{kind=link}

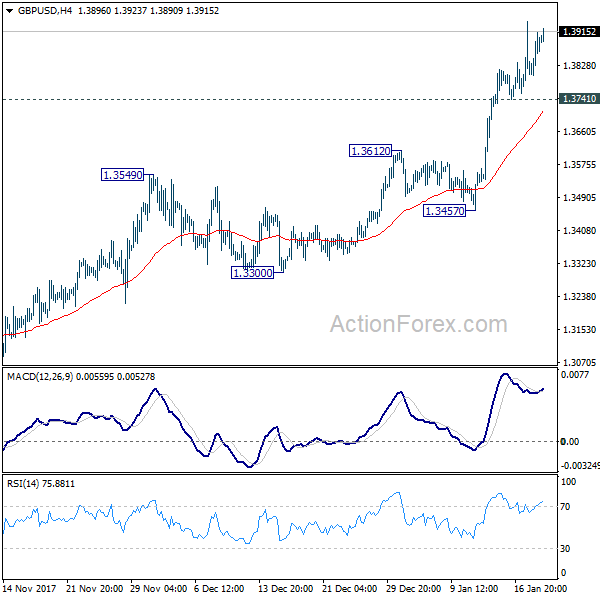

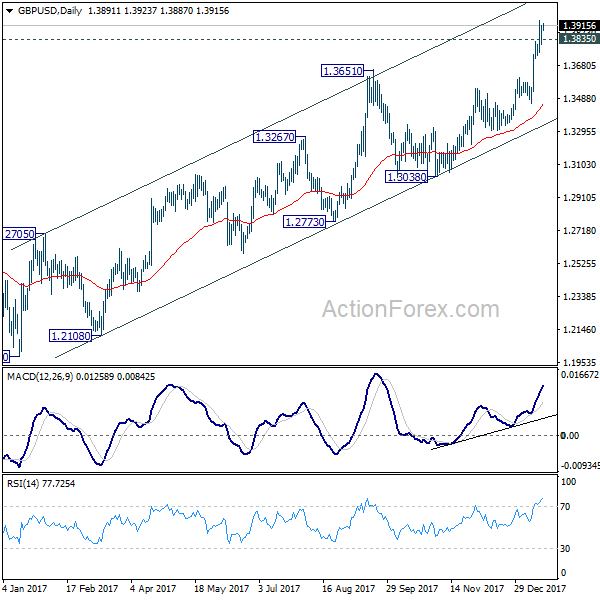

Sterling continues to trade as the strongest major currency for the week. Fundamentally, focus will turn to retail sales data to be published today. Technically, GBP/USD should have already taken out 1.3835 key resistance. GBP/JPY also broken 153.66 near term resistance for rally resumption. The next to be watched is 0.8688 support in EUR/GBP, which is still a bit far away from the current 0.8810 level.

Dollar on the other hand, is trading as the weakest one as diversification theme is in play. Other markets in the US are looking good. DOW reached record intraday high at 26153.42 before closing lower by -0.37% at 26017.81. The lost of momentum is not unusual considering the strength of recent rise. 10 year yield closed up 0.33 at 2.611. And 2.621 key resistance (2016 high) is finally in sight. In usual circumstances, we’d expect strength in yield to support the greenback. But it remains to be seen when the two will re-couple.

San Francisco Fed William in race for Fed Vice

San Francisco Fed president John Williams appear to be a funning for the position of Vice Chair of Fed, to fill up the vacancy left by Stanley Fischer. Williams said it’s would be a "great honor" to be number two under Jerome Powell. And he "welcome such an opportunity to contribute to the important mission of the Fed.

House approved bill to avoid government shut down

The US House approved the bill to avoid government shutdown on Thursday night. The final vote was 230-197, with 6 Democrats voting for the bill and 11 Republicans against it. Vote in the Senate is delayed to Friday but that should just be procedural.

Aussie strong on rate hike bets

Australian dollar’s recent strength can be explained by investors’ expectation of RBA tightening ahead. While the central bank continued to sound neutral in its communications, the bond markets are telling another story. The spread between 3 year bond yield and RBA policy rate jumped to 75 basis points today, hitting the widest level since May 2010. That comes after another month of stellar job data released earlier in the week. The strong setting to the start of 2018 could be putting up pressure for the RBA to follow other global peers to hike later in the year.

New Zealand manufacturing PMI tumbled sharply

New Zealand business NZ manufacturing PMI dropped sharply to 51.2 in December, down from 57.7. While it still stayed above 50 which signals expansions, the slowdown is notable. Looking in to the details, all five of the sub-indices declined with the biggest fall seen in new orders, from 57.3 to 50.2. BNZ noted that "anecdotal evidence, across the economy, suggests there was a post-election hiccup in activity as businesses put off major spending."

But overall, the data does little to hinder recent rally in NZD/USD, which rides on dollar’s weakness. Now with 61.8% retracement of 0.7557 to 0.6779 taken out, the pair should be targeting 0.7432/7557 resistance zone. There is no clear sign of resumption of long term rise from 0.6102 (2015 low) yet. Hence, we’ll pay attention to topping signal in this resistance zone.

Looking ahead

German PPI, Eurozone current account and Swiss PPI will be released in European session. But the main feature will be UK retail sales. Canada will release manufacturing sales and international securities transactions and US will release U of Michigan sentiment later in the day.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3826; (P) 1.3869; (R1) 1.3936; More…..

Intraday bias in GBP/USD remains on the upside at this point. As noted before, sustained trading above 1.3835 will carry larger bullish implication and should target long term fibonacci level at 1.5466 next. On the downside, though, break of 1.3741 minor support will indicate rejection from 1.3835 and turn bias to the downside for 1.3457.

In the bigger picture, sustained break of 1.3835 key resistance level will indicate that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. In that case, further rise should be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Nonetheless, rejection from 1.3835 will maintain medium term bearishness and thus, the risk retesting 1.1946 ahead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ Manufacturing PMI Dec | 51.2 | 57.7 | ||

| 7:00 | EUR | German PPI M/M Dec | 0.20% | 0.10% | ||

| 7:00 | EUR | German PPI Y/Y Dec | 2.30% | 2.50% | ||

| 8:15 | CHF | Producer & Import Prices M/M Dec | 0.60% | |||

| 8:15 | CHF | Producer & Import Prices Y/Y Dec | 1.80% | |||

| 9:00 | EUR | Eurozone Current Account (EUR) Nov | 31.3B | 30.8B | ||

| 9:30 | GBP | Retail SalesM/M Dec | -0.90% | 1.10% | ||

| 13:30 | CAD | Manufacturing Sales M/M Nov | 2.00% | -0.40% | ||

| 13:30 | CAD | International Securities Transactions (CAD) Nov | 20.81B | |||

| 15:00 | USD | U. of Mich. Sentiment (JAN P) | 97 | 95.9 |