{kind=link}

Risk appetite in Asian markets has been solid this week, support by optimism surrounding China’s latest measures to boost domestic consumption. Hong Kong stocks continue to lead gains in the region. Meanwhile, in the forex markets, both New Zealand and Australian Dollars are holding firm, though the Aussie is slightly lagging due to rising trade tensions with the US. As tariff threats continue to evolve, the Australian economy is relatively more vulnerable to disruptions in trade, keeping a cap on the currency’s momentum. Meanwhile,

Japanese Yen has weakened notably, weighed down by the prevailing risk-on sentiment in the region. Additionally, traders are solidifying expectations that BoJ will keep rates unchanged in this week’s policy decision, leaving any rate hike for future meetings. Though, any hints from Governor Kazuo Ueda about the timing of future hikes could rejuvenate Yen’s rebound. .

In Europe, attention turns to Germany, where ZEW economic sentiment index is expected to show early signs of optimism surrounding the incoming government’s EUR 500B infrastructure and defense spending plan. Also, Chancellor-in-waiting Friedrich Merz faces a crucial parliamentary vote on this plan today, and while it is broadly expected to pass, there remains an outside risk of legal intervention. The far-right Alternative für Deutschland party has challenged the speed of the legislation’s introduction. Merz might get the court’s verdict soon.

Meanwhile, Canada’s inflation data will be in focus, as markets assess BoC’s next policy steps, which are heavily complicated by trade war. OECD has significantly downgraded Canada’s growth forecast, citing trade war risks and economic fallout from US tariffs. However, OECD also warned of inflationary pressures, suggesting that if Canada faces 25% retaliatory tariffs from the US, borrowing costs could stay higher for longer. This places the BoC in a difficult position, as it must balance slowing growth with the risk of persistent price pressures.

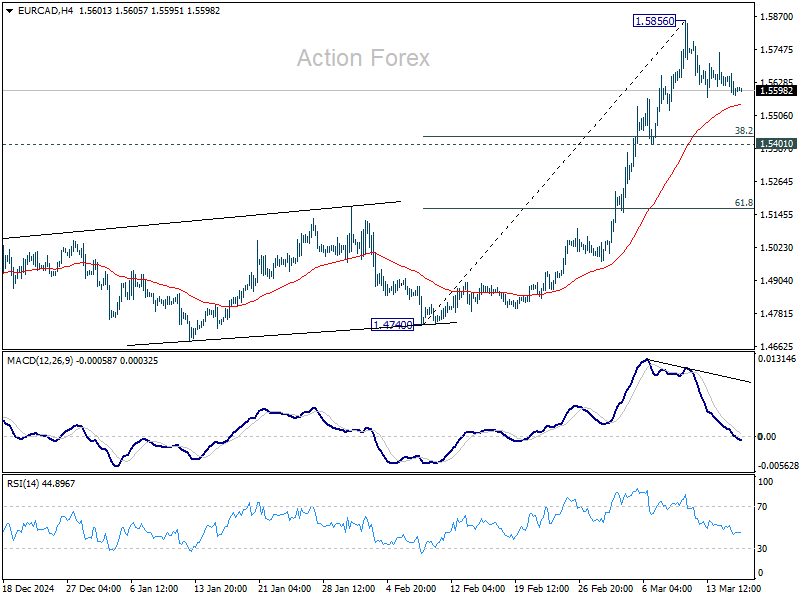

Technically, EUR/CAD should have formed a short term top at 1.5856 on bearish divergence condition in 4H MACD. Deeper retreat might be seen to 55 4H EMA (now at 1.5548). But downside should be contained by 1.5401 cluster support (38.2% retracement of 1.4740 to 1.5856 at 1.5430 to bring rebound. Larger up trend is expected to resume through 1.5856 at a later stage.

In Asia, at the time of writing, Nikkei rose 1.23%. Hong Kong HSI is up 2.12%. China Shanghai SSE is up 0.14%. Singapore Strait Times is up 1.12%. Japan 10-year JGB yield is up 0.0.007 at 1.510. Overnight, DOW rose 0.85%. S&P 500 rose 0.64%. NASDAQ rose 0.31%. 10-year yield fell -0.002 to 4.306.

RBA’s Hunter cautious on further rate cuts, Treasurer warns of trade war’s indirect impacts

RBA Chief Economist and Assistant Governor Sarah Hunter reinforced the central bank’s cautious stance on further rate cuts. She emphasized in a speech today that while the February cut was deemed an appropriate time to “take some restrictiveness away”, the Board were “more cautious than the market about prospects for further easing”.

