{kind=link}

Dollar jumps broadly overnight but it’s rally is starting to lose steam again in Asian session. Instead, while Yen remains the weakest one for the week, it’s starting to regain some strength. So far, the Japanese is not benefiting from risk aversion this week. Even though stocks attempted to rebound, there was no sustainable buying. DOW closed nearly flat by -0.04% overnight but NASDAQ extended recent fall by closing down -0.85% at 6949.23, losing 7000 handle. The pre-holiday calendar is rather busy today and we could see some bigger moves as liquidity dries up.

Technically, in spite of the rebound in the past two days, Dollar is kept below near term resistance level against Europeans. That is, EUR/USD is held above 1.2285, GBP/USD above 1.3982. While USD/CHF breached 0.9568 resistance, it’s kept well off 0.9626 key fibonacci level. USD/CAD also finds no buying even though it’s drawing support above 1.2802, and it’s kept well below recent high at 1.3124.

Dollar is showing more persistent strength only against Australian Dollar and Yen. In particular, USD/JPY’s break of 106.63 resistance is seen as a sign of trend reversal. Near term focus will now turn to 107.28.

Japan FM Aso: No bilateral trade negotiations with US

Japan finance minister Taro Aso said in the parliament that historically, US Dollar always rise against Japanese Yen when interest rate differentials widened to 3%. Aso added that US interest rates will “undoubtedly rise ahead”. And therefore, there won’t be “one-sided” Yen appreciation that could hurt the economy.

Regarding trade, Aso emphasized that Japan should “definitely avoid” bilateral trade negotiations with the US. He added that “When two countries negotiate, the stronger country gets stronger. That’s unnecessary (for Japan) so we’ve been saying all along that we would definitely avoid” bilateral trade talks with the United States.

Japan at beginning of consumer spending recovery

Japan retail sales rose 0.4% mom, 1.6% yoy in February, slightly higher than expectation of 0.6% mom, 1.7% yoy. And it’s marked improvement from January’s -1.6% mom, 1.5% yoy. It’s noted that consumer spending could be at the beginning of mild recovery. Improvement is also seen lately in the labor market. Overall picture suggests that consumption is going to pick up momentum. And that should eventually help lift inflation. But for now, core inflation is still way off BoJ’s 2% target and it will take some more time for BoJ to start considering stimulus exit.

UK Gfk Consumer Confidence: Definitely a movement in the right direction

UK Gfk consumer confidence rose to -7 in March, up from -10 and above expectation of -10. All five of the constituent measures recorded higher values. Personal financial situation over the past 12 months rose 3 pts to 3. Personal financial situation over next 12 months rose 5 pts to 10. General economic situation over the last 12 month rose 3 pts to -26. General economic situation over next 12 months rose 4 pts to -22. Major purchase index rose 2 pts to 2. Saving index rose 1 pt to 13.

Gfk noted in the release that “the prospect of wage rises finally outstripping declining inflation, high levels of employment with low-level interest rates, and finally some movement on the Brexit front appear to have boosted our spirits.” While it’s “still a little early to be talking about green-shoots”, “this is definitely a movement in the right direction”.

Looking ahead

The pre-holiday economic calendar is rather busy today. Swiss will release KOF leading indicator. Germany will release unemployment but more focus would be on CPI. UK will release Q4 GDP final, mortgage approvals, M4 and current account.

Later in US session, Canada will release GDP, IPPI and RMPI. US will release personal income and spending, jobless claims and Chicago PMI. USD/CAD could have some big moves ahead of holidays.

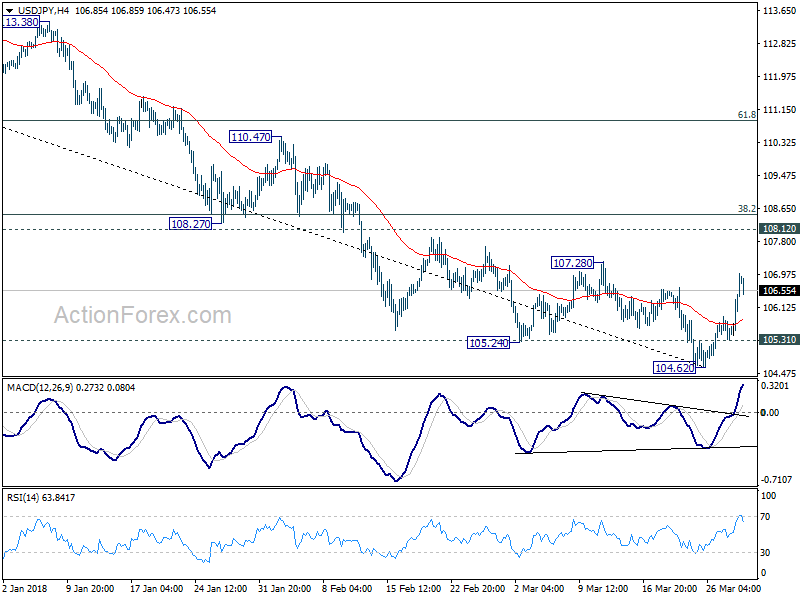

USD/JPY Daily Outlook

Daily Pivots: (S1) 105.12; (P) 105.51; (R1) 105.71; More…

USD/JPY’s rebound from 104.62 extended to as high as 107.00 so far. The break of 106.63 resistance indicates short term bottoming on bullish convergence condition in 4 hour MACD. Intraday bias is back on the upside for 38.2% retracement of 114.73 to 104.62 at 108.48. At this point, there is no confirmation of trend reversal yet. Hence, we’ll look at the reaction from 108.48 (which is close to 108.12 too) to assess the chance. On the downside, below 105.31 minor support will indicate that the rebound is completed and turn bias back to the downside instead.

