{kind=link}

Dollar remains generally strong today, but it’s over powered by Sterling. The Pound is lifted by optimism that Brexit negotiation is finally close to completing the first phase. It’s reported that the Irish border issue is solved with UK Prime Minister Theresa May’s new proposal. And she’s flying to Brussels again today to complete the talks. Dollar will look into today’s non-farm payroll report for the fuel for further rally. Elsewhere in the currency markets, Yen and Swiss Franc are trading as the weakest ones today.

NFP expected to grow 200k, eyes on wage growth

Economists are expecting NFP to show 200k growth in November. Unemployment is expected to be unchanged at 4.1%. Average hourly earnings are expected to rise 0.3% mom. Looking at other employment related data, ADP report showed 190k growth in private jobs, down fro October’s 235k. ISM manufacturing employment dropped 0.1 to 59.7. ISM non-manufacturing employment dropped 2.2 to 55.3. Four week average of initial jobless claims rose 11k to 242k. Continuing claims rose 0.01m to 1.91m. Conference board consumer confidence improved to 129.5, hitting the highest level since December 2000.

Overall, job related data pointed to rather healthy underlying growth momentum. And, 200k headline NFP should be easily met. The surprises today could be found in unemployment rate which may dropped further. And more importantly, wage growth would be the key market driver. Considering that average hourly earnings growth was at 0.0% mom back in October, a 0.3% mom growth in November looks achievable.

Technically, Dollar is looking very firm against Aussie, Canadian and Swiss Franc. USD/JPY’s break of 113.08 overnight also suggests underlying upside momentum and would likely target 114.73 resistance again. However, GBP/USD managed to rebound strongly after breaching 1.3337 support. And that’ should resilience of Sterling. The bigger question lies in EUR/USD which is holding above 1.1712 support and maintains bullishness. However, in case of dollar rally after NFP, firm break of 1.1712 will align EUR/USD with other dollar pairs expect GBP/USD. In that case, we’ll likely see Dollar gains broad based momentum.

US Congress passed two week funding extension

US Congress passed two-week extension of federal funding that avoids a partial government shutdown this week. House voted 235 to 193 for the extension while Senate voted 81 to 14. This gives lawmakers a bit more time to finish the work on spending and legislation till December 22. At the same time, they will also be working on the tax reform, rushing to reconcile the differences between House and Senate version, and pass them in respective chambers before year end holidays.

Brexit negotiations close to complete first phase, May to meet Juncker

Quick update: Juncker declared that "sufficient progress has now been made on the three terms of the divorce." And negotiation can move on to trade agreements.

UK Prime Minister Theresa May would likely rush to Brussels today and meet European Commission President Jean-Claude Juncker at around 7am local time to resume Brexit negotiations. It’s reported that after a night of intensive talk and phone calls, May is closing on a deal on Irish border, with support from her Northern Ireland partner DUP. The second issue on divorce bill should have been agreed for some time already. Meanwhile, it’s believed that UK and EU have also agreed on the third issue, the role of European Court of Justice in British legal cases after Brexit. So, Brexit negotiation should be ready to move on to the next stage of trade talks.

Sterling was given a boost in Asian session today. In particular, EUR/GBP has taken out 0.8732 support to finally resume recent decline from 0.9305. GBP/JPY also broke 152.93 to resume the rise from 139.29. Pound traders will now eagerly await the post meeting press briefing of May and Juncker to confirm this optimism.

Japan GDP grew 0.6% qoq in Q3, doubled initial estimate

Japan GDP growth was finalized at 0.6% qoq in Q3, double the pace of initial estimate of 0.3% qoq. Annualized rate was 2.5%. GDP deflator was finalized at 0.1% yoy, unchanged. The data showed that Abenomics and BoJ’s easing have definite boosted growth, but is so far having little impact on lifting inflation. Also from Japan current account surplus widened to JPY 2.44T in October. Labor cash earnings rose 0.6% yoy, below expectation of 0.8% yoy.

China trade surplus widened to USD 40.2b in November, up from USD 38.2b and above expectation of USD 34.9b.Exports rose 12.3% yoy while imports also surged 18% yoy. In Yuan, trade surplus widened to CNY 264b, up fro CNY 254b and beat expectation of CNY 238b. Also from Asia Pacific, Australia home loans dropped -0.6% mom in October. New Zealand manufacturing activity rose 0.5% in Q3.

