{kind=link}

Sterling slumped broadly today after UK GDP unexpectedly contracted in October, missing forecasts of modest growth. This contraction underscores the challenges facing the UK economy, which has been grappling with persistent inflation and uncertainty following the Autumn Budget. The government’s recent pledge to transform the UK into the fastest-growing G7 economy now seems even more “ambitious”. While BoE is expected to keep interest rates unchanged at next week’s meeting, deteriorating economic conditions could challenge expectations of four rate cuts in 2025, particularly if the growth outlook weakens further.

Meanwhile, Dollar surged overnight, supported partly by the dovish 25bps rate cut by ECB and stronger-than-anticipated US PPI data. 10-year Treasury yield climbed above the 4.3% mark, reflecting worries over ongoing inflationary pressures. Coupled with recent CPI data showing a plateau in disinflation, Fed remains on track for a pause in its rate-cutting cycle after this month’s expected 25bps reduction. The path of rate easing next year looks more set to be gradual, with terminal rates potentially higher than previously anticipated, reinforcing support for the greenback.

So far this week, Dollar has emerged as the strongest performer, followed by Australian Dollar, which drew strength from surprisingly robust employment data. Canadian Dollar ranks third. At the other end of the spectrum, Japanese Yen is the weakest, with limited reaction to the Tankan Survey data released today. Swiss Franc and New Zealand Dollar also underperformed, while Euro and Sterling occupy a neutral middle ground.

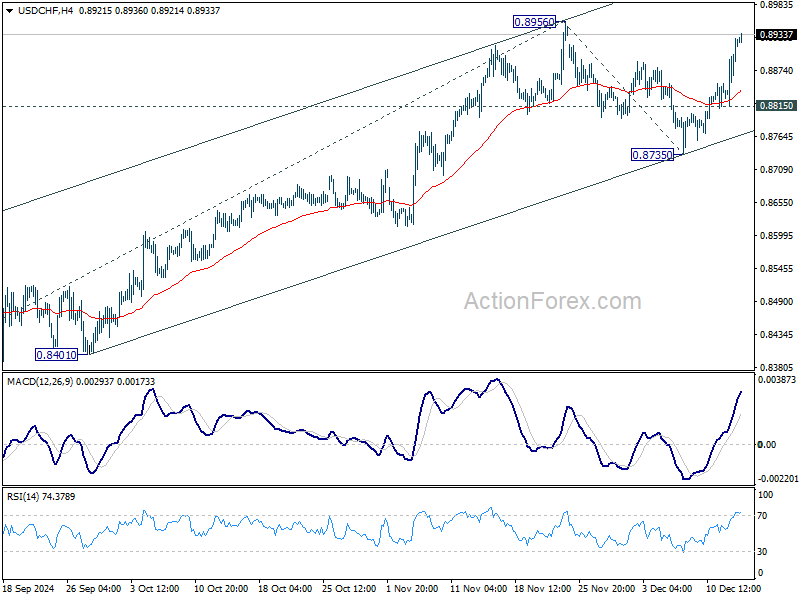

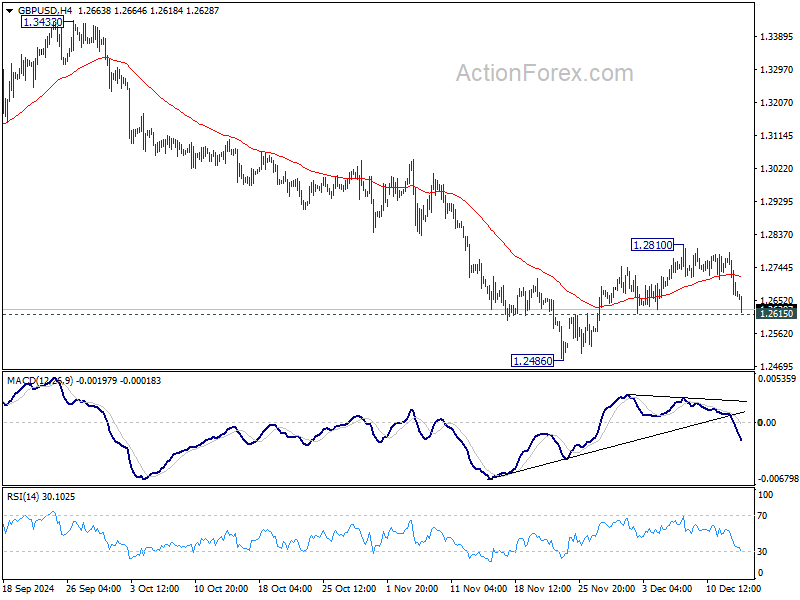

Technically, Dollar is gaining bullish momentum again with break of 1.0471 minor support in EUR/USD. Retest of 1.0330 should be seen next. To solidify Dollar’s momentum, some more progress will be needed including breaking of 1.2615 minor support in GBP/USD, 0.6336 support in AUD/USD, and 0.8956 resistance in USD/CHF.

