{kind=link}

Sharp selloff in commodity currencies against Dollar is dominating market action as the US session unfolds. While broader trading remains subdued, the sudden weakness in these currencies appears tied to trader caution ahead of President-elect Donald Trump’s inauguration on Monday. Concerns over tariff policies could be the main driver of the moves, in the absence of other clear fundamental catalysts.

Canada, Mexico, and China are widely speculated to be high on Trump’s tariff agenda. The tariffs may serve as leverage to address issues like fentanyl exports or re-exports impacting the United States.

However, the specifics of Trump’s strategy remain a “wild card.” Possible scenarios include blanket tariffs on major trading partners, sector-specific measures, immediate enactment via executive orders, or staggered monthly increases. Or, it could be a mix of these approaches.

For the week, Sterling remains the weakest performer, followed by Loonie and Dollar. On the other hand, Japanese Yen leads gains with the Aussie and Swiss Franc rounding out the top three. Kiwi and Euro are trading in mixed positions. However, the current selling pressure on commodity currencies could alter these rankings as the week comes to the close.

ECB’s Nagel: Should avoid rushing monetary policy normalization

German ECB Governing Council member Joachim Nagel in an interview with Platow Brief, highlighted persistent services inflation and a “high level of uncertainty,” referencing concerns about global trade dynamics as Donald Trump prepares to return to the White House next week.

“We should therefore not rush into anything on the path to monetary policy normalization,” Nagel stated.

Meanwhile, he defended the ECB’s discussions of a more aggressive 50-basis-point rate cut during its December meeting, noting that such debates are a normal part of policy deliberations.

ECB’s Elderson: Rate setting is a question of speed and magnitude

ECB Executive Board member Frank Elderson emphasized the delicate balance the central bank must strike in setting interest rates during an interview with Het Financieele Dagblad.

He warned, “If we lower the interest rate too quickly, dialling down services inflation sufficiently could become complicated.” At the same time, he acknowledged the risks of maintaining rates too high for too long, which could lead to undershooting ECB’s inflation target.

“The markets don’t think we’ve finished easing now that we’re at 3% and I don’t think we have, either,” he added. “Setting interest rates is ultimately a question of how fast and how much.”

Eurozone CPI finalized at 2.4% in Dec, core CPI at 2.7%

Eurozone inflation was finalized at to 2.4% yoy in December, up from November’s 2.2% yoy. Core CPI, which excludes energy, food, alcohol, and tobacco, held steady at 2.7% yoy. Services made the largest contribution to the annual headline inflation rate (+1.78 percentage points), followed by food, alcohol, and tobacco (+0.51 pp), non-energy industrial goods (+0.13 pp), and energy (+0.01 pp).

In the broader EU, inflation was finalized at 2.7% yoy, up from 2.5% yoy in November. Ireland recorded the lowest annual inflation rate at 1.0%, followed by Italy at 1.4%, with Luxembourg, Finland, and Sweden at 1.6% each. On the other end, Romania (5.5%), Hungary (4.8%), and Croatia (4.5%) posted the highest inflation rates.

Across the EU, annual inflation rose in 19 member states, remained unchanged in one, and fell in seven compared to the previous month.

UK retail sales fall -0.3% mom in Dec, down -0.8% qoq in Q4

UK retail sales volumes declined by -0.3% mom in December, significantly missing expectations for 0.4% mom increase. The drop was primarily driven by reduced supermarket sales, partially offset by a rebound in non-food stores such as clothing retailers, which saw recovery after recent declines.

On a quarterly basis, sales volumes in Q4 fell -0.8% qoq compared with Q3, highlighting a slowdown in consumer activity. However, year-on-year, Q4 sales volumes rose 1.9% compared to the same period in 2023.

China’s Q4 GDP growth surpasses expectations, full-year growth hits 5% target

China’s economy ended 2024 on a strong note, with GDP expanding by 5.4% yoy in Q4, beating market expectations of 5.0%. This marked a significant acceleration from 4.6% in Q3, 4.7% in Q2, and 5.3% in Q1. The robust Q4 performance pushed full-year GDP growth to 5.0%, aligning with the government’s target of “around 5%.”

December’s economic indicators also showed positive momentum. Industrial production surged 6.2% yoy, exceeding the forecast of 5.4%. Retail sales grew by 3.7% yoy, marginally beating expectations of 3.5%. However, fixed asset investment lagged, rising only 3.2% year-to-date, just below the 3.3% forecast.

Despite the upbeat data, concerns remain. Statistics Bureau spokesperson Fu Linghui acknowledged lingering weakness in consumer spending and cautioned that in 2025, the “unfavorable impact of external factors may deepen.”

