{kind=link}

The forex markets are pretty steady in Asian session as an extremely busy week starts. Reactions to Italy election and Germany SPD vote on grand coalition were muted. Euro remains steady so far, staying as the second strongest major currency for the month after Yen. Canadian Dollar and Australian Dollar remain the weakest ones for the month. Asian stocks are weak, however, with Nikkei trading down -0.8%, HK HSI down -1.3% at the time of writing. Investors are cautious and US President Trump continued to step up his words on trade wars.

Trump: EU has been brutal to us

Trump counter-attacked on EU’s criticism on his steel and aluminum tariff. He tweeted again during the weekend that the European Union has been “brutal to us”. And he warned that “if the E.U. wants to further increase their already massive tariffs and barriers on U.S. companies doing business there, we will simply apply a Tax on their Cars which freely pour into the U.S.”

That was in reaction to European Commission President Jean-Claude Juncker’s statement that “we will not sit idly while our industry is hit with unfair measures that put thousands of European jobs at risk.

Trump’s advisor Navarro: Tariffs exemption possible, but no exclusion

White House Director of the National Trade Council, Peter Navarro commented on Trumps’ tariffs on Sunday: He said exemptions and exclusions are different. And, “there’ll be an exemption procedure for particular cases where you need to have exemptions so that business can move forward.” However, “at this point in time, there’ll be no country exclusions.” Navarro added that “As soon as he (Trump) starts exempting countries, he has to raise the tariff on everybody else.” And, “as soon as he exempts one country, his phone starts ringing with the heads of state of other countries.”

Trump is expected to formally sign an order for the 25% tariff on steel and 10% on aluminum this week, or next week latest.

No clear winner in Italy election

In Italy, based on the early vote counts, there will be no clear winner in the election. Center-right coalition of former Primer Minister Silvio Berlusconi is heading for a win in the election, but falls short of a majority. That means, it will take weeks of negotiations before a government could be formed. Anti-establishment Five Star movements to come in second place. Center-left coalition by the governing Democratic Party will come in third.

SPD approved grand coalition, Merkel secured fourth term

Angela Merkel secured her fourth term as Chancellor of Germany. Members of the Social Democrats voted for the coalition deal with Merkels’ CDU/CSU. Months of political uncertainty has now ended. The SPD’s vote results were overwhelming, with 66% supporting, and only 34% rejecting.

On the data front

China Caixin PMI services dropped 0.5 to 54.2 in February. Australia TD securities inflation dropped -0.1% mom in February. Australia building approvals rose 17.1% mom in January. Main focuses in European session is on UK PMI services. Eurozone will also release Sentix investor confidence, retail sales and PMI services revisions. Later in the day, US will release ISM non-manufacturing composite.

The week ahead

For the week ahead, RBA, BOC, ECB and BoJ would have monetary policy meetings, scheduled on Tuesday, Wednesday and Thursday, Friday respectively. RBA is widely expected to keep interest rate unchanged at 0.50%. Governor Philip Lowe and other policymakers have been clear in their neutral stance. RBA is not going to follow other global central banks for tightening. NAB recently adjusted their expectation to just one RBA hike this year, not two. Westpac maintained their forecast that RBA will be on hold throughout this year.

For BOC, the biggest uncertainty on the economic outlook is undoubtedly future trade relations with the US, in particulate NAFTA negotiations. Also, it should be noted again that Canada is the biggest steel importer to the US. And the newly to be imposed tariff could give the country’s economy another blow. BoC is not expected to hike again until the picture becomes clear.

As such, the central bank would be cautious over rate hike decisions. ECB would also maintain its rates and QE program unchanged. However, the focus is the timing for changing the forward guidance. The language in the accompanying statement and President Mario Draghi’s comments at the press conference would be closely watched. For now, it’s expected that ECB officials will discuss tweaking the languages, but hold it for June meeting. So Euro bulls could be disappointed out of the meeting.

On the dataflow, the focus is on US employment report due Friday. Non-farm payrolls probably increased 205K in February, up modestly from January’s 200K. The unemployment rate probably slid -0.1 percentage point to a new low of 4%. Average hourly earnings might have grown 0.2% m/m in February, easing from 0.3% in the prior month. Scheduled for release on the same day is Canada’s employment situation. The number of employment probably increased 21K in February, after contracting -88K a month ago. The unemployment rate might have stayed unchanged at 5.9%.