In Asia, Nikkei fell -0.95%. Hong Kong HSI is down -1.82%. China Shanghai SSE is down -2.01%. Singapore strait times is up 0.16%. Japan 10-year JGB yield fell -0.0083 to 1.043. Overnight, DOW fell -0.53%. S&P 500 fell -0.54%. NASDAQ fell -0.66%. 10-year yield rose 0.053 to 4.324.

UK economy contracts -0.1% mom in Oct, dragged down by weak production

UK GDP fell by -0.1% mom in October, disappointing expectations for 0.1% mom growth. The decline was primarily driven by a -0.6% mom contraction in production output, with no growth observed in services and a -0.4% mom decline in construction output.

On a rolling three-month basis, GDP showed a marginal increase of 0.1% in the period ending October, compared to the prior three-month period. This modest growth was supported by a 0.1% expansion in services and a 0.4% rise in construction output. However, production output contracted by -0.3%, weighing on overall performance.

Japan’s Tankan Survey: Manufacturing Confidence Improves to 14

Confidence among Japan’s major manufacturers showed a modest recovery in Q4, breaking a two-quarter decline. The Tankan large manufacturing index rose to 14 from 13, slightly exceeding market expectations. However, the outlook dipped marginally from 14 to 13, though still better than the anticipated 11.

In contrast, the non-manufacturing sector, which includes services, saw its index decline to 33 from 34, marking the first deterioration in two quarters. The outlook for non-manufacturers held steady at 28.

On a bright note, large Japanese companies across sectors plan to boost capital expenditure by 11.3% in the fiscal year ending March 2025. This is a notable increase from the 10.6% projection in the September survey and surpasses market forecasts of 9.6%.

NZ BNZ PMI falls to 45.5, 21st month of contraction

New Zealand’s BNZ Performance of Manufacturing Index dipped from 45.7 to 45.5 in November, marking its lowest reading since July 2024 and extending the contraction streak to 21 consecutive months. Despite some improvement in select components, the sector remains under significant strain, highlighting the challenges of achieving a meaningful turnaround.

Production weakened further, dropping from 44.0 to 42.5, signaling continued struggles in output. New orders also plunged from 48.5 to 44.8, underlining the persistent lack of demand. In contrast, employment improved modestly from 46.0 to 46.9, and finished stocks edged higher from 47.8 to 49.3. Deliveries saw the most notable recovery, rising from 44.9 to 49.9, yet still narrowly missed returning to expansion territory.

The sentiment among respondents remains predominantly negative, with 56% of comments in November reflecting pessimism, slightly up from 53.5% in October. Recurring concerns revolve around weak order volumes and the enduring pressures of high living costs. However, this negativity has moderated from its peak of 71.1% in mid-2024, suggesting some stabilization.

Doug Steel, Senior Economist at BNZ, noted that while manufacturers are beginning to show improved confidence about the future, “the main message of a manufacturing sector still under significant pressure remains. There is scant evidence of a general turnaround in activity to date.”

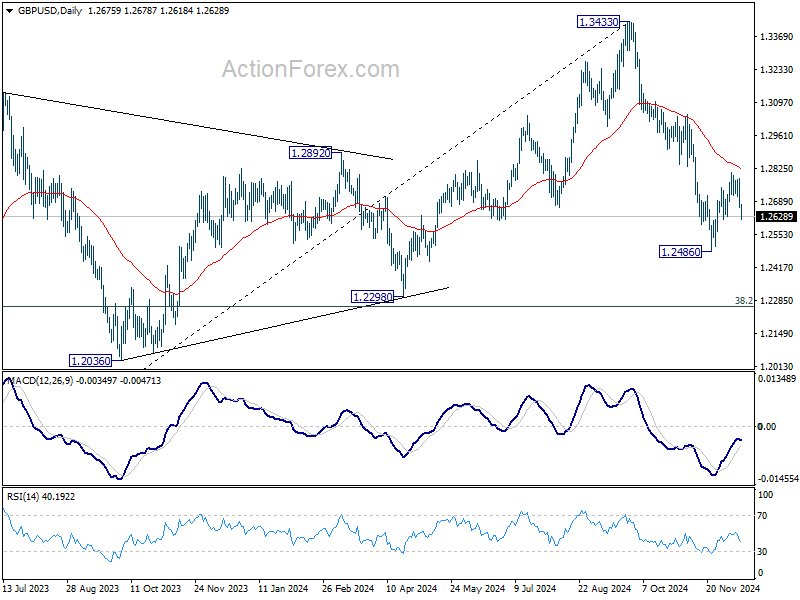

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2631; (P) 1.2710; (R1) 1.2752; More…

Sterling’s extended decline today suggests that corrective rebound from 1.2486 has completed at 1.2810 already. Immediate focus is now on 1.2615 minor support. Firm break there will bring retest of 1.2486 first. Break there will resume whole decline from 1.3433 to 1.2298 cluster support zone.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.