{kind=link}

- Trump’s agenda and Fed to set the tone for 2025

- Eurozone politics, a dovish ECB and weak growth in the spotlight

- The UK is in better shape, but the budget could prove a major headwind

- Pound strength may persist in early 2025, the euro might find its moment later on

If the stars align, 2025 could be a dream year for the euro

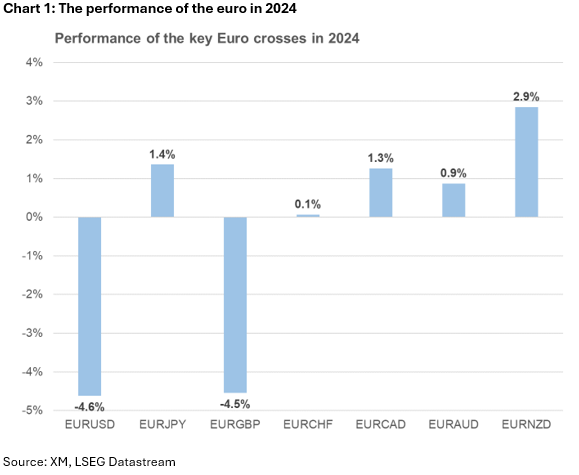

It has been a year to forget for the euro area. Political crises in both France and Germany, continued weak growth – with Germany expected to contract for a second consecutive year – and an active conflict near its eastern borders have all impacted economic momentum. As a result, the euro weakened considerably against both the dollar and the pound.

Going into 2025, the outlook remains clouded. While the world adjusts to Trump’s second term and the Fed’s monetary policy stance, the euro area is leaderless. The new German Chancellor is expected to take office by mid-March, and French President Macron is under constant pressure following the June European election disaster.

Aggressive ECB easing to continue

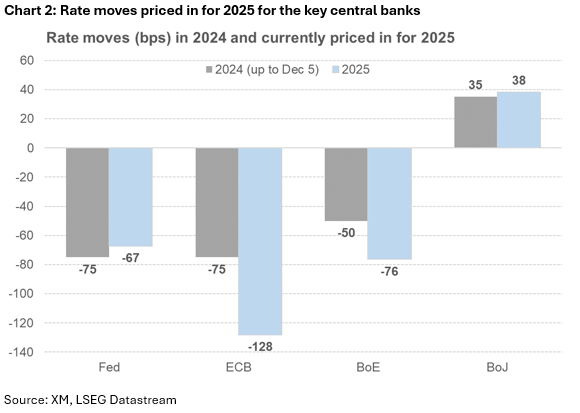

Meanwhile, the European Central Bank (ECB) is expected to further ease its monetary policy stance by around 130bps in 2025, thus decisively contributing to a potential growth pick up. However, the ECB cannot turn the current situation around on its own. Expansionary fiscal policy could be extremely effective at this stage, but, with the COVID pandemic in the rearview mirror, euro area governments have returned to a stricter fiscal doctrine, removing one of the key tailwinds of the economy.

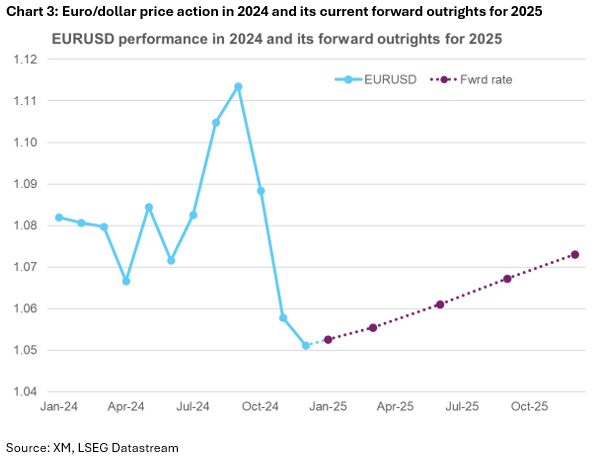

Most market analysts are fairly pessimistic about the euro’s performance in 2025. However, there is an avenue for a brighter performance in 2025 if the euro area manages to return to more respectable growth rates, boosted by consistent wage growth and increased consumer spending, outperforming both the US and UK.

