{kind=link}

Here are the latest developments in global markets:

FOREX: The US currency was on its fourth straight day of declines, with the dollar index falling to its lowest in two years as other majors were boosted on hopes of policy normalization on behalf of their respective central banks. The Chinese currency recorded a two-year high versus the greenback as the PBOC altered its rate fixing to the dollar.

STOCKS: The Japanese Nikkei 225 closed 0.3% higher even as the yen kept strengthening versus the dollar, with dollar/yen at one point hitting its lowest since mid-September. Hong Kong’s Hang Seng was 0.3% down after previously rising as much as 1% to hit a fresh decade high. Euro Stoxx 50 futures traded 0.1% higher at 0741 GMT. Meanwhile, Dow, S&P 500 and Nasdaq 100 contracts were up by 0.3%, 0.1% and 0.1% respectively. US markets will be closed on Monday for Martin Luther King Jr. Day.

COMMODITIES: WTI and Brent crude were not much changed, trading at $64.38 and $69.84 per barrel respectively, not far below the recently tracked three-year highs. Gold continued gaining on the back of dollar weakness. The precious metal was up by 0.2% after touching $1,344.44 per ounce, its highest since early September.

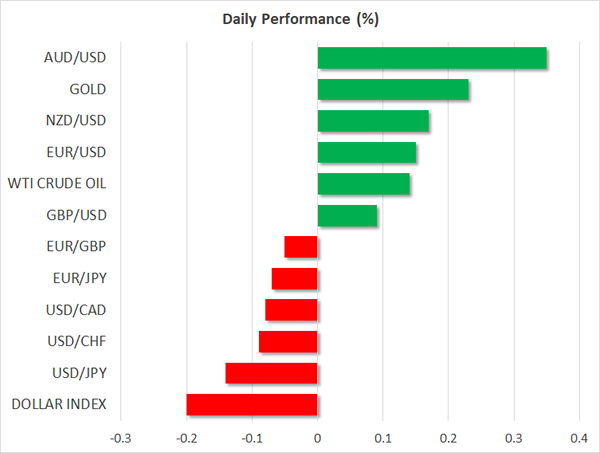

Major movers: Dollar weaker across the board; euro records fresh 3-year high versus greenback

The dollar kept retreating versus a basket of currencies, with the dollar index touching 90.62 at its lowest, a level last experienced in January 2015. The euro and the yen continued posting gains relative to the greenback, buoyed by what some market participants perceived as rising prospects for the European Central Bank and the Bank of Japan to scale back their easy monetary policies; a speech by BoJ Governor Haruhiko Kuroda also stressed that Japan is on a path of recovery, while adding that core consumer prices are picking up. Euro/dollar touched 1.2240 at one point, its highest since late 2014, and dollar/yen fell as low as 110.54, a level last experienced on September 15.

The US currency was weaker across the board. Pound/dollar recorded its highest since mid-2016 of 1.3767; sterling was bolstered late last week after reports suggested that Spain and the Netherlands were supportive of a Brexit deal that allows the UK to remain as close as possible to the EU. Despite officials from the two countries not backing the claims, the British currency remained boosted. Aussie/dollar reached its highest since late September of 0.7960 as optimism about global growth is spurring hopes that commodity prices will remain elevated. Kiwi/dollar hit 0.7282, a level last seen in late September.

Adding insult to injury, the yuan touched a two-year high versus the US currency – dollar/yuan fell as low as 6.4140 – after the People’s Bank of China raised the currency’s reference rate to the highest since May 2016, at 6.4574 per dollar. The Bundesbank – the German central bank – also decided to include the yuan in its reserves.

Day ahead: Kiwi waits for New Zealand’s business confidence and electronic retail sales

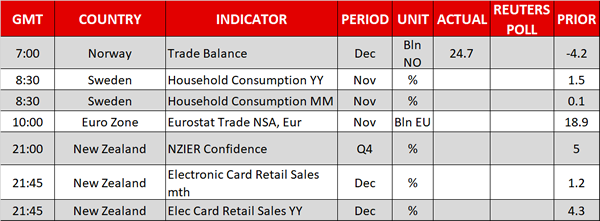

Monday will be a relatively quiet day in terms of data releases. Kiwi traders though will be waiting for updates on New Zealand’s business confidence (2100 GMT) and electronic card retail sales (2145 GMT). In the US, markets will be shut for Martin Luther King Jr. Day.

Regarding New Zealand’s business confidence, it will be interesting to see whether the business outlook continued to deteriorate in the fourth quarter of 2017 as the index has been slowing down since the beginning of the year when it touched a 2½-year high. In the third quarter, the measure hit the lowest growth mark seen in 2017, rising by 5.0%.

On the other hand, electronic transactions in New Zealand increasingly grew from September onwards, reaching a 10-month high of 1.2% m/m in December. If the measure continues to extend its uptrend, this would mirror further improvements in consumption and constitute a positive contribution to the country’s economic expansion.

Political developments in Germany would attract attention the following weeks after Merkel’s Conservatives managed to make progress on coalition talks with their former partners, the Social Democrats. The Social Democrats said on Sunday they would make efforts to improve the blueprint and gain the trust of their skeptical members, hoping for a deal at a congressional meeting on January 21, when a vote on the agreement will take place. Formal negotiations will be able to start only if the vote is positive.

Investors will also keep a close eye on several earnings reports due this week, which have the potential to lead to stock market positioning.

Technical Analysis: NZDUSD increasingly bullish but overbought

NZDUSD holds a bullish bias in the short-term. However, a pullback might take place in the short-term given that the RSI is currently located in overbought zone above 70.

In case New Zealand releases surprise to the upside, immediate resistance could be met at the 78.6% Fibonacci at 72.93 of the downleg from a more than a two-year high of 0.7433 to a low of 0.6779 (September – November). Further increases could also test the 0.7350, which was a congested area in the past, and the previous peak of 0.7433.

On the flip side, if figures disappoint, support could come first around the 61.8% Fibonacci at 0.7182 and then a stronger obstacle could be found at the 50% Fibonacci at 0.7105 where the 20- and the 200-day MA are currently located.