{kind=link}

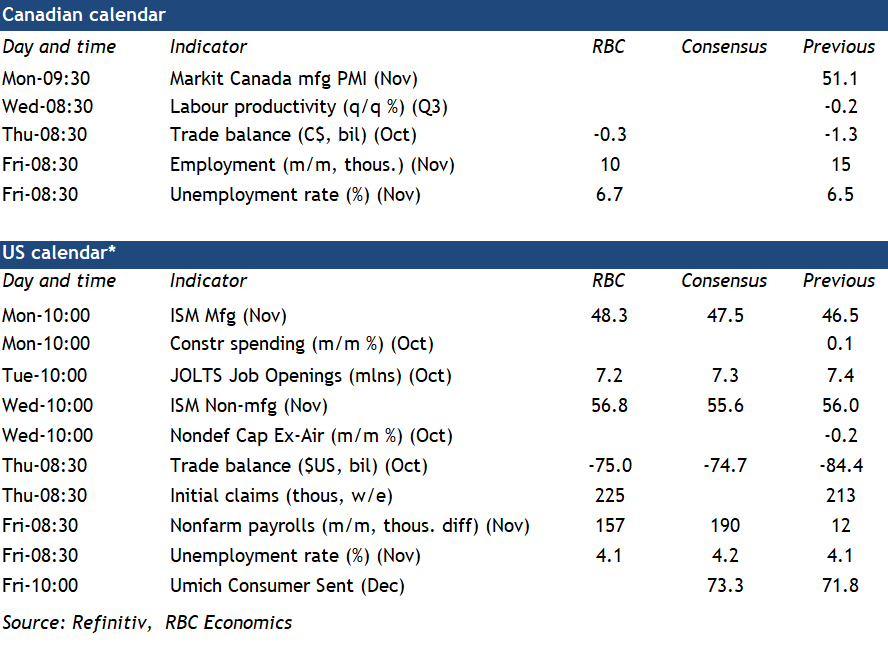

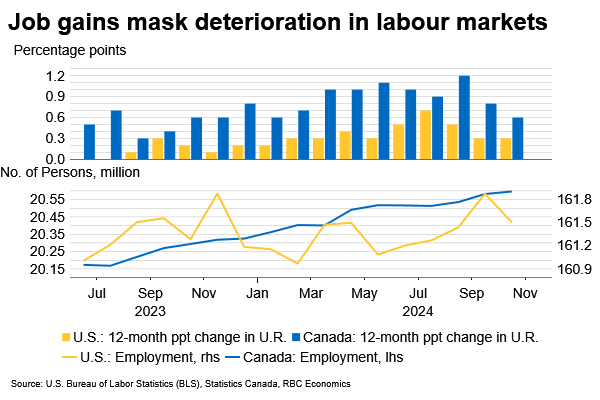

Canadian and U.S. jobs reports on Friday will highlight the growing underperformance of the Canadian labour market compared to the U.S.

We expect Canadian employment edged up 10,000 with the unemployment rate rising to 6.7% in November from 6.5% in October. Canada has steadily posted job growth, but not fast enough to keep up with growth in the labour force as the population continues to rise rapidly. The past two months were an exception—the unemployment rate ticked lower for the first time since January in September and held at that level in October—but largely because of a sharp pullback in the share of, particularly younger, workers giving up their job search. The unemployment rate is still running almost 1 percentage point above year-ago levels and hiring demand has continued to slow with job openings falling. Data from the latest Survey of Employment Payrolls and Hours showed September job openings were still down 18% year-over-year. We expect the labour force participation rate to partially reverse the 0.3 percentage point decline over the last two months.

The U.S. labour market, on the other hand, has remained firm, supported by resilient economic growth. We look for U.S. payroll employment to bounce back 157,000 in November after a 12,000 increase in October. That October increase was the smallest rise since the pandemic, but the reading was distorted by disruptions from hurricanes and strikes. The unemployment rate (which is less impacted by those disruptions) is expected to hold steady at 4.1% for a third consecutive month in November. That would still be up from 3.7% a year ago, but below a recent “peak” 4.3% in the summer.

Beneath the surface, the U.S. labour market is still showing signs of softening. Job openings have continued to fall, and quit rates are at their lowest level since 2020. We continue to expect the unemployment rate will edge higher into next year, but it’s still historically low. We see it “normalizing” rather than faltering with support from an unusually large government budget deficit.

The Bank of Canada and U.S. Federal Reserve will take these employment readings into consideration before their final policy decisions of the year in December. We continue to expect deeper interest rate cuts will come from the BoC than the Fed in the year ahead, reflecting substantial and persistent underperformance in Canadian economic growth and easing inflation pressures.

Week ahead data watch

- We expect the Canadian trade deficit narrowed to $0.3 billion in October from -$1.3 billion in September, mainly driven by higher exports. Oil prices rose in October, pushing up the energy trade balance.

- We expect U.S. trade deficits narrowed to $75B in October. According to the advance trade report, the goods deficit shrank $9.6B, with declines in both goods exports and imports.