Three external factors could determine euro’s performance

This scenario depends heavily on three factors: (a) Trump’s trade agenda, (b) the Ukraine-Russia conflict, and (c) China’s growth pickup. Should any of these factors prove unfavourable for the euro area, then the euro will most likely remain under pressure during 2025.

Having said that, should global economic performance prove below par in 2025, the ECB’s decisive stance and front-loading strategy could pay some dividends at a time when other major central banks also rush to support their economies, thus inadvertently weakening their currencies.

The pound’s good fortunes could reverse in the latter part of 2025

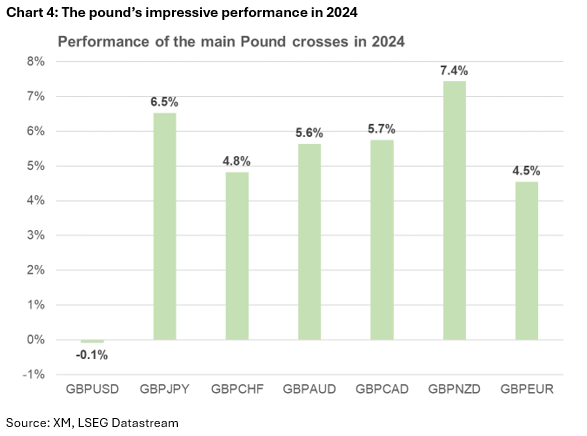

The pound exhibited solid strength during 2024, outperforming the euro for a second consecutive year and barely underperforming against the mighty dollar. The UK Labour party’s comfortable victory in the July 2024 general election and the measured dovish strategy by the Bank of England (BoE) contributed to the pound’s performance. However, both events could come back to haunt the pound during 2025.

While the world prepares for Trump’s second tenure in the White House, the UK is expected to escape relatively unscathed from the newly imposed trade tariffs. However, while the UK might be less affected from a potential deterioration in global trade due to its dominant services sector, the eurozone’s anemic growth means the UK’s economic outlook is not exactly rosy.

The UK budget remains a key unknown for 2025

Domestically, the impact of the 2025 budget is still uncertain. There are increasing concerns that the new tax measures, particularly the rise in employer’s national insurance, could prove counterproductive, hitting both employment and consumption, especially if the government insists on fully implementing these measures. However, there is a non-negligible possibility of amendments if PM Starmer succumbs to pressure from various industry groups, thus easing the overall impact. Meanwhile, the housing sector might be preparing for brighter days ahead, boosting consumer sentiment.

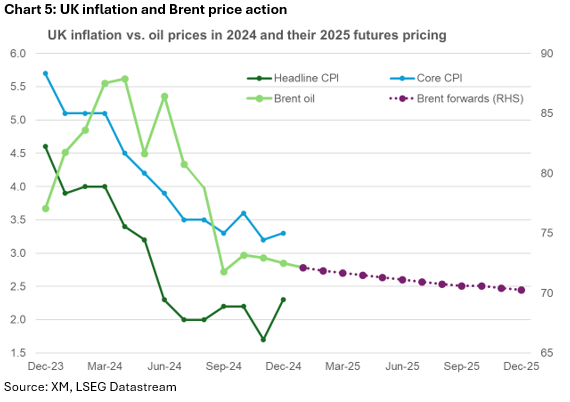

Amidst this environment, the BoE is forecast to continue supporting growth and consumer spending with further rate cuts. The market is currently pricing in 75bps of rate cuts, far less than the 130bps of easing expected by the ECB, which is surprising considering the BoE’s dovish pedigree. Having said that, another trade war could unsettle the BoE’s strategy, especially if core inflation fails to record a sizeable downward trend during 2025.

Pound’s strength could linger in early 2025

Putting everything together, the pound may experience a strong start to the year as the rest of the world scrambles to adjust to Trump’s “America First” agenda. However, this outperformance could moderate later in 2025 if the budget has a damaging effect on consumption, and the world divides into trading blocks, substantially hitting global growth momentum.