{kind=link}

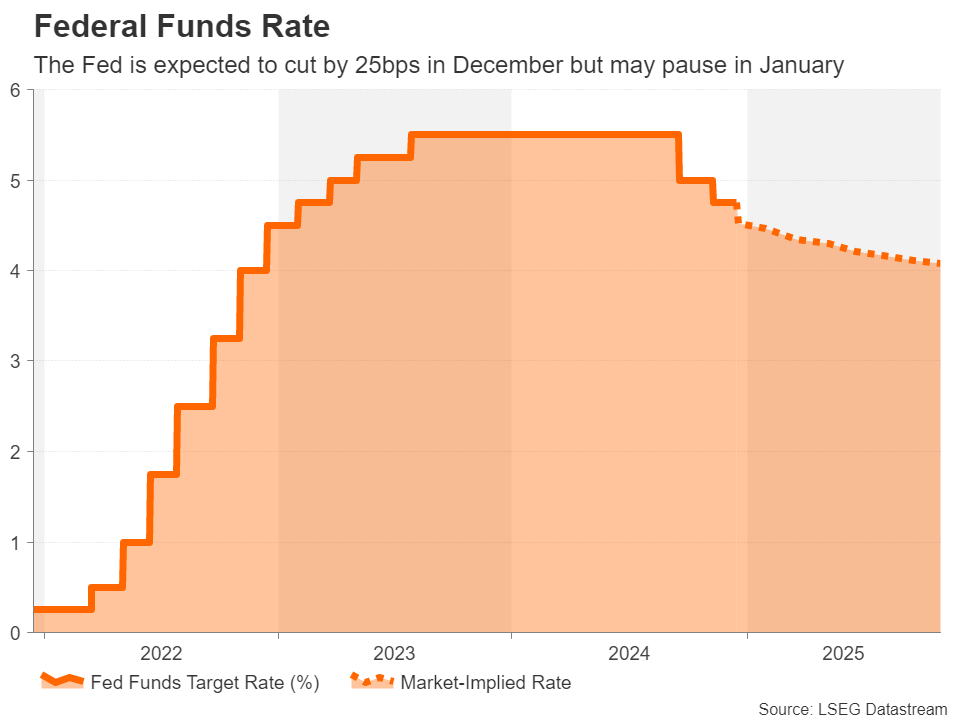

- Fed is widely expected to cut rates by 25 bps on Wednesday

- But updated dot plot may signal fewer cuts in 2025

- Can the dollar extend its rebound or is a correction due?

- Powell’s press conference at 19:30 GMT could hold the key

Rate cut bets have been pared back

The US Federal Reserve meets this week for the last time in 2024 and it looks set to end the year with its third rate cut since September. However, it’s only in the past week or two that investors have become confident that the central bank will deliver a 25-basis-point reduction in the Fed funds rate when it announces its decision at 19:00 GMT on Wednesday.