Looking ahead

UK trade balance, productions and German trade balance are the main features in European session. US will release NFP and U of Michigan sentiment. Canada will release housing starts.

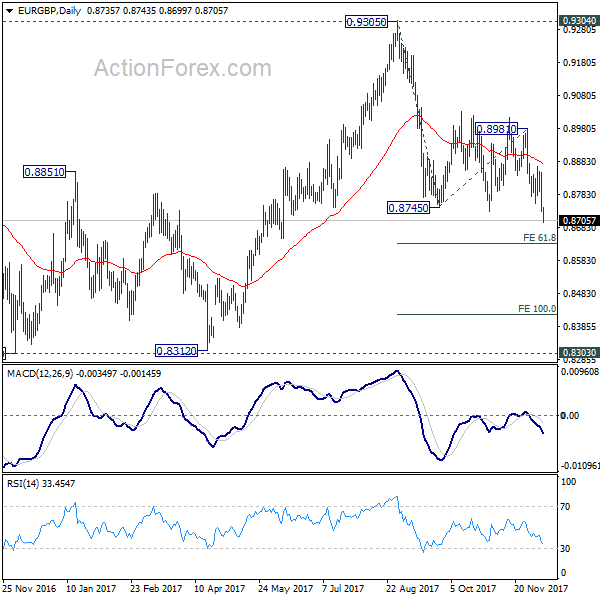

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8696; (P) 0.8773; (R1) 0.8812; More…

EUR/GBP drops sharply to as low as 0.8699 so far. Firm break of 0.8732 support finally confirms resumption of fall from 0.9305. Intraday bias is back on the downside for 61.8% projection of 0.9305 to 0.8745 from 0.8981 at 0.8468 first. Break will target 100% projection at 0.8151 next. On the upside, break of 0.8849 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we’d expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Activity Q3 | 0.50% | 3.90% | 3.40% | |

| 23:50 | JPY | Current Account (JPY) Oct | 2.44T | 1.93T | 1.84T | |

| 23:50 | JPY | GDP Q/Q Q3 F | 0.60% | 0.40% | 0.30% | |

| 23:50 | JPY | GDP Deflator Y/Y Q3 F | 0.10% | 0.10% | 0.10% | |

| 0:00 | JPY | Labor Cash Earnings Y/Y Oct | 0.60% | 0.80% | 0.90% | |

| 0:30 | AUD | Home Loans M/M Oct | -0.60% | -2.00% | -2.30% | -2.50% |

| 3:13 | CNY | Trade Balance (CNY) Nov | 264B | 238B | 254B | |

| 3:36 | CNY | Trade Balance (USD) Nov | 40.2B | 34.9B | 38.2B | |

| 7:00 | EUR | German Trade Balance (EUR) Oct | 22.3B | 21.8B | ||

| 9:30 | GBP | Industrial Production M/M Oct | 0.00% | 0.70% | ||

| 9:30 | GBP | Industrial Production Y/Y Oct | 3.50% | 2.50% | ||

| 9:30 | GBP | Manufacturing Production M/M Oct | 0.00% | 0.70% | ||

| 9:30 | GBP | Manufacturing Production Y/Y Oct | 3.80% | 2.70% | ||

| 9:30 | GBP | Construction Output M/M Oct | 0.10% | -1.60% | ||

| 9:30 | GBP | Visible Trade Balance (GBP) Oct | -11.5B | -11.3B | ||

| 13:00 | GBP | NIESR GDP Estimate Nov | 0.40% | 0.50% | ||

| 13:15 | CAD | Housing Starts Nov | 221K | 223K | ||

| 13:30 | CAD | Capacity Utilization Rate Q3 | 85.20% | 85.00% | ||

| 13:30 | USD | Change in Non-farm Payrolls Nov | 200K | 261K | ||

| 13:30 | USD | Unemployment Rate Nov | 4.10% | 4.10% | ||

| 13:30 | USD | Average Hourly Earnings M/M Nov | 0.30% | 0.00% | ||

| 15:00 | USD | U. of Mich. Sentiment (Dec P) | 99 | 98.5 |