{kind=link}

Dollar showed minimal reaction, other than some initial jitters, to November’s US CPI data, holding steady within its range as the report largely aligned with expectations. Headline inflation edged up, while core inflation remained flat, refusing to trend lower. With no surprise, the data cleared the way for a 25bps rate cut by Fed next week, with Fed fund futures pricing a near-certainty at 99.9%. However, the real focus has shifted to January, where the likelihood of a pause remains high at over 75%. Fed’s outlook, therefore, appears relatively unchanged, with policymakers likely to reassess conditions early next year amid ongoing uncertainties surrounding fiscal and trade policies under the incoming US administration.

In contrast, Japanese Yen is facing broad declines despite stronger-than-expected wholesale inflation data. November’s Corporate Goods Price Index rose by 3.7% yoy, accelerating from October’s 3.6% and marking the fastest pace since mid-2023. This suggests renewed inflationary pressures in corporate prices, creating a dilemma for BoJ, which continues to face subdued consumption despite robust wage growth. after all, Markets anticipate another rate hike imminently, whether at this week’s meeting or in January. Ultimately, the timing of the move may not significantly alter Yen’s trend.

Overall for the day so far, Swiss Franc is currently the strongest one. Canadian Dollar is the second, awaiting BoC’s rate cut while Dollar is third. Yen is the worst for now. Aussie and Kiwi follow next on speculations that China would allow Yuan to weaken next year to cushion some of the impacts of renewed tariff war with the US. Euro and Sterling are positioning in the middle.

Australian Dollar will be the focus again in the upcoming Asian session, with Australian job data featured. Aussie continues to struggle, weighed down by a confluence of negative factors. The RBA’s surprise dovish policy shift has added to speculation of a possible February rate cut, though May remains the base case for many analysts. Furthermore, China’s stimulus pledges have failed to inspire sustained confidence, and markets are now grappling with concerns that Beijing may allow the Yuan to weaken further in 2025 to counter US tariffs. Traders are now awaiting Australia’s job data, which could tilt the balance further toward an earlier easing by RBA if it signals significant labor market loosening.

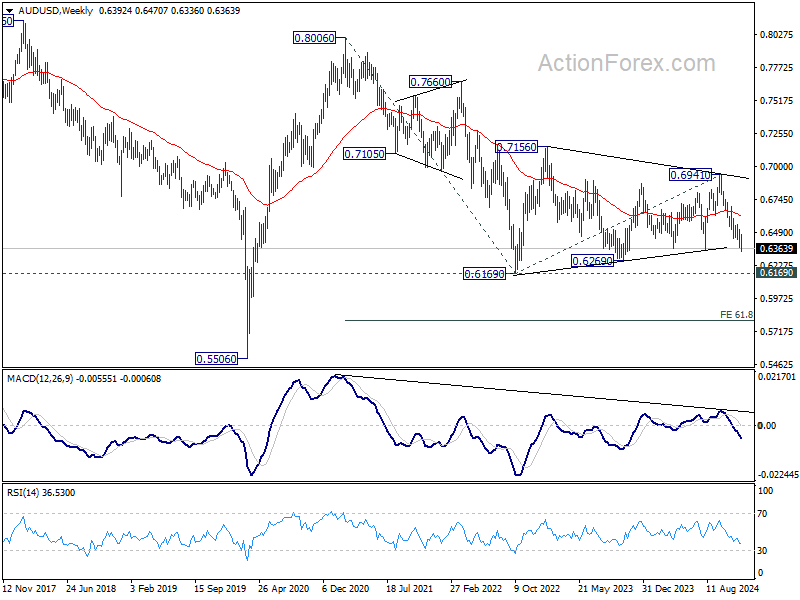

Technically, AUD/USD will soon enter into an important medium term support zone of 0.6169/6269 on next fall. Strong support could be seen there, at least on first attempt, to bring rebound. While AUD/USD would stay bearish even with a rebound, it would be hard for it to break through 0.6169, not until RBA’s easing has commenced and we’d know the pace.

