{kind=link}

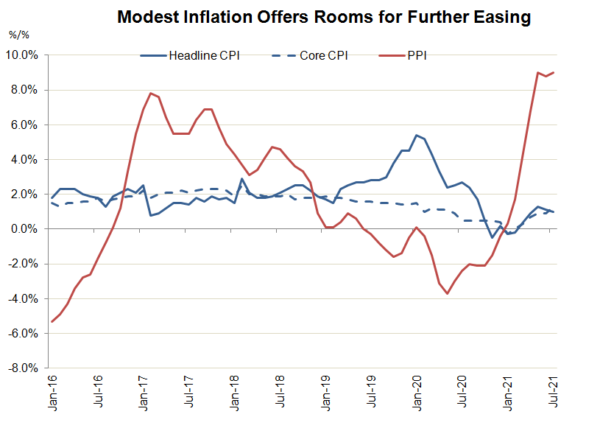

Headline CPI eased to +1% y/y in July from +1.1% a month ago. From a month ago, inflation rose +5.3%, compared with +1.8% in June. This suggests that the slowdown in the year-over-year data was mainly due to high base. Food inflation contracted -3.7% y/y, after dropping -1.7% in June. Deflation in pork prices worsened to -43.5% y/y in July from -36.5% a month ago. Meanwhile, fresh vegetable price also fell into deflation, falling -4% y/y during the month. Yet, fresh fruit price accelerated to +5.2%, from June’s +3.1%. Non-food price improved to +2.1% y/y in Jule, from +1.7% in the prior month. Core CPI, the headline inflation excluding food and energy, climbed higher to +1.3% y/y. In June, the reading was +0.9%.

On the upstream prices, PPI accelerated to +9% y/y in July, from +8.8% in the prior month. The monthly reading also rose to +9.7% in July, from June’s +6.4%. The report reveals that the cost of production continued to increase in China. Yet, producers find it difficult to pass the cost to customers.

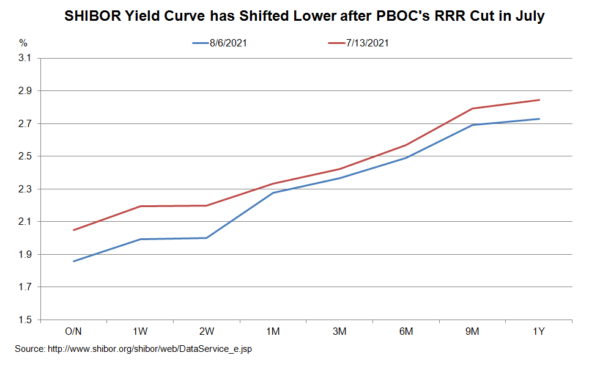

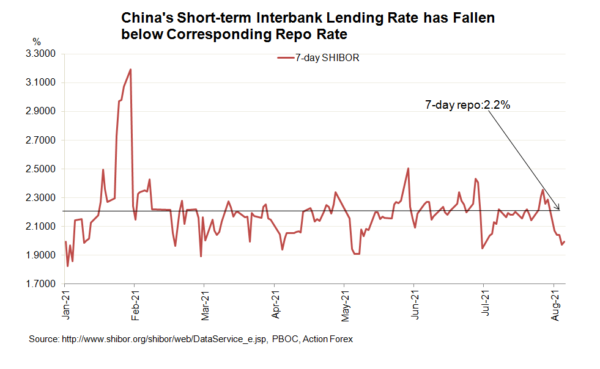

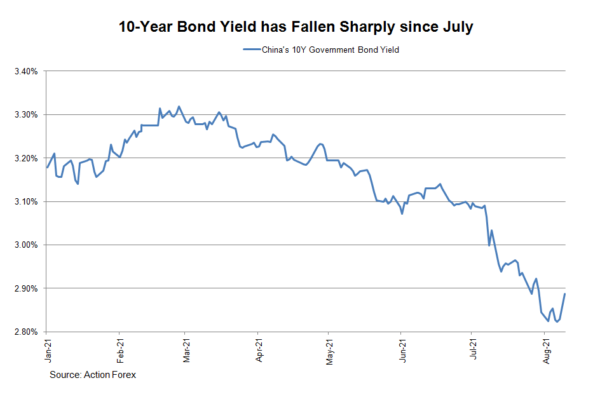

Modest CPI inflation suggests that the PBOC could still go ahead with further easing in coming months. The PBOC cut the broad RRR by -50 bps in July and affirmed a prudent and stable monetary policy stance. We believe this was an insurance cut to prevent deterioration in the country’s growth. The worsening of delta outbreak in the country affirms that more easing is needed from the central bank. Indeed, the market is preparing for more RRR cut later this year. The decline in 10-year government bond yield has accelerated since July. From the peak in mid-February, the yield has actually fallen more than 40 bps. Interbank borrowing costs have also been lowered. The entire SHIBOR yield curve has shifted lower after PBOC’s RRR last month. Meanwhile, the 7-day SHIBOR rate has consistently been trading below the 7-day repo rate since the beginning of August. The cost of borrowing amongst financial institutions has been lowered amidst PBOC’s injection of liquidity.

Interbank borrowing costs have also been lowered. The entire SHIBOR yield curve has shifted lower after PBOC’s RRR last month. Meanwhile, the 7-day SHIBOR rate has consistently been trading below the 7-day repo rate since the beginning of August. The cost of borrowing amongst financial institutions has been lowered amidst PBOC’s injection of liquidity.