{kind=link}

The pivotal US non-farm payroll report today stands at the center of market focus, with its implications likely to influence both the Fed decision outlook, but probably more on January meeting than this month’s.

Fed fund futures indicate a 70% probability of a 25bps rate cut this month, up from 66% a week ago. This reflects a growing expectation that recent economic data, including ISM services and manufacturing figures, ADP employment, and JOLTs openings, support further easing to 4.25%-4.50% at the December 18 meeting. This mounting confidence in Fed’s decision is unlikely to be deterred by today’s data, barring any drastic upside surprises.

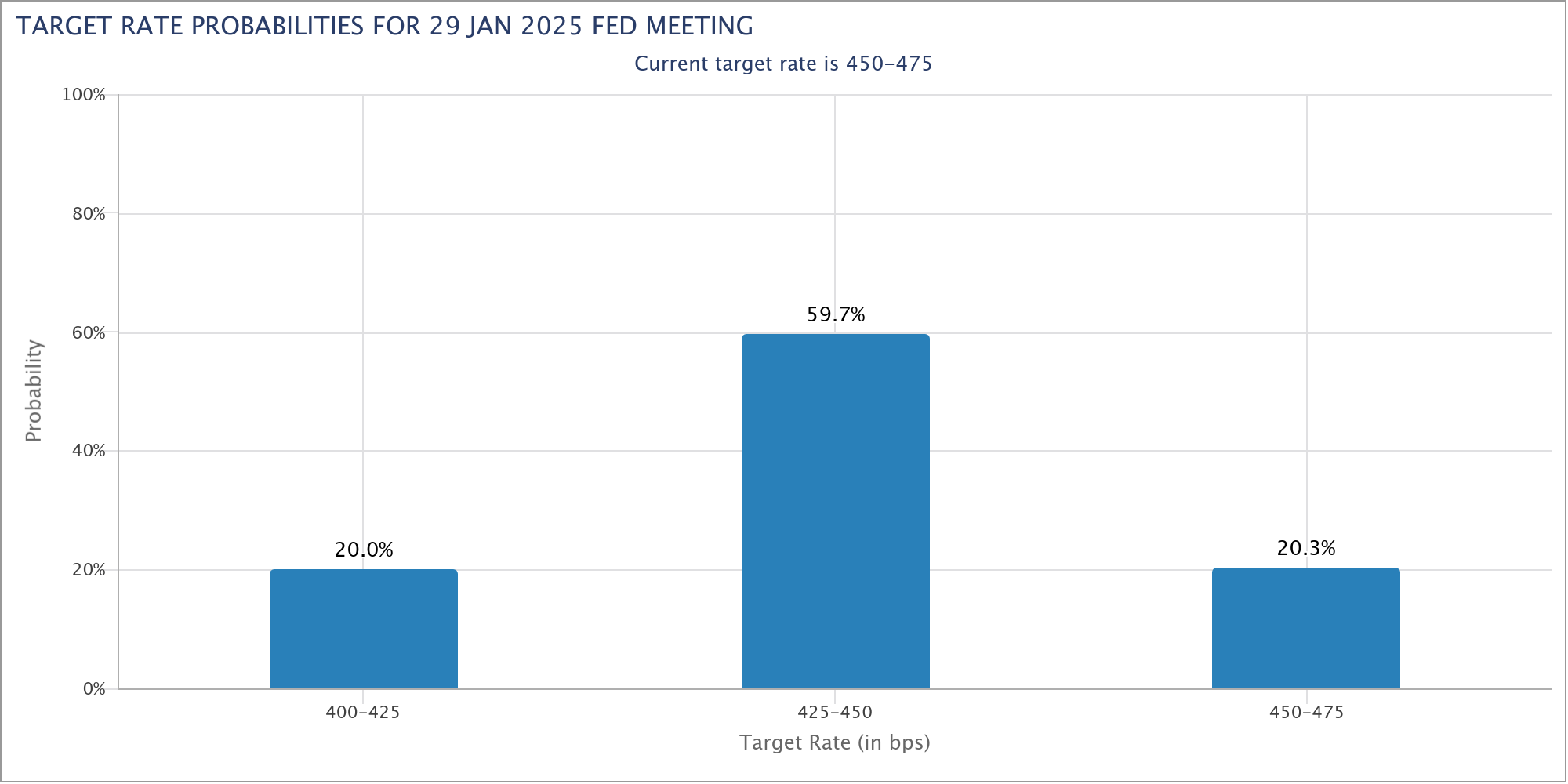

However, sentiment regarding January paints a different picture, with just a 20% likelihood of another 25bps cut to 4.00%-4.25%. A stronger-than-expected NFP report today, particularly one highlighting a significant rebound in job growth after October’s hurricane- and strike-induced distortions, could solidify expectations of a pause in January.

Recent labor market indicators offer a mixed but steady backdrop. ISM Manufacturing Employment improved to 48.1 from 44.4, while ISM Services Employment softened to 52.1 from 56.0. ADP employment showed a moderation in net job additions at 146K, down from a revised 184K prior. Meanwhile, the 4-week average of initial unemployment claims fell to a strong 218K from 236K. These data points suggest no major red flags for today’s NFP release.

In terms of market reactions, Dollar Index remains in a corrective phase after peaking at 108.07. While a recovery today is possible, near-term risks tilt to the downside as long as 106.72 resistance holds. Deeper pullback could extend to 38.2% retracement of 100.15 to 108.07 at 105.04 completion. Nevertheless, rise from 100.15 would remain in favor to resume at a later stage as long as 55 D EMA (now at 104.77) holds.