{kind=link}

Despite being pressured in the past few days, Dollar remains relatively resilient, refusing to drop despite renewed selling pressure earlier today. US President Donald Trump’s tariff rhetoric is having a diminishing effect on markets, as traders shift their attention back to fundamental and intermarket dynamics. The first significant market reaction to tariffs is likely to come only after actual implementation, with the initial measures on Canada, Mexico, and China anticipated on February 1.

A key intermarket factor aiding Dollar’s stability is recovery in US Treasury yields, which is providing some support. However, upside momentum of the greenback is clearly capped by strong risk-on sentiment in equity markets. In particular, S&P 500, currently hovering just inch below its all-time high of 6099.97, is showing robust upward momentum. Decisive break above this level would confirm the resumption of the index’s long term up trend, with upper channel resistance (now at around 6380) as next target.

For the week so far, Japanese Yen is the weakest performer as markets look past BoJ’s expected rate hike on Friday. Dollar follows as the second worst performer, trailed Loonie. In contrast, Kiwi is still leading gains, despite expectations of another 50bps RBNZ rate cut after inflation data. Euro is supported by ECB officials’ reassurances of gradual easing, making it the second-best performer. Aussie Australian Dollar comes in third strongest, with Sterling and Swiss Franc positioned in the middle of the pack.

ECB’s Lagarde highlights regular, gradual rate cuts as policy diverges from Fed

ECB President Christine Lagarde emphasized the central bank’s commitment to a “regular, gradual path” of monetary easing, citing progress in disinflation across the Eurozone.

Speaking to CNBC, Lagarde reiterated that the pace of rate cuts will depend on incoming data. Meanwhile, she described the neutral rate — where monetary policy neither stimulates nor restricts the economy — as between 1.75% and 2.25%.

Lagarde also acknowledged the divergence in monetary policy paths between ECB and Fed. She attributed this gap to differing economic circumstances, noting that the two central banks “did not reduce rates at the same pace.” Markets, she said, are pricing in “vastly different monetary policy moves” over the next few months, reflecting these fundamental differences.

On external risks, Lagarde played down concerns about inflation being exported to Europe from the US, suggesting that any reigniting of U.S. inflation would primarily impact the U.S. economy. She added, “We are not overly concerned by the export of inflation to Europe.” However, she acknowledged potential spillover effects through the exchange rate, which “may have consequences.”

SNB’s Schlegel: Negative rates remain a tool, despite being unpopular

SNB Chair Martin Schlegel said today at the World Economic Forum in Davos that with the policy rate currently at 0.50%, “we still have some room” for adjustments. But he ruled out any firm commitment on future rate moves.

While negative rates remain an unpopular tool in Switzerland, Schlegel noted that the SNB would reintroduce them if deemed necessary to stabilize monetary conditions.

Looking ahead to the SNB’s next policy meeting in March, Schlegel indicated that the central bank will evaluate whether further rate adjustments are warranted.

“At the moment monetary conditions are appropriate. We decide from quarter to quarter and then we will see,” he said, refraining from estimating the likelihood of rates turning negative again.

Schlegel also addressed risks stemming from global uncertainties, particularly the tariff hikes proposed by Trump administration. While he downplayed the direct impact of such measures on Swiss inflation, he acknowledged that heightened global risks could bolster the safe-haven appeal of the Swiss Franc.

“Whenever there is a crisis, investors tend to buy the Swiss Franc,” Schlegel said, highlighting the currency’s role in monetary conditions alongside interest rates.

New Zealand CPI unchanged at 2.2% yoy, non-tradeable pressures persist

New Zealand’s CPI rose 0.5% qoq in Q4 2024, in line with expectations, as tradeable inflation increased 0.3% qoq and non-tradeable inflation rose 0.7% qoq. Annually, CPI was unchanged at 2.2% yoy, slightly exceeding the anticipated 2.1% yoy. This marks the second consecutive quarter that inflation has stayed within RBNZ’s target range of 1% to 3%.

The data highlights diverging trends within inflation components. Non-tradeable inflation, which reflects domestic demand and supply conditions and excludes foreign competition, stood at 4.5% yoy, highlighting persistent internal price pressures. Tradeable inflation, influenced by global factors, recorded a -1.1% yoy decline.

Rent prices were the largest contributor to the annual CPI increase, rising 4.2% and accounting for nearly 20% of the overall 2.2% gain. Lower petrol prices, down -9.2% yoy, offset some of the upward momentum, with CPI excluding petrol increasing 2.7% yoy.

Australia’s Westpac Leading Index falls to 0.25%, signals gradual growth pickup

Westpac Leading Index for Australia dipped slightly in December, moving from 0.33% to 0.25%. Westpac noted that while the growth signal remains modest, it reflects a marked improvement from the consistently negative and below-trend readings observed over the past two years. This uptick hints at a gradual lift in economic momentum through the first half of 2025.

