 53.1 | 53.1 | |

| 07:55 | EUR | Germany Manufacturing PMI Jul F | 56.9 | 57.3 | 57.3 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Jul F | 55.1 | 55.1 | 55.1 | |

| 08:30 | GBP | PMI Manufacturing Jul | 54 | 54.2 | 54.4 | 54.3 |

| 12:15 | USD | ADP Employment Change Jul | 219K | 186K | 177K | 181K |

| 13:30 | CAD | Manufacturing PMI Jul | 57.1 | |||

| 13:45 | USD | US Manufacturing PMI Jul F | 55.5 | 55.5 | ||

| 14:00 | USD | Construction Spending M/M Jun | 0.30% | 0.40% | ||

| 14:00 | USD | ISM Manufacturing Jul | 59.3 | 60.2 | ||

| 14:00 | USD | ISM Employment Jul | 56 | |||

| 14:00 | USD | ISM Prices Paid Jul | 75.5 | 76.8 | ||

| 14:30 | USD | Crude Oil Inventories | -2.6M | -6.1M | ||

| 18:00 | USD | FOMC Rate Decision (Upper Bound) | 2.00% | 2.00% | ||

| 18:00 | USD | FOMC Rate Decision (Lower Bound) | 1.75% | 1.75% |