In Europe, at the time of writing, FTSE is up 0.31%. DAX is up 0.03%. CAC is up 0.37%. UK 10-year yield is down -0.0156 at 4.314. Germany 10-year yield is down -0.021 at 2.102. Earlier in Asia, Nikkei rose 0.01%. Hong Kong HSI fell -0.77%. China Shanghai SSE rose 0.29%. Singapore Strait Times fell -0.54%. Japan 10-year JGB yield rose 0.006 to 1.072.

US CPI accelerates to 2.7% in Nov, core CPI unchanged at 3.3%

November’s US inflation data came in line with expectations, showing no significant progress toward easing price pressures further. Headline CPI rose 0.3% mom, supported by a 0.3% mom rise in the shelter index, which accounted for nearly 40% of the monthly increase. Food prices rose by 0.4% mom, while the energy index rose 0.2% mom. Core CPI, excluding volatile food and energy prices, also rose by 0.3% mom.

On an annual basis, headline CPI ticked up from 2.6% yoy in October to 2.7% yoy in November, aligning with market forecasts. Core CPI, excluding the volatile food and energy components, remained steady at 3.3% yoy. Among key categories, food prices increased 2.4% yoy, while energy prices remained a deflationary force, falling -3.2% yoy.

RBA’s Hause: Australia more seriously affected by global trade war because of China reliance

RBA Deputy Governor Andrew Hauser addressed the implications of US President-elect Donald Trump’s proposed tariffs at an event today. He highlighted that while higher global tariffs could depress activity across supply chains, the full extent of the effects would depend on various factors, including currency adjustments and fiscal responses in affected economies.

“Given this uncertainty, it is important that we don’t prejudge the implications of tariffs for policy but monitor developments closely and stand ready to respond appropriately as the facts emerge,” Hauser stated.

Hauser pointed out Australia’s unique vulnerability due to its trade exposure, with over 80% of its iron ore exports destined for China, which accounts for three-quarters of global iron ore imports.

This heavy reliance on China increases the risk of significant disruptions if Beijing becomes the target of punitive tariffs or if global trade realigns along geopolitical lines.

“This seems to suggest that Australia could find itself more seriously affected by a global trade war than some of the average exposure data suggest,” Hauser noted.

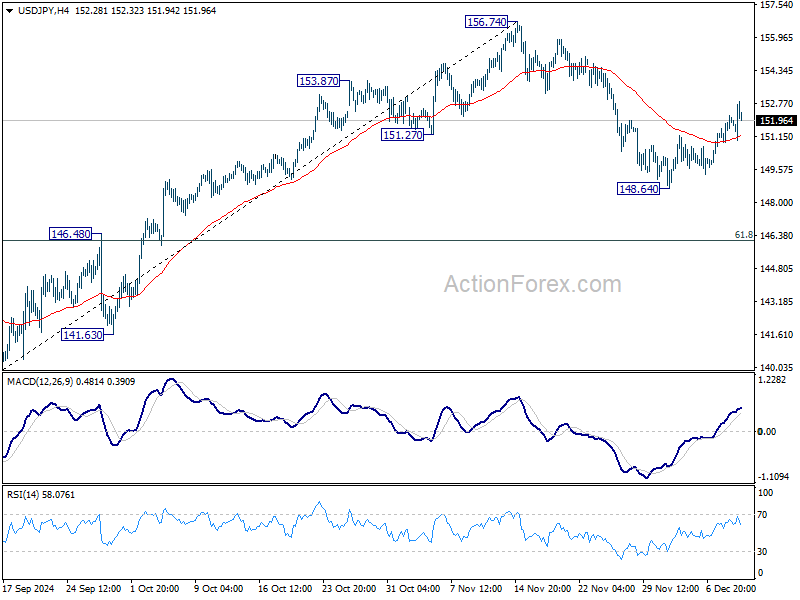

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.18; (P) 151.69; (R1) 152.47; More…

Intraday bias in USD/JPY remains mildly on the upside for the moment. Corrective pullback from 156.74 could have completed at 148.64, and larger rise from 139.57 might be still in progress. Further rally would be seen to retest 156.74 first. Firm break there will target 161.94 high next. For now, this will be the favored case as long as 148.64 support holds.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.