{kind=link}

Dollar is generally staying in familiar range, except versus Japanese Yen as markets await FOMC rate decision today. The federal funds rate is expected to be lifted by 25bps to 1.75-2.00%. There is practically no chance for Fed to disappoint the markets. Yet, there are a number of questions that could be answered by the voting, the statement, the press conference and the economic projections. A immediate one is whether Fed is on track for one or two more rate hikes this year. Further than that, we’d be keen to know where the neutral rate is in the board’s minds. And, Fed could tweak the language to reflect that it’s closer to neutral now.

More on FOMC

- FOMC Preview – Fed’s Rate Hike A Done Deal, Focus Turned to Forward Guidance

- FOMC Meeting: Rate Hike A ‘Done Deal’ But What About Inflation?

- Dollar Firm as Rate Hike Imminent; But Will Fed also Raise Rate Path Forecast?

Technically, USD/JPY in on track to extend the rebound from 108.10 towards 111.39 resistance. AUD/USD’s near term outlook is staying bearish as corrective rebound from 0.7411 should have completed at 0.7676. And deeper fall is expected to retest 0.7411 in near term. However, EUR/USD is holding above 1.1713 minor support for the moment and thus, could still extend recent corrective rebound from 1.1509. GBP/USD is also holding above 1.3341 minor support and UK CPI today could move the pair first.

Eurosceptic Savona: I never asked to leave indispensable Euro

The known Eurosceptic Italian Minister for European Affairs Paolo Savona said he fully backed the Euro as it’s “indispensable” even though the currency union needs to be “perfected” in regards to its system of governance. He urged that the ECB should be given a “new statute” similar to Federal Reserve. And, it’s “fundamental that the ECB should be able to act on exchange rates.” A so called “Plan B” was laid out in his book, written just before becoming minister, for an orderly exit from Euro if necessary. Savona emphasized that was written as a “analyst”. He said “there is no plan B and I never asked to leave.”

Savona, who has been highly critical on Germany, said that it’s a “great country from many points of view, culturally, economically and politically.” But he pointed out a major difference between him and many German economists. He noted that “they tend to see stability as a necessary condition for growth, while I am part of a group who sees growth as a necessary condition for stability.”

Italy was nearly in another political an constitutional crisis after President Sergio Mattarella vetoed Savona as economy minister. The antiestablishment coalition of 5-Star Movement and the League quitted forming the government. But then, they came back with Giovanni Tria as Economy Minister and kept Savona in the cabinet as Minister for European Affairs

Trump wants to stop war games for negotiation in good faith with North Korea

US President Donald Trump confirmed his intention to stop military exercise with South Korea while the negotiation with North Korea is in progress. He said in a Fox News interview in Singapore that “we’re not going to be doing the war games as long as we’re negotiating in good faith.” “So that’s good for a number of reasons, in addition to which we save a tremendous amount of money”. And, “you know, those things, they cost. I hate to appear a businessman, but I kept saying, what’s it costing?”

Republican Senator Lindsey Graham blasted the idea of cost cutting as ridiculous as “it’s not a burden onto the American taxpayer to have a forward deployed force in South Korea.” He added that “It brings stability. It’s a warning to China that you can’t just take over the whole region. So I reject that analysis that it costs too much, but I do accept the proposition, let’s stand down (on military exercises) and see if we can find a better way here.”

Japan Defence Minister Onodera: Military drills vital to East Asia security

Japan Defence Minister Itsunori Onodera emphasized that “the drills and the US military stationed in South Korea play a vital role in East Asia’s security.” And he hoped to “share this recognition between Japan and the US, or among Japan, US and South Korea.”

Onodera also said there is no change in Japan’s policy after the Kim-Trump summit, of “putting pressure” on North Korea. And, Japan would stick to plans to bolster its defences against a possible ballistic missile strike from North Korea.

Separately, Chief Cabinet Secretary Yoshihide Suga said that Japan could shoulder some of the costs of North Korea’s denuclearization, on the condition that International Atomic Energy Agency (IAEA) restarts inspections.

RBA Lowe: Any increase in interest rates, they’re some time away

RBA Governor Philip Lowe delivered a speech titled “Productivity, Wages and Prosperity” today. There he pointed out that “over the past couple of years, output growth has been subdued, but employment growth has been strong.” And, it’s productivity that’s holding the economy back. Low pointed to strong employment growth in household services, but output per hour worked was only 4% higher than it was in 2010. In contrast, the output per hour worked was up 13% to 16% in other industry groups.

He urged “strong ongoing focus on training, education and the accumulation of human capital” to bring up the overall productivity. And he emphasized that “our national comparative advantage will increasingly be built on the quality of our ideas and our human capital.”

Regarding monetary policy, Lowe said the economy is “moving in the right direction” and the next move in interest rate will be “up, not down”. But, “the environment in which interest rates are increasing is also likely to be one in which people’s incomes are growing more quickly than they are now.”And, “any increase in interest rates, however, still looks to be some time away.”

On the data front

Australia Westpac consumer confidence rose 0.3% in June. Swiss PPI will be released in European session. Eurozone will release industrial production and employment. But UK CPI will catch most attention. US will release PPI today but main focus in on FOMC rate decision and press conference.

