{kind=link}

Euro drops sharply today as markets are not quite happy with ECB announcement. In particular, while deciding to end the asset purchase program this year, ECB said interest rate will remain at current level at least through 2019 summer. President Mario Draghi also sounds cautious as usual in the post-meeting press conference. Adding to that, 2018 GDP growth forecast was revised notably lower. Though, a positive point is that inflation projections are revised notably higher too. On the other hand, Dollar is lifted by stellar retail sales report and solid as usual jobless claims report. Sterling was lifted briefly earlier today by strong retail sales data. But the Pound was dragged down by Euro in early US session.

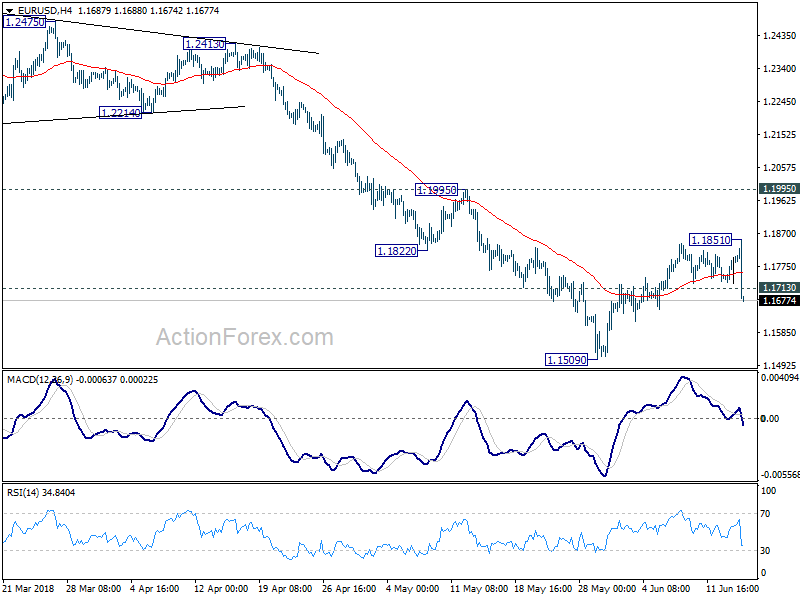

Technically, EUR/USD’s break of 1.1713 should now indicate completion of recent rebound from 1.1509. Retest of this low would be seen shortly. USD/CHF’s rebound also put 0.9911 resistance into focus. Firm break of which will confirm completion of corrective pull back from 1.0056.

ECB to taper APP to EUR 15B/M after September, end it after December

ECB left monetary policies unchanged as widely expected today. And it announced to taper the asset purchase program after September, then end it after December this year. The main refinancing rate is held at 0.00%. Correspondingly, the marginal lending facility rate is held at 0.25%. Deposit facility rate is held at -0.40%. Also, ECB said the key interest rates will “remain at their present levels at least through the summer of 2019”.

The current EUR 30B per month asset purchase program will continue to run as planned till the end of September. Then, the monthly size will be tapered to EUR 15B, subject to incoming data. The program will then run till the end of December 2018 and end there. ECB said the decisions “maintain the current ample degree of monetary accommodation that will ensure the continued sustained convergence of inflation towards levels that are below, but close to, 2% over the medium term.”

Euro drops sharply as markets are not too happy with ECB’s “judgement”. The decision to taper, instead of ending it right after September could be a factor. The more important one could be this part of the statement. “The Governing Council expects the key ECB interest rates to remain at their present levels at least through the summer of 2019 and in any case for as long as necessary to ensure that the evolution of inflation remains aligned with the current expectations of a sustained adjustment path.”

ECB President Mario Draghi’s cautious tone is not helping Euro neither. One important point to note in the introductory statement is the revision in economic projections. ECB now projects annual GDP growth to be at 2.1% in 2018, that’s notable downward revision from March projection of 2.4%. For 2019 and 2020, GDP projections were kept unchanged at 1.9% and 1.7% respectively. On the other hand, HICP inflation is projected to be 1.7% in 2018, 2019 and 2020. That’s notably revised up from March projection of 1.4% in 2018, 1.4% in 2019 and 1.7% in 2020.

Also from Eurozone, German CPI was finalized at 0.50% mom, 2.2% yoy in May.

US retail sales and jobless claims beat expectations

Initial jobless claims dropped -4k to 28k in the week ended June 9, slightly better than expectation of 223k. Four-week moving average of initial claims dropped -1.25k to 224.25k. Continuing claims dropped -49k to 1.697m in the week ended June 2, lowest since December 1, 1973. Four-week moving average of continuing claims dropped -3.75k to 1.726m, lowest since December 8, 1973.

Headline retail sales rose 0.8% in May versus expectation of 0.4% mom. Ex-auto sales rose 0.9% versus expectation of 0.3%. Import price rose 0.6% mom in May versus expectation of 0.5% mom.

Also released, new housing price index rose 0.0% mom in April versus expectation of 0.2% mom.

