{kind=link}

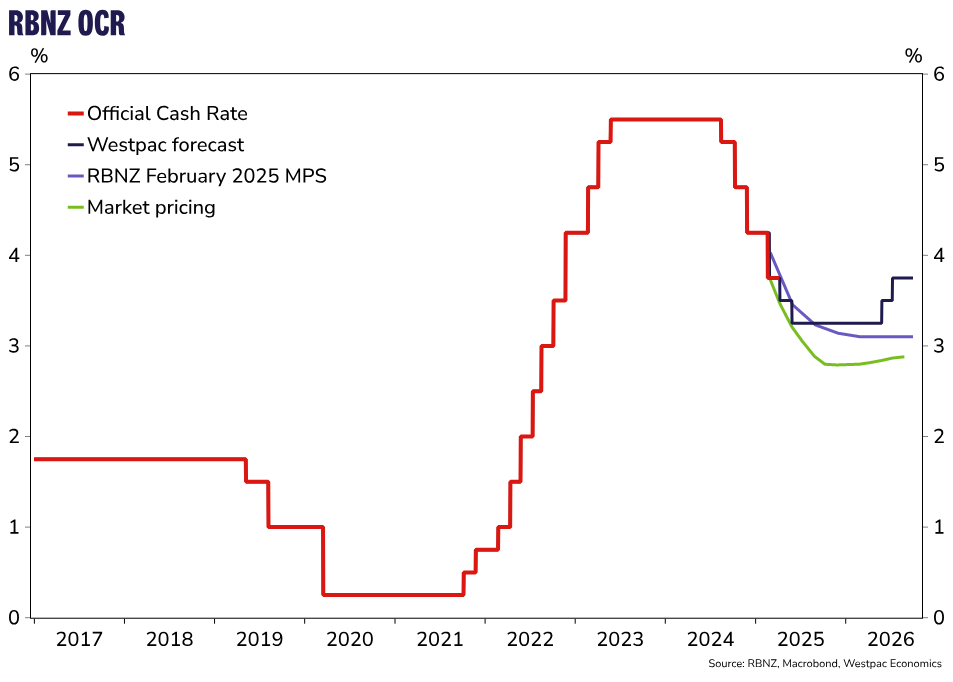

We continue to see the RBNZ cutting the OCR 25bp to 3.5% tomorrow. But the risks around the outlook have increased, especially due to the darkening global outlook.

Key points:

- We continue to see the RBNZ cutting the OCR 25bps to 3.5% tomorrow.

- Today’s sluggish QSBO and the darkening global outlook imply a less positive forward economic view.

- There are risks of a larger cut – but uncertainties should see the RBNZ keep that powder dry.

- We expect commentary indicating a firm intention to get the OCR to 3% soon.

- The risks of a sub 3% OCR are real, but no judgement will be made on that tomorrow.

Recent developments

Last Wednesday we released our Monetary Policy Review preview, and we forecast a 25bps cut in the OCR to 3.5%. We also indicated a risk of a pause to allow the RBNZ to assess the impacts of past easing. The balance of risks has shifted a lot in just one week. Hence, it’s important to update the view.

Markets have moved to price in risks of a much lower OCR over 2025 as the bomb that the US administration detonated on global trade reverberates. The news of rounds of retaliation between China and the US imply very elevated global growth risks. And that bodes poorly for the New Zealand outlook.

Today we also received the results of one of the more reliable domestic business surveys. We expected a decent bounce in activity indicators and an increase in pricing pressures. In actuality, the growth indicators still look fairly flat. Our GDP Nowcast indicator for Q1 GDP growth was pinned back to around 0.2% – somewhat weaker than our 0.4% forecast and certainly lower than the RBNZ’s 0.6% expectation.

We continue to expect the RBNZ to cut the OCR 25bps to 3.5% tomorrow. But the balance of risks lies clearly to the downside now – especially after the April MPR.

There are a wide range of outcomes for New Zealand interest and exchange rates from here. It’s likely the RBNZ will feel very keen to get the OCR to their estimate of neutral of 3% soon. They will likely indicate this intention in tomorrow’s statement. The meeting statement of record will also likely contain a discussion on the potential need to take the OCR below neutral at some point. But the MPC will likely not draw any conclusions on this point and leave that for discussion at the May Monetary Policy Statement.

In these circumstances the imperative for the central bank is to position policy as well as they can for the uncertainties ahead and ensure financial stability goals are met. We suspect the RBNZ will not want to scare the horses with a large policy shift after being so definitive about a 25bps cut at the February Monetary Policy Statement. Triggering large further falls in interest rate expectations and the exchange rate, both of which have moved in the right direction, and raising speculation that the economic outlook is dramatically weaker would be undesirable.

We suspect the big update will be in May where a wide range of outcomes look more feasible (the RBNZ will know the outcome of Budget 2025 by then also). Of course, the domestic and global outlook could look quite different by then. And the risk genuinely lies in both directions. NZ Inc could come off not too badly when all is said and done – but that doesn’t mean we will win outright either. The RBNZ will likely leave that assessment for May. We will update our own OCR forecasts when we review our forecasts at the May Economic Overview. But there are clear downside risks to our current 3.25% OCR forecast trough.