{kind=link}

Here are the latest developments in global markets:

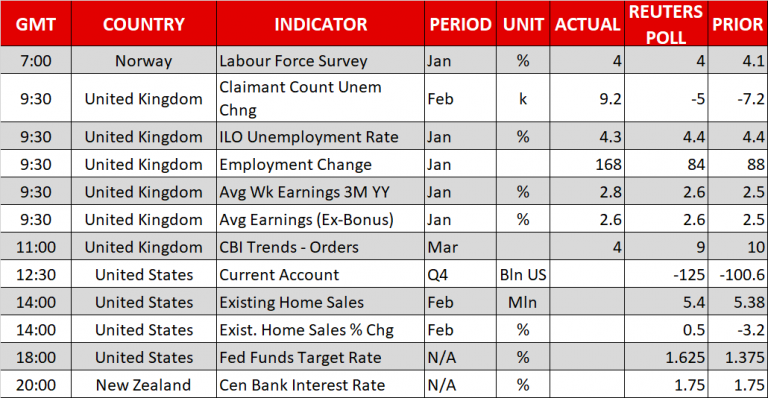

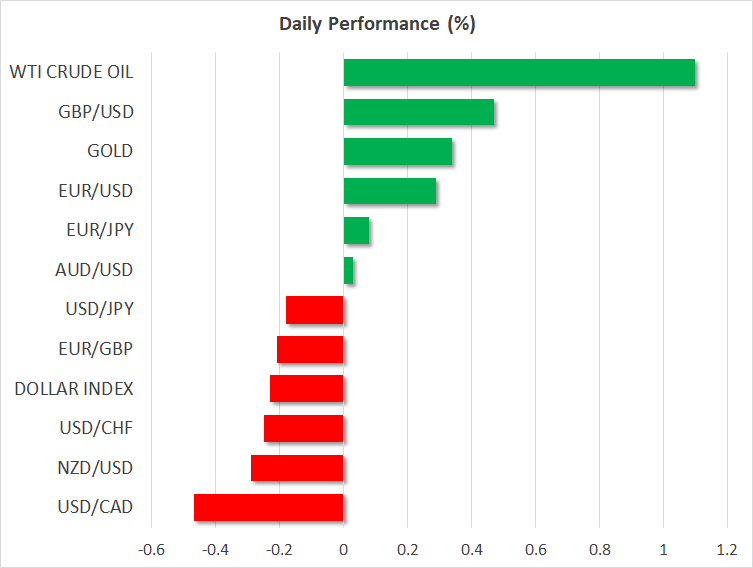

FOREX: Dollar/yen was falling by 0.18% and the dollar index was also under pressure, losing 0.25% at the time of writing as investors were preparing their positions ahead of the Fed interest rate announcement later in the day. While the dollar was struggling to gain ground, the euro managed to recover some losses, with euro/dollar moving higher towards 1.2278 (+0.23%). Pound/dollar touched an intraday high of 1.4074 before it slipped to 1.4043 (+0.34%) after the UK’s unemployment rate came in better than expected in February, falling from 4.4% to 4.3%. It is worth mentioning that the Bank of England is expected to keep interest rates unchanged on Thursday, but deliver a rate hike probably in May. Dollar/loonie extended losses for the third day, last trading at 1.2979 (-0.67%). Aussie/dollar held near its today’s opening level, around 0.7690, while kiwi/dollar declined to 0.7160 (-0.31%). Note that the RBNZ will also decide on monetary policy today but the central bank is anticipated to stand pat on interest rates.

STOCK: European stocks were mixed at 1055 GMT. The blue-chip Euro STOXX 50 was flat, the British FTSE 100 was down by 0.37%, while the German DAX 30 and the Spanish IBEX 35 were up by 0.17% and 0.07% respectively. US stock futures were pointing to a negative open.

COMMODITIES: Oil prices advanced considerably as markets feared that tensions between Saudi Arabia, US and Iran could disrupt supply in the Middle East. WTI crude oil surged by 1.13% towards a fresh three-week high of $64.26 a barrel. Brent crude oil climbed to a six-week high of $68.27, gaining 1.26% at the time of writing. In precious metals, gold increased by 0.34% to $1,314.95 an ounce. Given that oil and gold are depended on the US dollar, they are likely to react to the FOMC decision later today. A strong dollar could drive commodities lower, whilst a weaker dollar could push them higher.

Day ahead: FOMC announcement on interest rates; RBNZ also gathers to decide on monetary policy

Day ahead: FOMC announcement on interest rates; RBNZ also gathers to decide on monetary policy

The Federal Open Monetary Committee concludes its two-day policy meeting today under the lead of Jerome Powell for the first time after his nomination as the new Fed chair. The decision on interest rates will be announced at 1800 GMT and markets have no doubt that policymakers will deliver another 25bps rate hike. However, the question for the jury will be whether the Fed will alter its forecasts for the pace of monetary tightening this year, and hence all eyes will be on the Fed dot plot to identify any change in the distribution of the dots. If the median dot is placed higher, hinting that four rate hikes are now on the cards, dollar bulls could take control. On the other hand, if the picture remains unchanged, this could add some pressure to the greenback as the news could be taken as dovish by investors, potentially hinting that the US economy is not strong enough to support stricter credit constraints. Policymakers could embrace a positive outlook on the economy when they release their fresh economic projections today, considering the benefits arising from the new tax overhaul, the weaker dollar, and stronger global growth. However, the persisting softness in inflation and wage growth under a tighter labor market could keep them cautious and unwilling to change their plans for gradual rate rises for now. A press conference by Powell at 1830 GMT will give more insight into the central bank’s way of thinking.

Two hours later, at 2000 GMT, the Reserve Bank of New Zealand will also make an announcement on interest rates. But in this case, no change is expected, with projections being for the central bank to hold rates at a record low of 1.75%. Inflation readings came in worse than expected in the fourth quarter of 2017 and business sentiment remains at levels seen during the 2008 financial crisis, while a potential global trade war in the face of Trump’s import tariffs are likely to put the country’s terms of trade at risk. If the monetary policy statement following the decision uses a cautious tone, probably highlighting the risks above, the kiwi could extend its recent losses.

Meanwhile, in Australia, investors will be waiting for the Australian Bureau of Statistics to publish February’s employment data early in the Asian session on Thursday (0030 GMT). Expectations are for job growth to post the longest run of employment gains in the survey’s history and the unemployment rate to remain unchanged at 5.5%. It would be interesting to see though, whether job creation is skewed to part-time positions as was the case in January. Such an outcome would be a negative spot on the report.

Turning to today’s remaining data, existing home sales for the month of February out of the US at 1400 GMT might turn positive after two months of falling, while earlier, at 1230 GMT, the US current account deficit during the fourth quarter of 2017 is anticipated to widen.

In energy markets, oil prices might experience some volatility after the release of the Energy Information Administration’s weekly report on US oil inventories for the week ending March 16. Crude oil inventories are anticipated to have risen by 2.600 million barrels, less than the 5.022m seen in the preceding week. If this is the case, that would be the fourth week of consecutive rises. Gasoline inventories and distillate stocks are expected to continue falling.

Legislative developments will also attract attention during the week after US Congressional Republicans failed to unveil their government spending plans on Tuesday, pointing possibly to a third government shutdown on Friday if they do not approve the bill by midnight. Also on Friday, Trump is likely to announce further tariffs on China.