{kind=link}

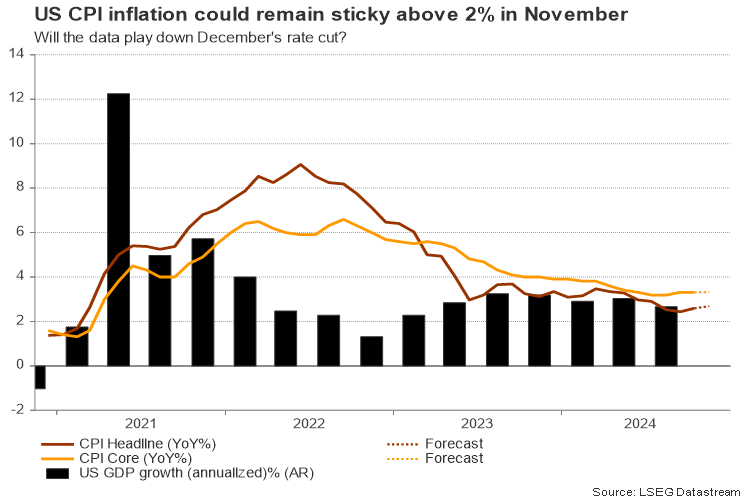

- US CPI inflation could inch higher for the second month

- A December rate cut could stay a close call

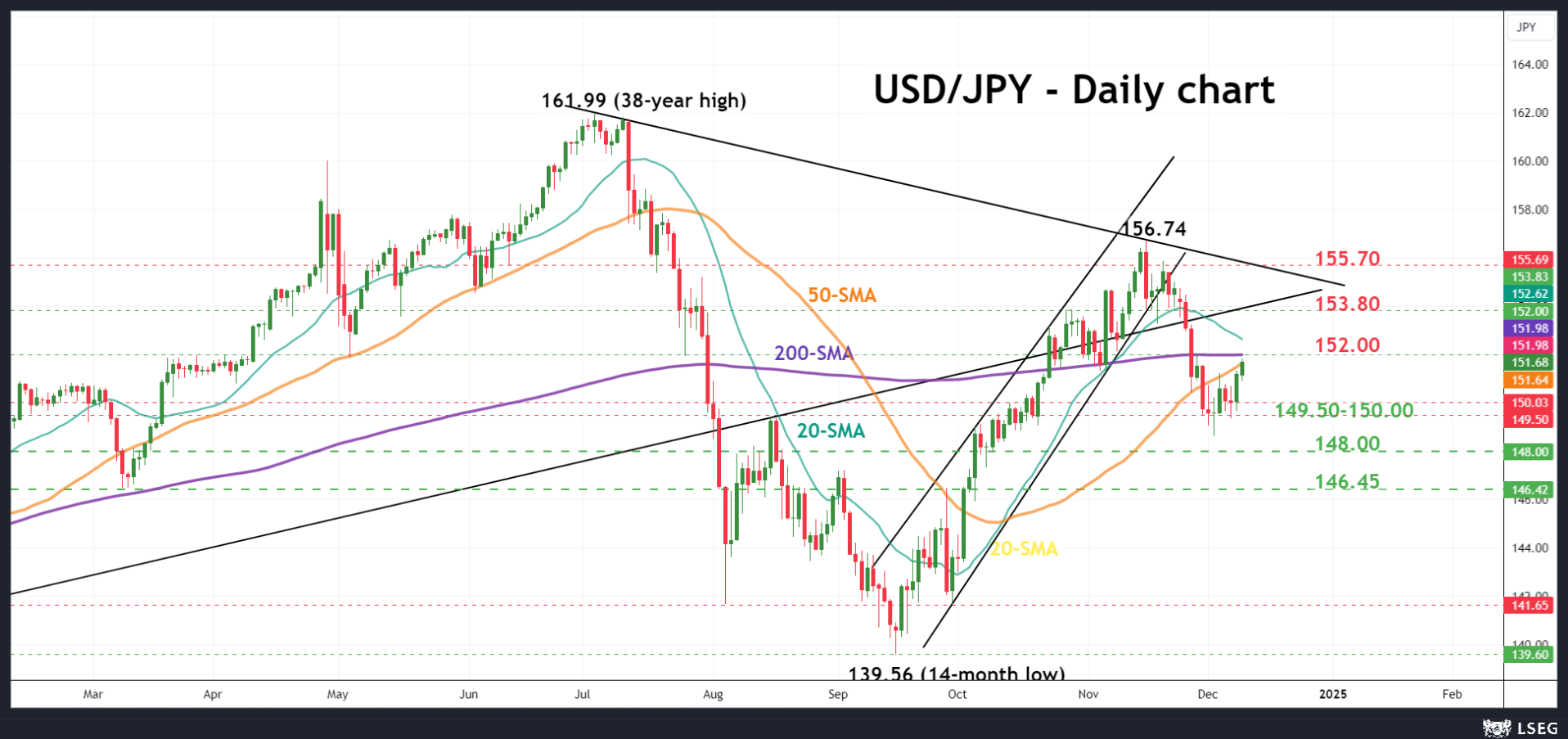

- USDJPY pushes for some recovery, needs a break above 152.00

US nonfarm payrolls could not play down the odds of a 25bps December rate cut despite clocking in stronger than expected last week. But could a rise in the US CPI inflation data derail those expectations?

Forecasts

The figures will be out on Wednesday at 13:30 GMT and analysts are forecasting a slight uptick in monthly CPI inflation, from 0.2% to 0.3%, which would push the annual rate up to 2.7% from 2.6% previously. The core CPI, which strips out volatile food and energy prices, is expected to remain steady at 0.3% month-over-month and 3.3% year-over-year.

Could CPI inflation derail a rate cut?

If inflation proves more persistent than anticipated, holding above the Fed’s 2.0% target, particularly in housing and shelter—a category that contributed over half of October’s gains—it could dampen hopes for an immediate rate cut. Recall that Donald Trump reassured investors that he has no intention of firing Fed Chair Jay Powell, signaling a continuity of the existing monetary guidance. Therefore, the Fed may feel less stressed to rush into rate cuts.

Even with these inflation concerns, there is still a compelling case for a rate cut in December. Investors are uncertain about the timing and scale of Trump’s proposed tax cuts and import tariffs, which could stir inflationary pressures, keeping interest rates in restrictive territory longer than expected. This would continue to weigh on growth, forcing the Fed to frontload rate cuts before political uncertainty kicks in.

How would markets react?

With futures markets providing a strong probability of 85% for a December 25bps rate cut in December, a soft negative surprise in the data could moderately press the US dollar. In this case, USDJPY could slide back to the 149.50-150.00 support area, while the 148.00 territory will be watched in the event of a significant slowdown in inflation, which could open the door to a January reduction. Note that the blackout period is already underway. Hence, there won’t be any directional comments from FOMC members in the aftermath.

In the opposite case, where the figures speed up faster than analysts think, the greenback could surpass the 152.00-yen barrier with scope to reach the crucial 153.80 resistance. Yet, given the uncertain 2025 political and economic policy outlook, policymakers could deliver a hawkish rate cut, signaling a potential pause in January.