BNZ PMI at 45.9: NZ manufacturing completes 2024 fully in contraction

New Zealand’s BNZ Performance of Manufacturing Index rose marginally in December, increasing from 45.2 to 45.9. While this marks a slight improvement, the sector remains in a prolonged contraction, far below the long-term average of 52.5 since the survey’s inception. December also marked the 22nd consecutive month of contraction, a record-breaking trend for the PMI.

Catherine Beard, Director of Advocacy at BusinessNZ, noted that 2024 was unprecedented, as it was the first year in the survey’s history with all 12 months in contraction. By comparison, the next closest period was 2008 during the Global Financial Crisis, which saw nine months of contraction.

Breaking down the December data, production dropped further, slipping from 42.3 to 41.9. Employment showed modest improvement, rising from 46.9 to 47.6, while new orders also edged up from 44.5 to 46.5. However, finished stocks fell significantly, declining from 49.2 to 45.9, and deliveries dipped slightly below the neutral 50 mark, moving from 50.0 to 49.8.

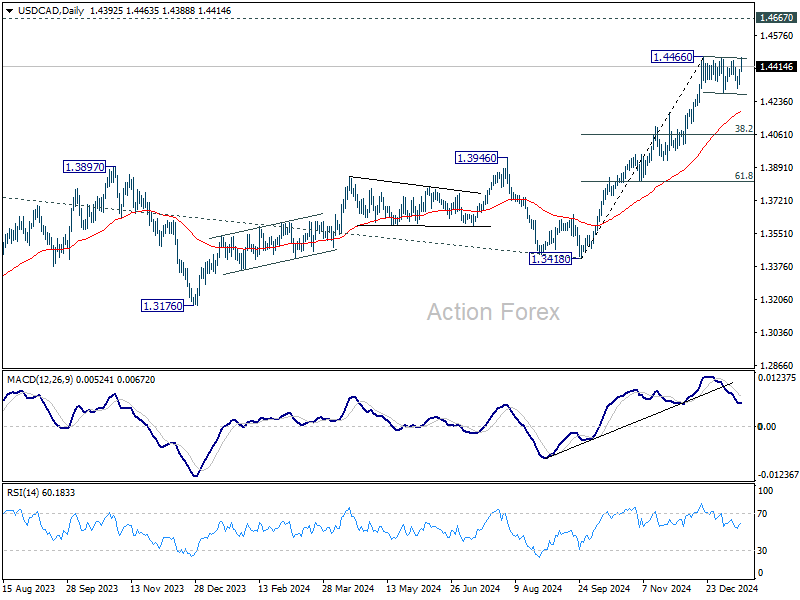

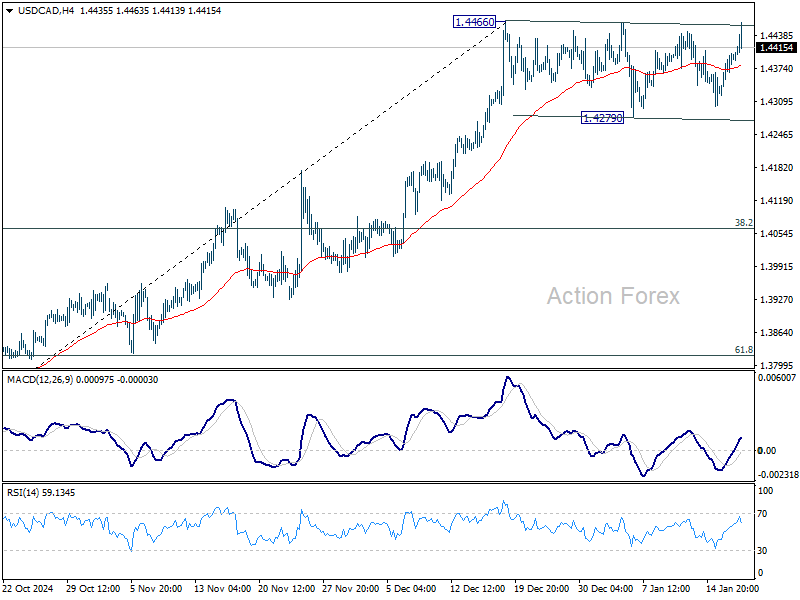

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.4336; (P) 1.4370; (R1) 1.4427; More…

Immediate focus is now on 1.4466 resistance with current strong rally ins USD/CAD. Decisive break there will resume larger up trend to 1.4667/89 long term resistance zone. On the downside, break of 1.4279 support will bring deeper correction. But downside should be contained by 55 D EMA (now at 1.4187) to bring rebound.

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.