{kind=link}

Stocks suffered another round of steep selloff overnight. DOW dropped more than -1000 pts for the second time in just four days, scoring the second biggest point drop ever. DOW lost -1035.89 pts, or -4.15% to close at 23860.46. This week’s low at 23778.74 was not breached yet. But it looks vulnerable as two other major indices made new lows already. S&P 500 lost -100.66 pts or -3.75% to close at 2581.0, below prior weekly low at 2593.07. NASDAQ dropped -274.82 pts or -3.9% to 6777.16, also below prior weekly low at 6824.82. That is, recent selloff is resuming and the indices will likely head further lower before closing the week. In Asian markets, Nikkei follows by losing -3.2% at the time of writing, HK HSI is down -3.65%.

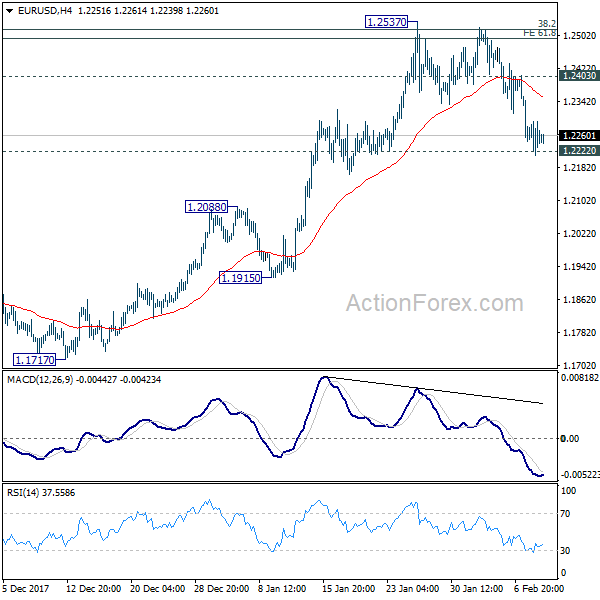

In the currency markets, Yen is leading the way up, followed by Dollar as the second strongest for the week. Aussie is the worst performer, followed by Euro, Canadian and Kiwi. Sterling is mixed as it got some boost from yesterday’s hawkish BoE announcement. Technically, 1.2222 is EUR/USD is the key level to watch today. The pair breached this level briefly yesterday but quickly turned sideway. Firm break of 1.2222 will be a strong sign of rejection of 1.2516 long term fibonacci resistance and trend reversal.

Fed George: Three hikes a reasonable baseline

Kansas City Fed President Esther George warned that the impact of the government’s fiscal stimulus on the economy is uncertain. In the background, the labor market appears to be tight, and inflation risks are on the rise. Therefore, "it is important that the [Fed] continues on its current path of policy normalization with gradual increases in the target federal funds rate." She added that rates are important to "sustain the expansion without pushing the economy beyond its capacity limits and creating inflationary pressures." And, in her view, three hikes this year is "a reasonable baseline unless the outlook changes materially."

RBA lowered unemployment forecast

In the monetary statement published today, RBA lowered unemployment rate forecasts but kept projections on growth and inflation unchanged. Year average GDP growth is projected to be at 3% in 2018 and 3.25% in 2019. CPI is projected to be at 2.25% by the end of 2018 and stay at 2.25% by the end of 2019. Unemployment rate, though, is forecast to drop from current 5.5% to 5.25% by the end of 2018, revised down from 5.50%. Unemployment is forecast to stay at 5.25% till end of 2019.

RBA noted that "financial market volatility has picked up in recent days, most notably in equity markets as market participants have begun to reassess the outlook for global inflation and the withdrawal of monetary accommodation". And, "an important consideration for the outlook is how far inflation picks up as the global economy strengthens." It added that "a larger-than-expected increase in inflation would have implications both for financial market pricing and exchange rates."

Also from Australia, home loans dropped more than expected by -2.3% mom in December.

Elsewhere

Japan M2 rose 3.4% yoy in January. China CPI slowed to 1.5% yoy in January, PPI slowed to 4.3% yoy. Swiss will release unemployment rate in European session. But main focus will be on UK data, where productions and trade balance are featured. Later in the data, Canada employment will take center stage.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2207; (P) 1.2250 (R1) 1.2290; More….

EUR/USD breached 1.222 key support but there is no follow through selling yet. Nonetheless, there is also no sign of bottoming and intraday bias remains on the downside. Sustained break of 1.2222 should confirm rejection from 1.2494/2516 key fibonacci level, as well as near term reversal, on bearish divergence condition in 4 hour MACD. That could also signal completion of medium term up trend from 1.0339. In that case, near term outlook will be turned bearish for 1.2091 resistance turned support first. On the upside, though, above 1.2403 minor resistance will revive bullishness and turn focus back to 1.2537.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. But key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is looking vulnerable. Sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862. Nonetheless, rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Jan | 3.40% | 3.60% | 3.60% | |

| 00:30 | AUD | Home Loans M/M Dec | -2.30% | -1.00% | 2.10% | 1.60% |

| 00:30 | AUD | RBA Monetary Policy Statement | ||||

| 01:30 | CNY | CPI Y/Y Jan | 1.50% | 1.50% | 1.80% | |

| 01:30 | CNY | PPI Y/Y Jan | 4.30% | 4.20% | 4.90% | |

| 04:30 | JPY | Tertiary Industry Index M/M Dec | 0.10% | 1.10% | ||

| 06:45 | CHF | Unemployment Rate Jan | 3.00% | 3.00% | ||

| 09:30 | GBP | Industrial Production M/M Dec | -0.90% | 0.40% | ||

| 09:30 | GBP | Industrial Production Y/Y Dec | 0.40% | 2.50% | ||

| 09:30 | GBP | Manufacturing Production M/M Dec | 0.30% | 0.40% | ||

| 09:30 | GBP | Manufacturing Production Y/Y Dec | 1.20% | 3.50% | ||

| 09:30 | GBP | Construction Output M/M Dec | -0.10% | 0.40% | ||

| 09:30 | GBP | Visible Trade Balance (GBP) Dec | -11.5B | -12.2B | ||

| 12:00 | GBP | NIESR GDP Estimate Jan | 0.50% | 0.60% | ||

| 13:30 | CAD | Net Change in Employment Jan | 10K | 78.6K | ||

| 13:30 | CAD | Unemployment Rate Jan | 5.80% | 5.70% | ||

| 15:00 | USD | Wholesale Inventories M/M Dec F | 0.20% | 0.20% |