Westpac forecasts GDP growth to improve steadily over the course of 2025, projecting a year-end expansion of 2.2%—a notable recovery from the weak 0.8% growth recorded in the year to September 2024. However, the bank noted that while this represents progress, it remains below the economy’s long-term potential.

Westpac highlighted that recent improvements in the Leading Index coincide with mixed signals on broader economy. A key concern for RBA is the labor market, where the “rebalancing” stalled in H2 2024.

“A further slowdown in underlying measures of inflation could still see the Bank ease in February or April but we suspect the RBA will need to be more comfortable about some of these risks before it is prepared to begin easing,” Westpac noted.

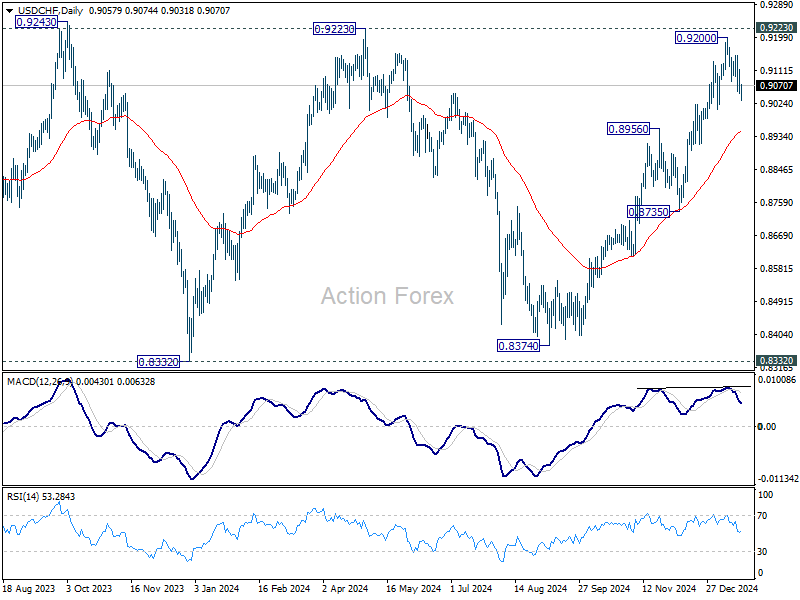

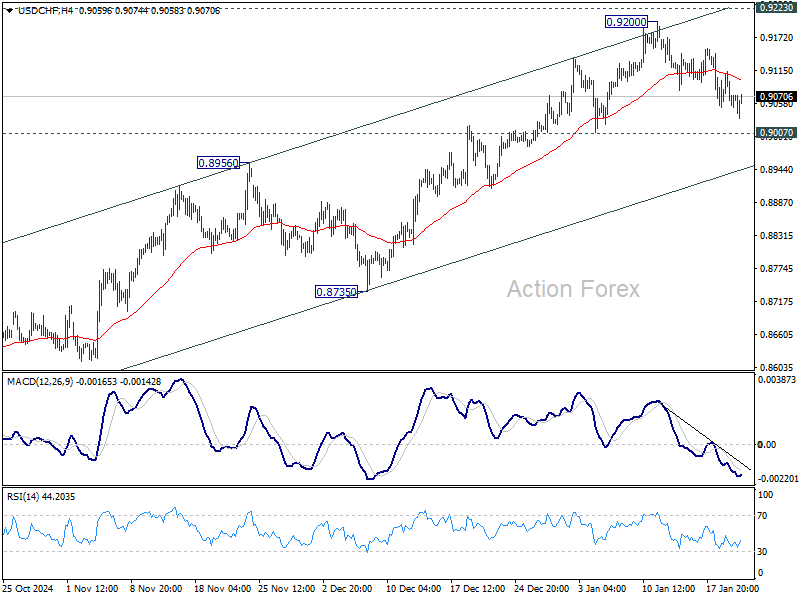

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9032; (P) 0.9077; (R1) 0.9102; More…

Intraday bias in USD/CHF stays neutral for now, as the pair is in mild recovery. Price actions from 0.9200 are seen as a near term corrective pattern only. Further rally is expected with 0.9007 support intact. On the upside, decisive break of 0.9223 will carry larger bullish implications. However, break of 0.9007 will turn bias back to the downside for deeper pull back to 55 D EMA (now at 0.8950).

In the bigger picture, as long as 0.9223 resistance holds, price actions from 0.8332 (2023 low) are seen as a medium term corrective pattern. That is, long term down trend is in favor to resume through 0.8332 at a later stage. However, sustained break of 0.9223 will be an important sign of bullish trend reversal.