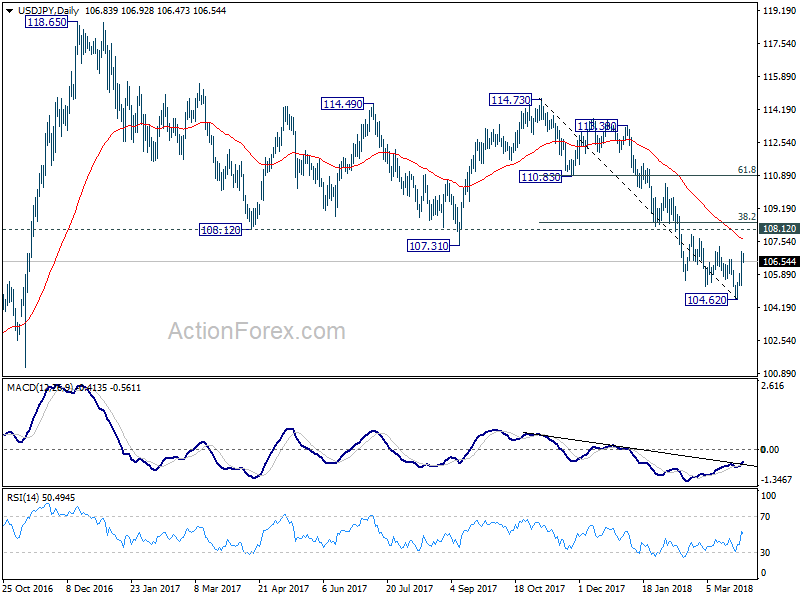

In the bigger picture, medium term down trend from 118.65 (2016 high) is still in progress and extending. Build up in downside momentum argues that it might be extending the whole corrective pattern from 125.85 (2015 high). 100% projection of 118.65 to 108.12 from 114.73 at 104.20 will be a key level to watch as firm break there could bring downside acceleration. And in that case, 98.97 key support level (2016 low) would at least be breached. This bearish case will now be favored as long as 108.12 support turned resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Feb | 5.70% | 0.20% | 0.00% | |

| 23:01 | GBP | GfK Consumer Confidence Mar | -7 | -10 | -10 | |

| 23:50 | JPY | Retail Trade Y/Y Feb | 1.60% | 1.70% | 1.60% | 1.50% |

| 07:00 | CHF | KOF Leading Indicator Mar | 107.2 | 108 | ||

| 07:55 | EUR | German Unemployment Mar | -15K | -22K | ||

| 07:55 | EUR | German Unemployment Claims Rate Mar | 5.30% | 5.40% | ||

| 08:30 | GBP | Mortgage Approvals Feb | 66K | 67K | ||

| 08:30 | GBP | Money Supply M4 M/M Feb | 1.30% | 1.50% | ||

| 08:30 | GBP | Current Account Balance Q4 | -23.7B | -22.8B | ||

| 08:30 | GBP | Index of Services 3M/3M Jan | 0.60% | 0.60% | ||

| 08:30 | GBP | GDP Q/Q Q4 F | 0.40% | 0.40% | ||

| 12:00 | EUR | German CPI M/M Mar P | 0.50% | 0.50% | ||

| 12:00 | EUR | German CPI Y/Y Mar P | 1.70% | 1.40% | ||

| 12:30 | CAD | GDP M/M Jan | 0.10% | 0.10% | ||

| 12:30 | CAD | Industrial Product Price M/M Feb | 0.30% | |||

| 12:30 | CAD | Raw Materials Price Index M/M Feb | 3.30% | |||

| 12:30 | USD | Personal Income Feb | 0.40% | 0.40% | ||

| 12:30 | USD | Personal Spending Feb | 0.20% | 0.20% | ||

| 12:30 | USD | Real Personal Spending Feb | 0.10% | -0.10% | ||

| 12:30 | USD | PCE Deflator M/M Feb | 0.20% | 0.40% | ||

| 12:30 | USD | PCE Deflator Y/Y Feb | 1.70% | 1.70% | ||

| 12:30 | USD | PCE Core M/M Feb | 0.20% | 0.30% | ||

| 12:30 | USD | PCE Core Y/Y Feb | 1.60% | 1.50% | ||

| 12:30 | USD | Initial Jobless Claims (MAR 24) | 231K | 229K | ||

| 13:45 | USD | Chicago PMI Mar | 62 | 61.9 | ||

| 14:00 | USD | U. of Mich. Sentiment Mar F | 102 | 102 | ||

| 14:30 | USD | Natural Gas Storage | -86B |