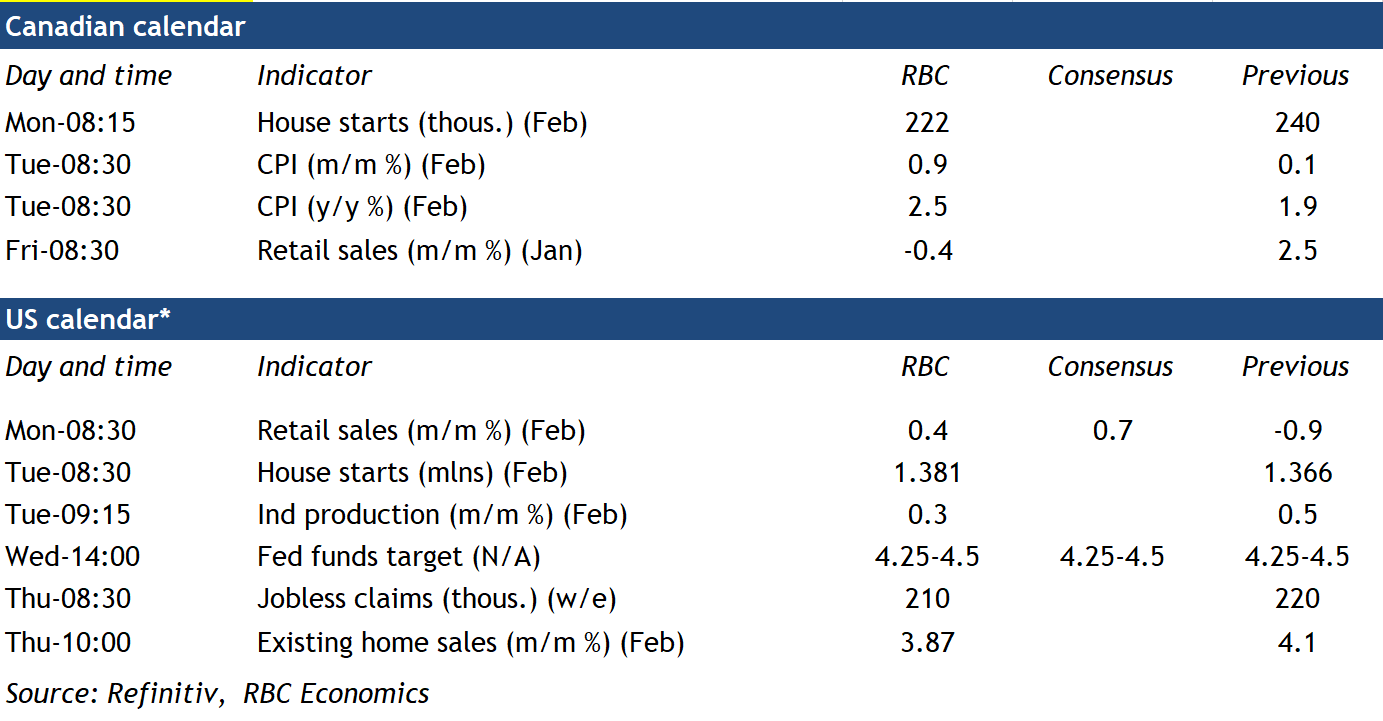

{kind=link}

The balance of risk around the U.S.’s growth may be shifting, but government data still shows a strong economy and that will likely lead the U.S. Federal Reserve to stand pat on interest rates on Wednesday.

At the recent U.S. Monetary Policy Conference in Chicago, Chair Jerome Powell said that “despite elevated levels of uncertainty, the U.S. economy continues to be in a good place.”

Our own forecasts for U.S. GDP growth for 2025 have been marked lower on signs that an 11-quarter run of steady growth may have paused in Q1. The U.S. economy is less sensitive to international trade risks than many of its close trading partners (like Canada), but some sectors, particularly manufacturing, will be negatively impacted by tariff increases.

Still, labour markets look firm. The Trump administration’s DOGE cuts will likely nudge the unemployment rate higher in coming months but we expect it to remain historically low. A slower month-over- month increase in the consumer price index (CPI) in February confirmed that a spike in prices in January was more a reflection of technical seasonal adjustment issues than a change in trend, but inflation is still running above the Fed’s 2% objective.

Our base case assumption is that an outperforming U.S. economy and above-target inflation will keep the Fed from cutting the fed funds target range this year. But, the balance of risks around that call have been shifting with market expectations for additional cuts already showing up significantly in lower term bond yields.

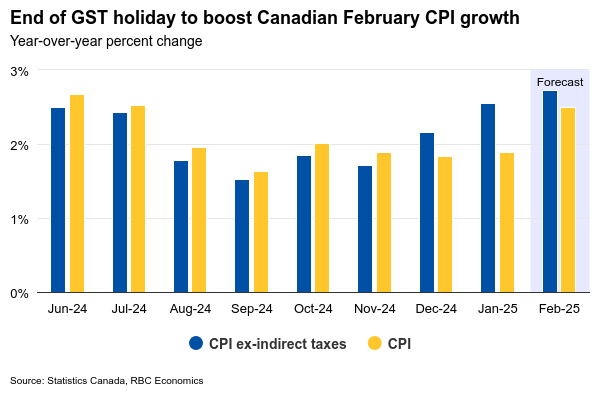

In Canada, the focus will be on February CPI data—in addition to international trade headlines. We expect to see a rise in year-over-year price growth to 2.5% with the GST tax holiday that mechanically depressed prices in December and January, ending in mid-February. That would end a string of six straight readings at or below the Bank of Canada’s 2% inflation target.

Indeed, evidence was building that a faster-than-expected re-acceleration in Canadian growth late last year and into early 2025 was also putting a floor under inflation. The BoC’s preferred “median” and “trim” core measures (which exclude the impact of changes in indirect taxes) picked up 2.7% year-over-year on average in January, and we expect it likely edged higher again in February. But, concerns that intensifying international trade risks will weigh on the economy are overshadowing stronger recent growth data. We continue to expect further BoC interest rate cuts down to 2.25% this summer.

Week ahead data watch

Canadian retail sales are expected to contract by 0.4% in January, following robust growth in the previous month. This decline is primarily attributed to a significant 9% reduction in unit auto sales, partially offset by higher sales at gas stations due to price increases.

Canadian housing starts are forecasted to decrease to 222,000 units in February from 240,000 in January. February’s construction activity was notably hampered by severe winter storms.

U.S. retail sales are expected to rise 0.4% in February, partially recovering from January’s contraction. This growth is largely fueled by stronger auto sales and increased gas station sales.

U.S. industrial production is anticipated to expand by 0.3%, mainly driven by extended manufacturing hours that have boosted output across the sector.