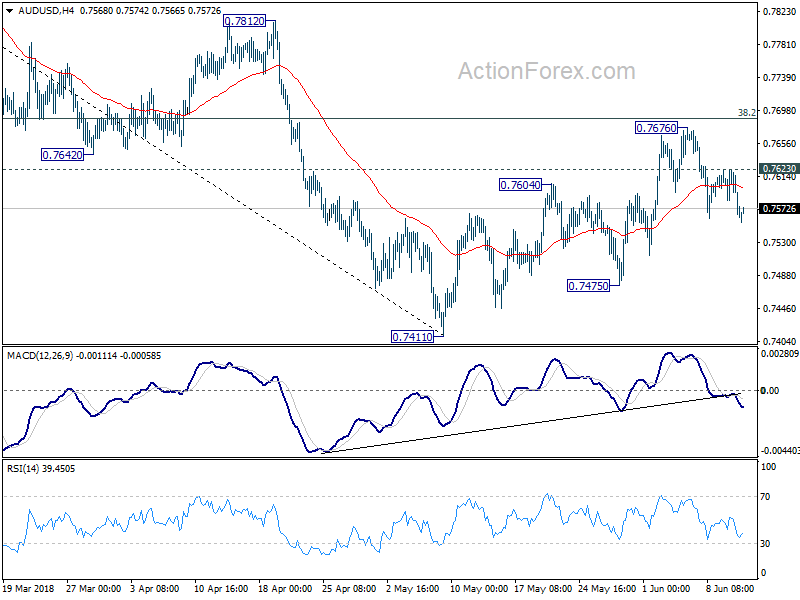

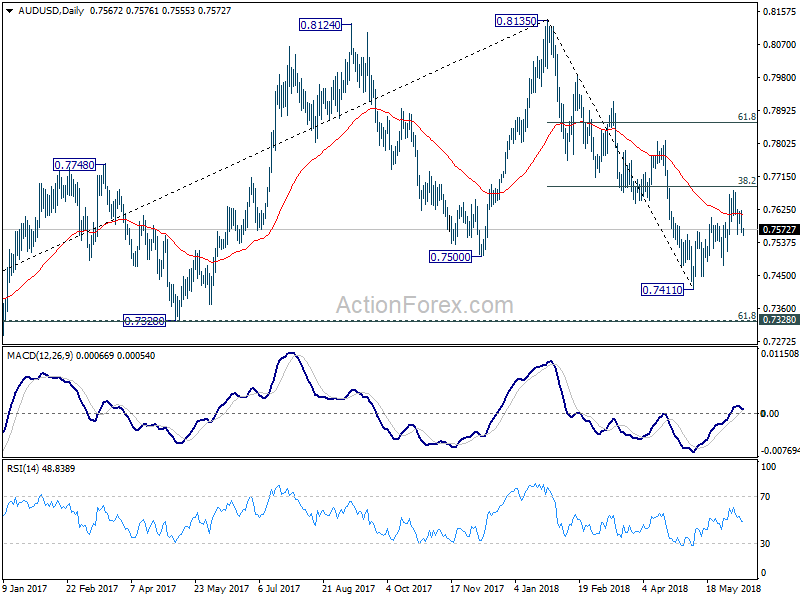

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7594; (P) 0.7608; (R1) 0.7625; More…

Despite some jittery, AUD/USD’s fall from 0.7676 is still in progress and intraday bias remains on the downside. As noted before, corrective rise from 0.7411 should have completed just ahead of 38.2% retracement of 0.8135 to 0.7144 at 0.7688. Deeper fall should be seen to 0.7475 support first. Break there should resume larger fall from 0.8135 and target 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326). Though, above 0.7623 minor resistance will delay the bearish case and extend the correction from 0.7411 instead.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. Prior break of 0.7500 key support suggests that such correction is completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. In case of another rise, we’d expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption eventually.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | AUD | Westpac Consumer Confidence Jun | 0.30% | -0.60% | ||

| 7:15 | CHF | Producer & Import Prices M/M May | 0.10% | 0.40% | ||

| 7:15 | CHF | Producer & Import Prices Y/Y May | 3.20% | 2.70% | ||

| 8:30 | GBP | CPI M/M May | 0.40% | 0.40% | ||

| 8:30 | GBP | CPI Y/Y May | 2.50% | 2.40% | ||

| 8:30 | GBP | Core CPI Y/Y May | 2.10% | 2.10% | ||

| 8:30 | GBP | RPI M/M May | 0.40% | 0.50% | ||

| 8:30 | GBP | RPI Y/Y May | 3.40% | 3.40% | ||

| 8:30 | GBP | PPI Input M/M May | -0.10% | 0.40% | ||

| 8:30 | GBP | PPI Input Y/Y May | 7.00% | 5.30% | ||

| 8:30 | GBP | PPI Output M/M May | 0.30% | 0.30% | ||

| 8:30 | GBP | PPI Output Y/Y May | 2.90% | 2.70% | ||

| 8:30 | GBP | PPI Output Core M/M May | 0.10% | 0.10% | ||

| 8:30 | GBP | PPI Output Core Y/Y May | 2.20% | 2.40% | ||

| 8:30 | GBP | House Price Index Y/Y Apr | 4.40% | 4.20% | ||

| 9:00 | EUR | Eurozone Industrial Production M/M Apr | -0.50% | 0.50% | ||

| 9:00 | EUR | Eurozone Employment Q/Q Q1 | 0.30% | 0.30% | ||

| 12:30 | USD | PPI M/M May | 0.20% | 0.10% | ||

| 12:30 | USD | PPI Y/Y May | 2.70% | 2.60% | ||

| 12:30 | USD | PPI Core M/M May | 0.20% | 0.20% | ||

| 12:30 | USD | PPI Core Y/Y May | 2.70% | 2.30% | ||

| 14:30 | USD | Crude Oil Inventories | 2.1M | |||

| 18:00 | USD | FOMC Rate Decision (Upper Bound) | 2.00% | 1.75% | ||

| 18:00 | USD | FOMC Rate Decision (Lower Bound) | 1.75% | 1.50% | ||

| 18:30 | USD | FOMC Press Conference |