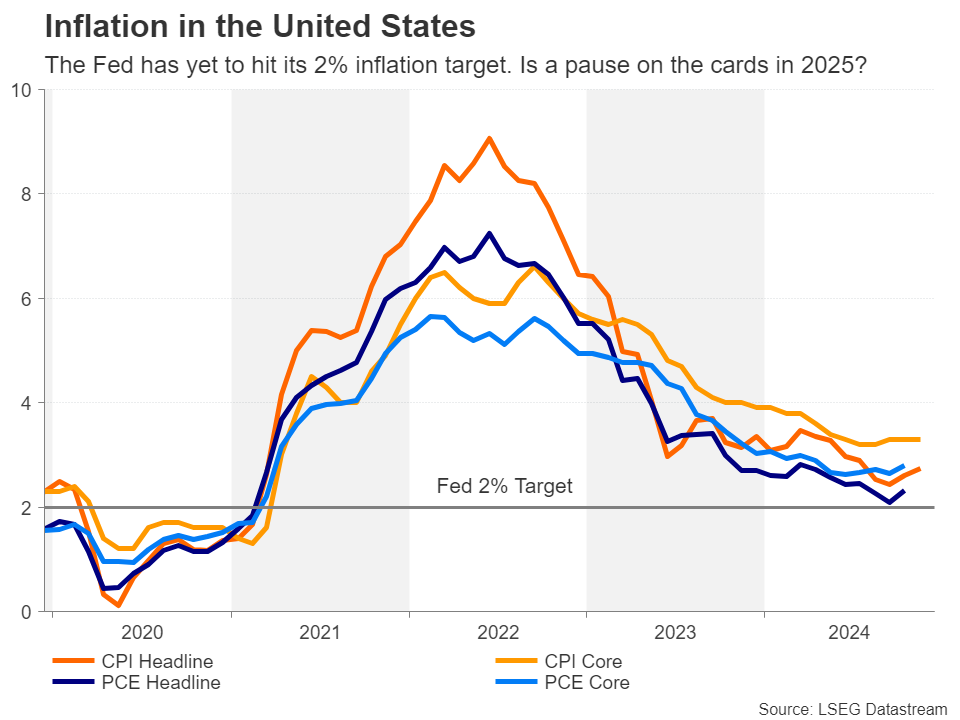

A string of upbeat economic indicators as well as inflation edging higher over the last couple of months, not to mention of course Trump’s election victory, have all led to a drastic repricing of the expected number of rate cuts next year. Donald Trump’s re-election and the implications his policies could have on growth and inflation have complicated the Fed’s interest rate path at a time when the US economy continues to defy fears of a slowdown and underlying price pressures remain sticky.

All eyes on new dot plot

If the Fed does trim rates as expected in December, markets currently foresee just two more 25-bps cuts in 2025. That would be about 50 bps less than what FOMC members predicted in the September dot plot. So, what’s the likelihood that the December dot plot will be revised accordingly?

Most Fed officials backed the case for further rate cuts heading into the blackout period but were split on the size of easing that would be warranted with the inflation picture as it is now. With markets having already done the heavy lifting, policymakers will probably pencil in a similar path as implied by traders.

Will the Fed signal several rate cuts or a pause?

In fact, the risk for the dot plot is tilted toward a dovish surprise as some FOMC members may still be optimistic about inflation coming down substantially in 2025 and therefore being able to cut rates by at least three times. Although, if it’s evident that policymakers based their projections on not making too many assumptions about how inflationary Trump’s policies will be, investors might not be very convinced about a more dovish path.

Hence, Jay Powell’s press conference will be as closely watched as ever for gauging the Fed chief’s and his colleagues’ views on inflation and the economy. Earlier in December, Powell said that the Fed can “afford to be a little more cautious”. He is likely to reiterate that there is no rush to take rates closer to the neutral level.

The question is how strongly he will signal a pause in January and is he going to open the door to a longer pause? The odds that the Fed will stand pat in January currently stand at around 87%.

Dollar could climb to a new 2024 high

Should Powell remain worried about the prospect of inflation staying above the Fed’s 2% goal and the dot plot is predicting barely two rate cuts in 2025, the US dollar could stretch its recent bounce back. The greenback’s index against a basket of currencies could easily surpass the November 22 high of 108.07 if both Powell and the dot plot are more hawkish than anticipated.

Moreover, if any hawkish rhetoric is followed up with an uptick in the core PCE price index on Friday when the November readings are due, the dollar’s bullish streak could extend even still.

Such a move, though, would have to be backed by a similar rally in Treasury yields and this poses a downside risk for Wall Street.

If, however, Powell adopts a more balanced tone and is hopeful that there will be further progress in reducing inflation in 2025, the dollar index could pull back towards its 50-day moving average near 105.30 before attempting to breach the 105.00 level.

Clouded Outlook

On the whole, the Fed meeting may not change much about the monetary policy outlook, and this may stay the case until some of the cloud for 2025 has been lifted. Specifically, the Fed is unlikely to let its guard down on inflation until it sees that the incoming Trump administration’s policies on taxes and tariffs won’t pose a huge risk to re-igniting inflationary pressures. This means that the dollar’s downside is limited for now.

This could change, however, if the labour market starts to deteriorate unexpectedly over the coming months, in which case, the Fed won’t hesitate to lower borrowing costs even if inflation remains problematic.