Trump’s decision on Chinese tariffs watched

Main focus in the US session will now be on Trump’s decision regarding tariffs on USD 50B of 1300 lines of Chinese imports. that’s the action under section 301 investigation in response to forced transfer of U.S. technology and intellectual property. It’s different from the section 232 steel and aluminum tariffs against the world. The section 301 tariffs solely targeted at China. Trump will meet with his trade advisors to make a decision. The final list of tariffed products could be unveiled as soon as tomorrow.

Chinese Foreign Ministry spokesman Geng Shuang said today that there were progress in the trade talks with the US. But he warned that those agreements reached will be voided if Trump decides to go on with the tariffs. He also emphasized that that “The essence of China-U.S. trade and business ties is cooperation and win-win. We have consistently upheld that both sides should appropriately resolve relevant trade and business problems … via dialogue and consultations,”

Sterling enjoyed brief rally on stellar May retail sales

Sterling surges after much stronger than expected retail sales data in May. But it was then dragged down by Euro after ECB rate decision. Retail sales include fuel rose 1.3% mom versus expectation of 0.5% mom and prior 1.8% mom. Retail sales include fuel rose 3.9% yoy versus expectation of 2.4% yoy and prior 1.4% yoy. Retail sales ex-fuel rose 1.3% mom versus expectation of 0.3% mom and prior 1.4% mom. Retail sales ex-fuel rose 4.4% yoy versus expectation of 2.5% yoy and prior 1.4% yoy.

In the release, ONS noted that “feedback from retailers suggested that a sustained period of good weather and Royal Wedding celebrations encouraged spending in food and household goods stores in May.” And, the sharp 3.9% yoy rise in headline years was “possibly due to a combination of warm weather and slow year-on-year growth in May 2017 at 0.8%.”

Also from UK, RICS house price balance improved to -3 in May.

Australian Dollar lower on job and China data

Australian Dollar is pressured by its own data miss as well as weaker than expected China data today. Australia employment rose 12k seasonally adjusted in May, below consensus of 19.2k. Unemployment rate dropped to 5.4%, as participation rate also dropped to 65.5%.

From China, retail sales rose 8.5% yoy in May, slowed from 9.4% yoy and missed expectation of 9.6% yoy. Industrial production slowed to 5.8% yoy, down from 7.0% yoy and missed expectation of 7.0% yoy. Fixed asset investment slowed to 6.1% yoy, down from 7.0% yoy and missed expectation of 7.0% yoy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1745; (P) 1.1773 (R1) 1.1822; More…..

EUR/USD’s sharp fall and firm break of 1.1713 minor support suggests that corrective rise form 1.1509 has completed at 1.1851 already. Intraday bias is turned back to the downside for 1.1509 low first. Break will resume larger down trend from 1.2555 to 50% retracement of 1.0339 to 1.2555 at 1.1447. On the upside, above 1.1851 will extends the corrective rise from 1.1509. But as noted before, upside should be limited by 1.1995 resistance to bring down trend resumption eventually.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won’t consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS House Price Balance May | -3% | -5% | -8.00% | -7% |

| 01:00 | AUD | Consumer Inflation Expectation Jun | 4.20% | 3.70% | ||

| 01:30 | AUD | Employment Change May | 12.0K | 19.2K | 22.6k | 18.3K |

| 01:30 | AUD | Unemployment Rate May | 5.40% | 5.60% | 5.60% | |

| 02:00 | CNY | Retail Sales Y/Y May | 8.50% | 9.60% | 9.40% | |

| 02:00 | CNY | Industrial Production Y/Y May | 6.80% | 7.00% | 7.00% | |

| 02:00 | CNY | Fixed Assets Ex Rural YTD Y/Y May | 6.10% | 7.00% | 7.00% | |

| 04:30 | JPY | Industrial Production M/M Apr F | 0.50% | 0.30% | 0.30% | |

| 06:00 | EUR | German CPI M/M May F | 0.50% | 0.50% | 0.50% | |

| 06:00 | EUR | German CPI Y/Y May F | 2.20% | 2.20% | 2.20% | |

| 08:30 | GBP | Retail Sales Inc Auto Fuel M/M May | 1.30% | 0.50% | 1.60% | 1.80% |

| 11:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | ||

| 12:30 | EUR | ECB Press Conference | ||||

| 12:30 | CAD | New Housing Price Index M/M Apr | 0.00% | 0.20% | 0.00% | |

| 12:30 | USD | Retail Sales Advance M/M May | 0.80% | 0.40% | 0.30% | |

| 12:30 | USD | Retail Sales Ex Auto M/M May | 0.90% | 0.30% | 0.30% | |

| 12:30 | USD | Import Price Index M/M May | 0.60% | 0.50% | 0.30% | 0.60% |

| 12:30 | USD | Initial Jobless Claims (Jun 09) | 218K | 223K | 222K | |

| 14:00 | USD | Business Inventories Apr | 0.30% | 0.30% | ||

| 14:30 | USD | Natural Gas Storage | 87B | 92B |