Hunter highlighted that US policy settings and their impact on the global economy as “one of the things we are focused on right now.

She added that policy decisions are always made in uncertain environments, where the baseline forecast is just one of many possible scenarios rather than a strict roadmap for future moves. The link between economic forecasts and rate decisions is “not mechanical”.

Separately, Australian Treasurer Jim Chalmers acknowledged that the direct impact of US tariffs on Australia is “concerning, but manageable”. But he warned that the larger risk lies in a broader global trade war. He described the current environment as a “new world of uncertainty”, where the spillover effects from rising trade tensions could have far-reaching consequences for Australia’s economy.

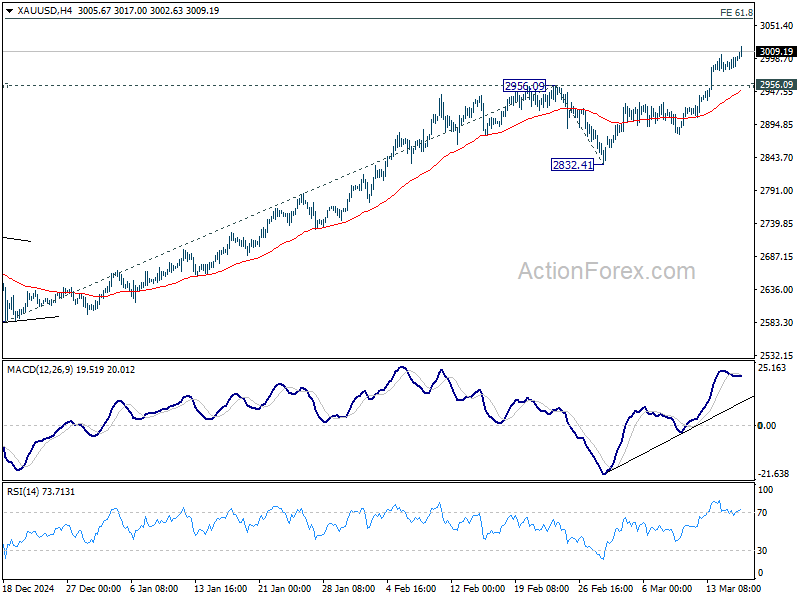

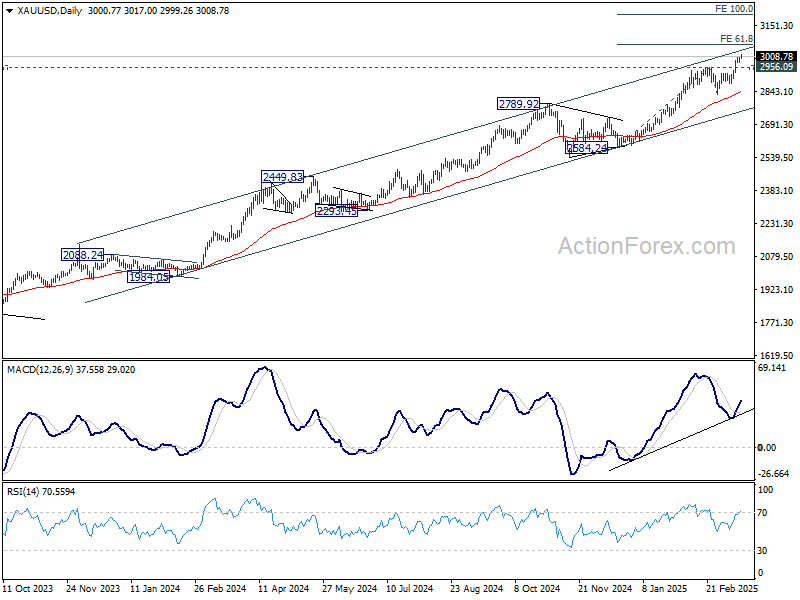

Gold extends record run above 3000 on geopolitical and trade risks

Gold surged further above the 3000 psychological level today, extending its record-breaking rally as geopolitical uncertainty, trade tensions, and global monetary easing continue to fuel demand.

Trade tensions remain front and center with investors are piling into the precious metal ahead of the April 2 deadline, when reciprocal and sectoral tariffs will take effect on US trading partners. US President Donald Trump reinforced his stance, declaring that the new tariffs would mark “liberation day” for the US, with broader reciprocal tariffs and sector-specific duties, particularly on steel and aluminum used in auto production.