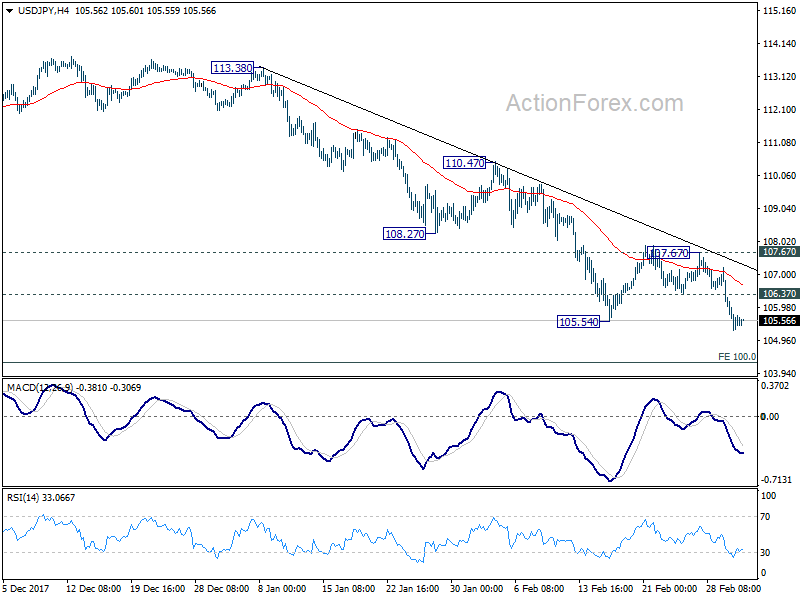

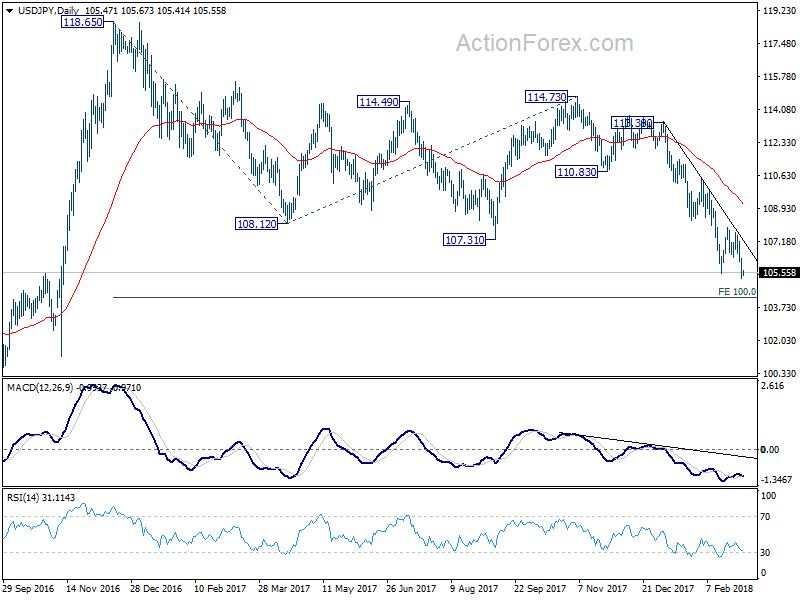

USD/JPY Daily Outlook

Daily Pivots: (S1) 105.20; (P) 105.75; (R1) 106.25; More…

Intraday bias in USD/JPY remains on the downside for the moment. Down trend from 118.65 has just resumed and should target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. Firm break there will target 98.97 key support level. On the upside, above 106.37 minor resistance will turn bias neutral first. But outlook will remain bearish as long as 107.67 resistance holds.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | AUD | TD Securities Inflation M/M Feb | -0.10% | 0.30% | ||

| 0:30 | AUD | Building Approvals M/M Jan | 17.10% | 5.00% | -20.00% | -20.60% |

| 1:45 | CNY | Caixin PMI Services Feb | 54.2 | 54.3 | 54.7 | |

| 8:45 | EUR | Italy Services PMI Feb | 57 | 57.7 | ||

| 8:50 | EUR | France Services PMI Feb F | 57.9 | 57.9 | ||

| 8:55 | EUR | Germany Services PMI Feb F | 55.3 | 55.3 | ||

| 9:00 | EUR | Eurozone Services PMI Feb F | 56.7 | 56.7 | ||

| 9:30 | GBP | Services PMI Feb | 53.3 | 53 | ||

| 9:30 | EUR | Eurozone Sentix Investor Confidence Mar | 30.9 | 31.9 | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Jan | -0.10% | -1.10% | ||

| 14:45 | USD | US Services PMI Feb F | 55.9 | 55.9 | ||

| 15:00 | USD | ISM Non-Manufacturing/Services Composite Feb | 59 | 59.9 |