{kind=link}

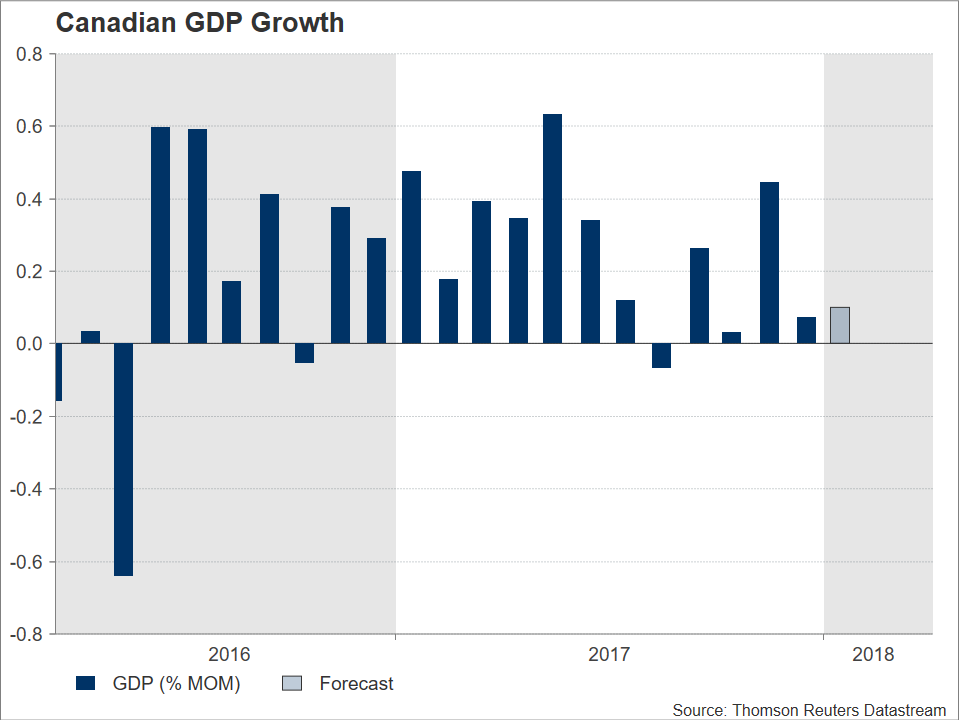

Canadian GDP figures for the month of January are due on Thursday at 1230 GMT. The release could give direction to the local dollar which has been performing poorly relative to its US counterpart, shedding 2.7% year-to-date.

Economic activity in Canada is expected to have expanded by 0.1% m/m during the first month of the year, at the same rate as in December. Strong growth during the first half of 2017 was instrumental for the country’s economy to expand by 3.0% for the year overall, its highest since 2017. Growth after H1 2017 was not as robust though and Thursday’s release is anticipated to show a continuation of this pattern, adding credence to those supporting that the Canadian economy is likely settling to a more sustainable pace of expansion.

Data on Canadian producer prices for the month of February will also be released on Thursday at 1230 GMT, with an increase of 0.5% on a monthly basis being projected by analysts, a faster pace relative to January’s respective reading of 0.3%.

Data on Canadian producer prices for the month of February will also be released on Thursday at 1230 GMT, with an increase of 0.5% on a monthly basis being projected by analysts, a faster pace relative to January’s respective reading of 0.3%.

The Bank of Canada has delivered three 25bps interest rate hikes since July. Market participants currently do not expect a rate increase when the Bank next meets on April 18, while according to Canadian overnight index swaps they project greater than even odds – around 65% – for a quarter percentage point rate hike to be delivered during the meeting in late May. Upbeat GDP and producer price figures have the capacity to push that probability even higher, benefitting the local dollar by pushing dollar/loonie lower.