Meanwhile, attention is also on Trump’s call with Russian President Vladimir Putin today, where discussions will reportedly cover territorial issues and energy infrastructure, likely including Ukraine’s Zaporizhzhia nuclear plant. Any escalation or breakthrough in these discussions could have broader implications for markets,

Technically, Gold’s up trend remains on track to 61.8% projection of 2584.24 to 2956.09 from 2832.41 at 3062.21. which is close to the medium-term channel resistance.

Rejection by the resistance zone, followed by break of 2956.09 resistance turned support will risk a correction back towards 55 D EMA (now at 2841.83) first.

However, strong break above the channel resistance would prompt acceleration in Gold’s uptrend. In such a scenario, gold could quickly reach 100% projection at 3204.26.

Looking ahead

Swiss SECO economic forecasts, German ZEW economic sentiment, and Eurozone trade balance will be released in European session. Later in the day, Canada CPI will be the main focus. US will publish housing starts and building permits, import prices, and industrial production.

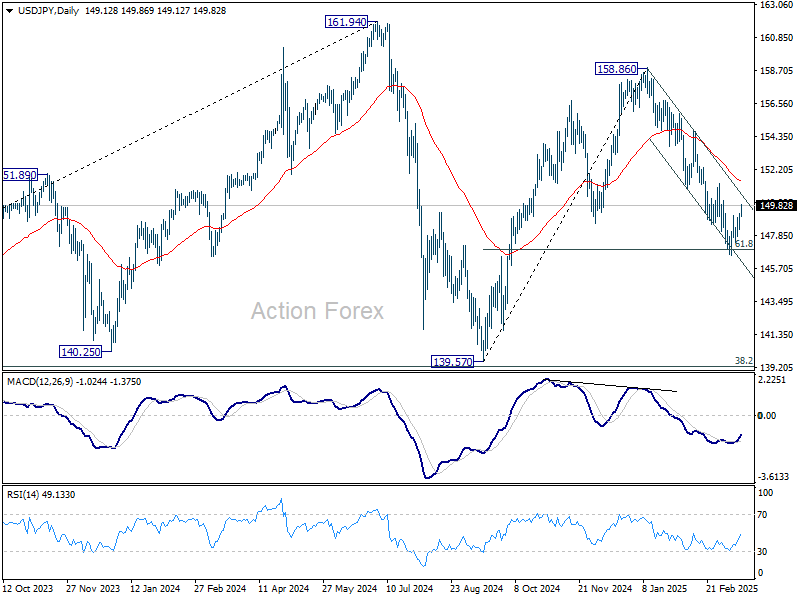

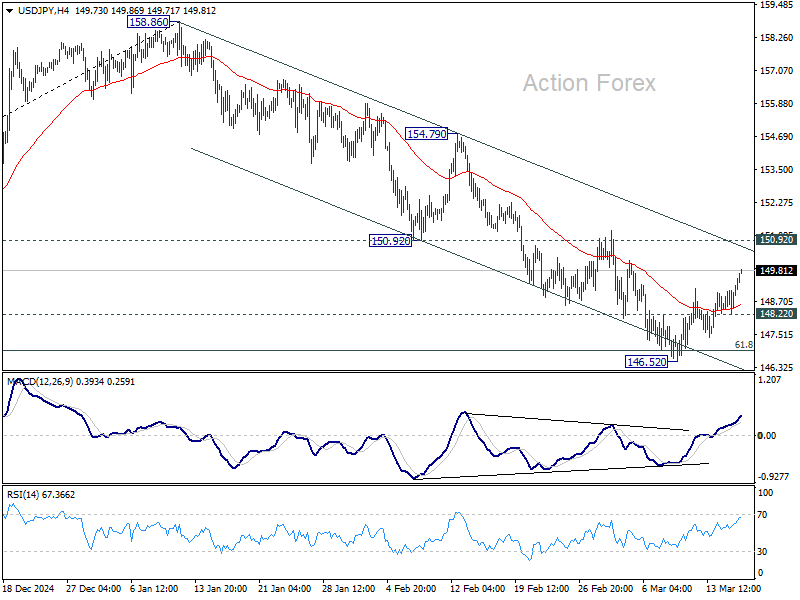

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.89; (P) 148.45; (R1) 149.20; More…

Intraday bias in USD/JPY stays neutral at this point. While recovery from 146.52 might extend further, upside should be limited by 150.92 support turned resistance. On the downside, below 148.22 minor support will bring retest of 146.52 low first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will pave the way to 139.57 support. However, decisive break of 150.92 will dampen this bearish view and turn bias to the upside for 154.79 resistance instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.