{kind=link}

Dollar weakened broadly in early US session as reports from The Wall Street Journal indicated that Donald Trump, during his inauguration, will only outline his trade vision but avoid imposing new tariffs for now. While this temporarily calms market fears of immediate disruptions, the situation remains dynamic, and unexpected developments could trigger sharp reversals, especially if the WSJ report proves inaccurate.

According to the report, Trump plans to issue a memorandum directing federal agencies to study trade policies and assess trade relationships with key partners, including China, Canada, and Mexico. The memorandum is expected to focus on addressing persistent trade deficits and investigating unfair trade and currency practices.

Specific directives include examining China’s compliance with the 2020 trade deal and reviewing the US-Mexico-Canada Agreement, which is up for re-evaluation in 2026. These steps suggest Trump is prioritizing groundwork over immediate action, but the spotlight remains on the possibility of future tariffs.

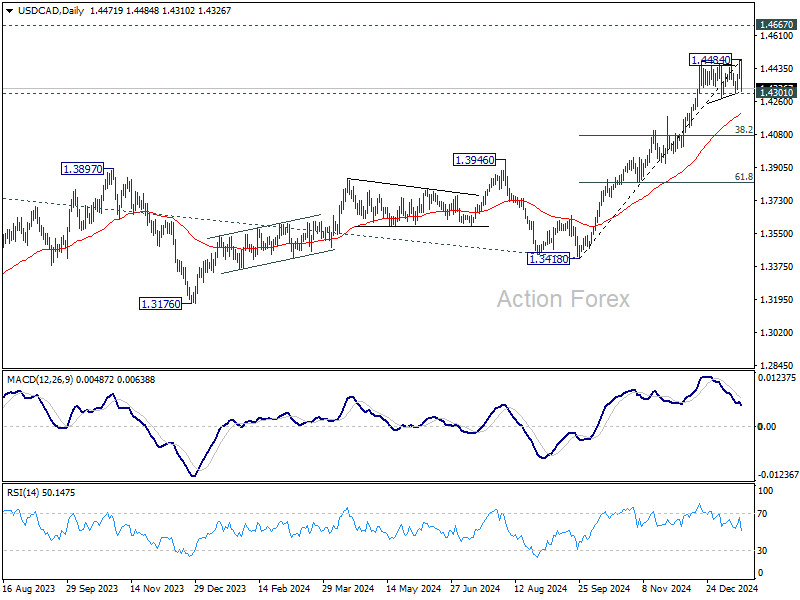

Technically, immediate focus is now on 1.4301 support in USD/CAD’s with today’s sharp reversal. Firm break there would at least bring deeper pull back to 55 D EMA (now at 1.4194). There is prospect of even deeper fall to 38.2% retracement of 1.3418 to 1.4484 at 1.4077 should CPI and retail sales data from Canadian Dollar later in the week are Loonie supportive. Or, at least, Canadian Dollar could have a breather until Trump’s tariffs are really imposed.

In Europe, at the time of writing, FTSE is extending its record run and rises 0.12%. DAX is down -0.03% while CAC is up 0.02%. UK 10-year yield is up 0.041 at 4.701. Germany 10-year yield is up 0.016 at 2.548. Earlier in Asia, Nikkei rose 1.17%. Hong Kong HSI rose 1.75%. China Shanghai SSE rose 0.08%. Singapore Strait TImes fell -0.07%. Japan 10-year JGB yield fell -0.010 to 1.197.

ECB’s Holzmann: January rate cut not as certain with elevated inflation risks

Austrian ECB Governing Council member Robert Holzmann expressed skepticism over a potential rate cut at ECB’s upcoming January meeting. In an interview with Politico, Holzmann stated, “A cut is not a foregone conclusion for me at all,” emphasizing his commitment to approaching the discussion with an “open mind.”

Holzmann highlighted that ECB decisions are fundamentally data-driven and noted that inflation remained “well above” 2% in December, with January figures expected to reflect similar levels. He cautioned that “cutting interest rates when inflation rises faster than anticipated, even temporarily, risks hurting credibility.”

As a known policy hawk, Holzmann also revealed increased doubts about inflation settling around ECB’s 2% target by the end of the year. He cited unexpected developments since the December decision, including faster-than-expected depletion of gas reserves due to colder weather, the effective closure of the Ukraine gas transit, and the risks of persistently high energy prices.

China maintains LPR as offshore Yuan recovers ahead of key support

China’s central bank maintained its benchmark lending rates unchanged on Monday. The one-year loan prime rate was steady at 3.1%, while the over-five-year LPR, which influences mortgage rates, remained at 3.6%.

The offshore Yuan strengthened notably against the Dollar, continuing to draw support from a a key long-term level. This comes despite market speculation that China might allow Yuan to weaken further to counteract the economic effects of new tariffs introduced under Donald Trump’s presidency.

A weaker currency would bolster export competitiveness by making Chinese goods more affordable internationally. However, Beijing faces a dilemma: while a controlled depreciation could help exporters, an uncontrolled fall could lead to heightened volatility in domestic financial markets and reduced investor confidence.

Acknowledging these risks, PBOC Governor Pan Gongsheng reaffirmed the central bank’s commitment to exchange rate stability last week, stating, “We will resolutely prevent the risk of the exchange rate overshooting, ensuring that the Yuan exchange rate remains generally stable at a reasonable, balanced level.”

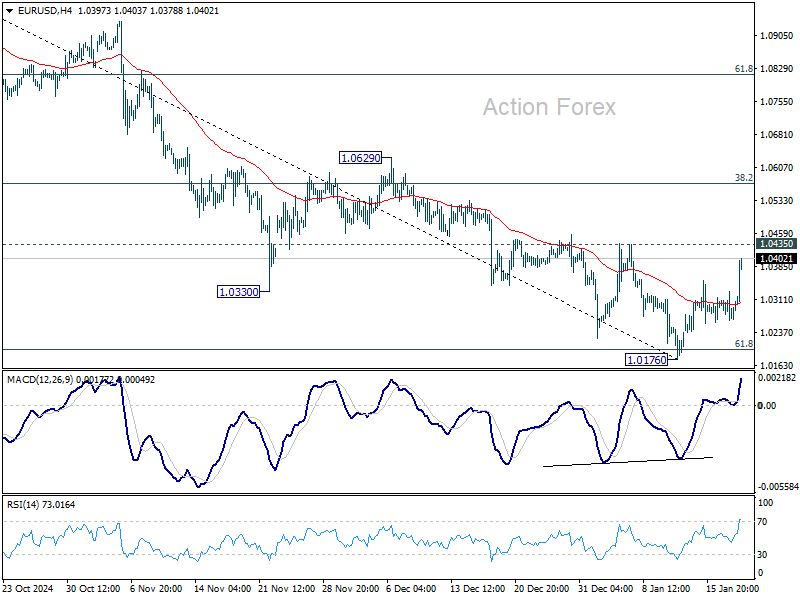

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0247; (P) 1.0289; (R1) 1.0313; More…

EUR/USD is still capped below 1.0435 resistance despite extending rebound from 1.0176. Intraday bias remains neutral and outlook stay bearish. Firm break of 1.0176 will resume whole fall from 1.1213. However, decisive break of 1.0435 will confirm short term bottoming, and turn bias back to the upside for stronger rebound to 38.2% retracement of 1.1213 to 1.0176 at 1.0572 first.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.