{kind=link}

Here are the latest developments in global markets:

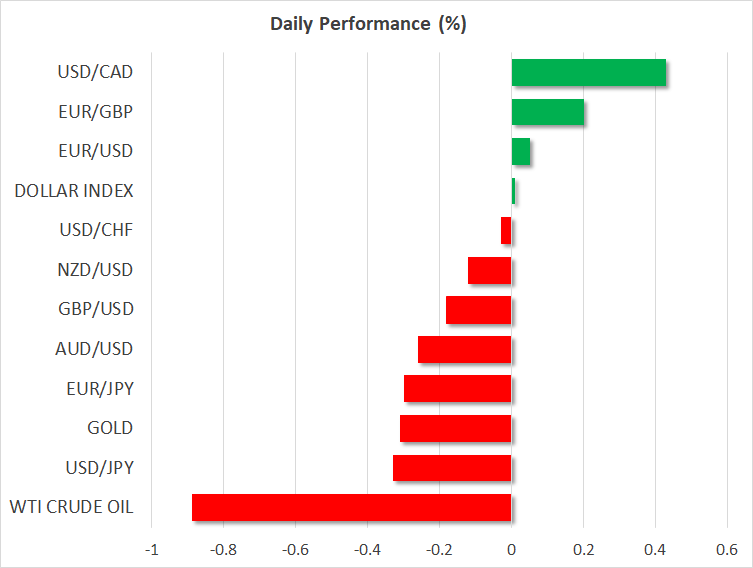

FOREX: The resignation of Trump’s economic adviser and free-trade advocate, Gary Cohn, late yesterday, spurred speculations that the President’s plans to impose hefty import tariffs on aluminum and steel were more likely than analysts previously thought. The dollar index touched a fresh two-week low at 89.40 (-0.14%) and dollar/yen continued to trade near 16-month lows reached yesterday, last seen at 105.46 (-0.46%). Pound/dollar extended losses to reach 1.3858 (-0.17%) after the EU’s Brexit guidelines stated that a future trade deal should address an “appropriate” customs cooperation, preserving any regulatory autonomy. Moreover, the document acknowledged that Britain’s departure from the EU will lead to frictions in trade, though it also revealed the EU’s willingness to maintain a close partnership with the UK. Euro/dollar inched up to a fresh three-week high of 1.2443 (+0.14%) shrugging off US trade threats as the EU reiterated its warnings to react accordingly if the US punitive tariffs materialize. Speaking in Brussels, the EU trade Commissioner argued that US protectionism would damage transatlantic relations, hoping for the EU to be excluded from the tariffs. Dollar/loonie changed hands higher at 1.2932 (+0.43%) ahead of the BoC rate announcement, aussie/dollar edged back up to 0.7800 (-0.24%) but remained down on the day, while kiwi/dollar was weak at 0.7279 (-0.14%).

STOCKS: European stocks corrected lower following their Asian counterparts as Cohn’s resignation revived fears of a potential trade war between the US and the rest of the world. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.26% and 0.23% respectively at 1050 GMT. The German DAX 30 retreated by 0.19%, with automaker shares including mainly those of Volkswagen and Daimler being the worst performers in the index. Still, losses could have been larger if not offset by gains in telecommunications. The French CAC 40 fell by 0.37% and the British FTSE 100 managed to erase earlier losses after the British plane engine maker, Rolls Royce stated that it was on track to meet its 2020 goals, lifting its shares by 12.30%. US futures were in the red, pointing to a negative open.

COMMODITIES: Heightened trade risks weighed on oil prices as well, with WTI crude and Brent remaining pressured at $62.14 (-0.79%) and $65.27 (-0.73%) per barrel respectively. Yesterday, the API oil report added to concerns that US oil production could hamper OPEC’s efforts to curb supply as the numbers indicated a larger increase in US stockpiles than analysts thought. In precious metals, gold was slightly down at $1332.64 (-0.11%) per ounce.

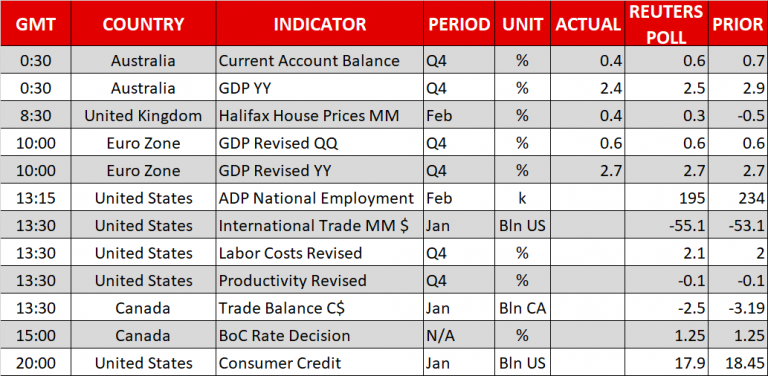

Day ahead: Bank of Canada to announce interest rate decision; US ADP nonfarm employment report in focus

Day ahead: Bank of Canada to announce interest rate decision; US ADP nonfarm employment report in focus

The Bank of Canada (BoC) will announce its rate decision at 1500 GMT and expectations are for the central bankers to keep interest rates steady at 1.25% after raising borrowing costs three times since July, when rates stood at 0.75%. In the recent weeks, investors have been paring back the odds of a potential rate hike since the economy seemed to lose momentum in times when the government was struggling to reach an agreement on the NAFTA front. GDP growth slowed down surprisingly to 1.7% y/y in the final quarter of 2017, following a downward revision in the Q3 measure, while it was a big surprise to see employment declining sharply in January. Trump’s punitive import tariffs on steel could be another reason for the BoC to leave monetary policy unchanged today as Canada owns the largest share of steel imports to the US and any implementation of the measures could exaggerate trade conflicts between the countries and make NAFTA negotiations much more difficult. While markets are already waiting for the BoC to hold a cautious tone given the above risks, a larger degree of pessimism in the central bank’s outlook could push the loonie lower.

Canadian trade statistics for the month of January will be also available today prior the rate decision at 1330 GMT.

Meanwhile in the US, investors will keep a close eye on the ADP nonfarm employment report due at 1315 GMT before they prepare their positions ahead of the famous nonfarm payrolls on Friday. According to analysts, the ADP readings which regard the US private sector are expected to show an employment increase of 195,000 in February compared to 234,000 seen in the previous month. Government’s nonfarm payrolls which track changes in both the private and public labor sectors are anticipated to stand flat at 200,000.

In other data out of the US, the Fed’s Beige Book will give an overview of the current economic conditions in each of the 12 Federal districts at 1900 GMT, while the Energy Information Administration will publish its weekly report on US oil inventories earlier at 1530 GMT.

Elsewhere, Japan will see the release of the GDP growth figures for the final quarter of 2017 at 2350 GMT. However, these will be the second estimates and are likely to have a moderate impact on the yen. Forecasts continue to support a growth rate of 0.9% y/y, although first GDP growth estimates came in lower at 0.5%. Data on private consumption and capital expenditure will also attract some attention.

As for today’s speakers, we will hear from Atlanta Fed President Raphael Bostic (voter), as well as New York Fed President William Dudley (voter), at 1300 GMT and 1320 GMT respectively.