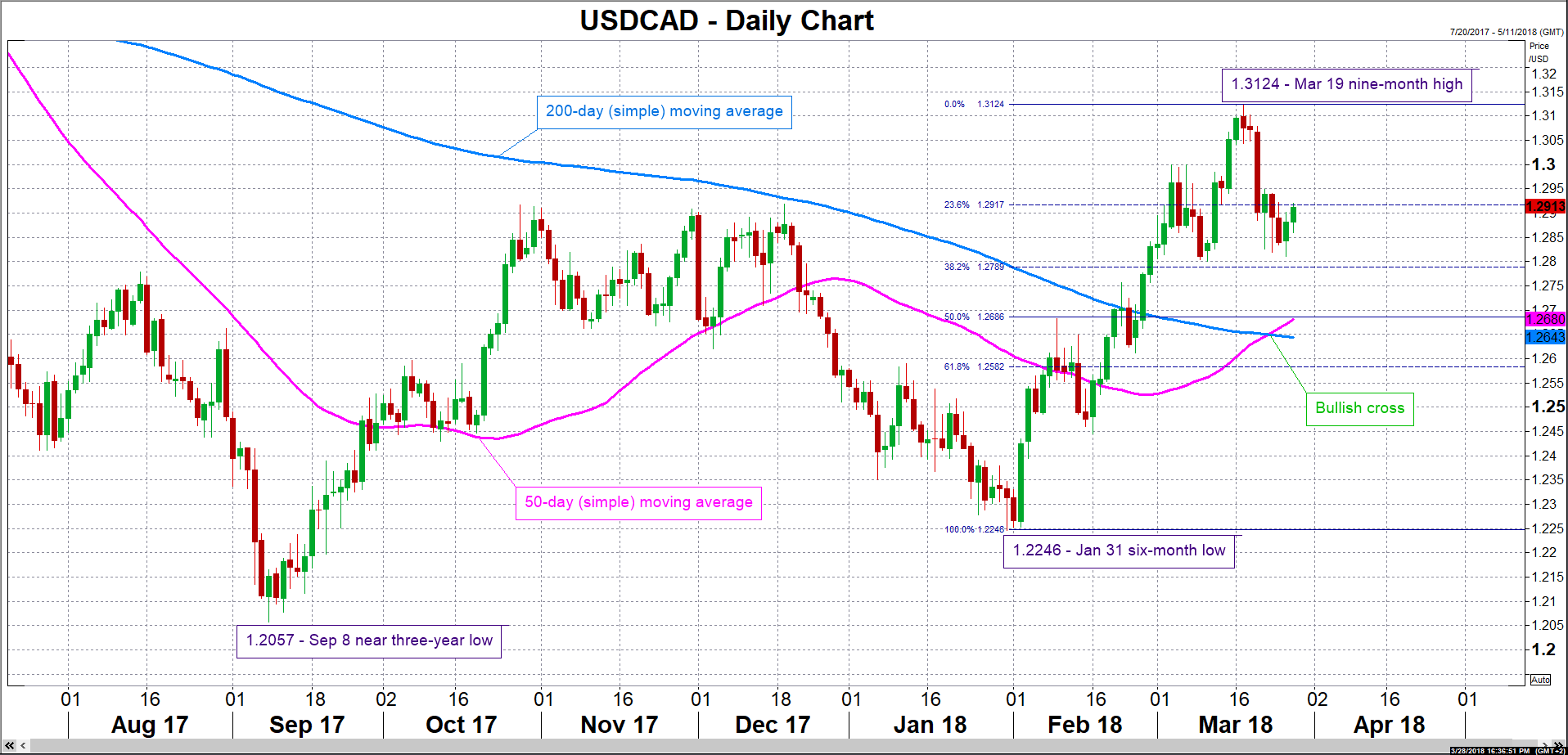

Support in case of a falling dollar/loonie could come around the 38.2% Fibonacci retracement level of the January 31 to March 19 upleg at 1.2789. The area around this mark also includes the 1.28 round figure, while it was one of congestion in previous months. Disappointing numbers on the other hand might propel the pair higher. Dollar/loonie could be meeting resistance at the moment around the 23.6% Fibonacci level at 1.2917 – the range around this encapsulates the 1.29 handle and a few peaks from the recent past. An upside break would shift the focus to 1.30 that may be of psychological significance and then to March 19’s nine-month high of 1.3124.

Within the context of reaction in the dollar/loonie pair, it should be kept in mind that Canadian releases should not be viewed in isolation, as US personal income and consumption data, as well as the core PCE price index – all for the month of February – will be made public at the same time. In the meantime, markets will also have to digest initial and continued jobless claims for the week ending March 24 out of the US.

Within the context of reaction in the dollar/loonie pair, it should be kept in mind that Canadian releases should not be viewed in isolation, as US personal income and consumption data, as well as the core PCE price index – all for the month of February – will be made public at the same time. In the meantime, markets will also have to digest initial and continued jobless claims for the week ending March 24 out of the US.

In the bigger picture, besides tomorrow’s data out of Canada and how they would affect the BoC, the loonie’s broader direction also seems heavily dependent on the future of NAFTA negotiations; the currency appeared very sensitive to developments on this front in the past. In the latest developments, US Trade Representative Robert Lighthizer said in an interview earlier on Wednesday that he is hopeful that an agreement can be reached “in the next little bit”, though he also made reference to a “short window” for such an outcome, implying that the parties involved should act quickly in the face of presidential and midterm congressional elections in Mexico and the US respectively later in the year. The eighth round of talks is expected to commence sometime in April in Washington.

Lastly, the trajectory in oil prices could also affect the loonie given that Canada is a major exporter of the precious liquid. Rising US shale production is a driver that could exert pressure on prices. On the other hand, the appointment of policy-hawks in the Trump administration, such as new National Security Adviser John Bolton, that could push for fresh sanctions on Iran thus taking a chunk of oil supply out of the market, are supportive of prices.