{kind=link}

The forex market has turned subdued as the US Thanksgiving holiday curbs activity, but overall trends have held steady. Yen continues to outperform, supported by the ongoing decline in US and European benchmark yields, maintaining its position as the strongest currency this week so far . Euro is the second strongest, showing signs of gaining ground against commodity currencies like the Australian and Canadian Dollars, though it still lacks the momentum needed to decisively advance against Dollar and other European majors.

On the weaker side, Loonie and Aussie remain under pressure, weighed down by US tariff threats targeting Canada and China. Aussie is also being pushed lower by its underperformance against Kiwi, which is benefiting from expectations of a slower rate-cutting cycle in 2025. These expectations were reinforced today by comments from a senior RBNZ official. Dollar is also softer but has yet to confirm a bearish reversal, even against the surging Yen.

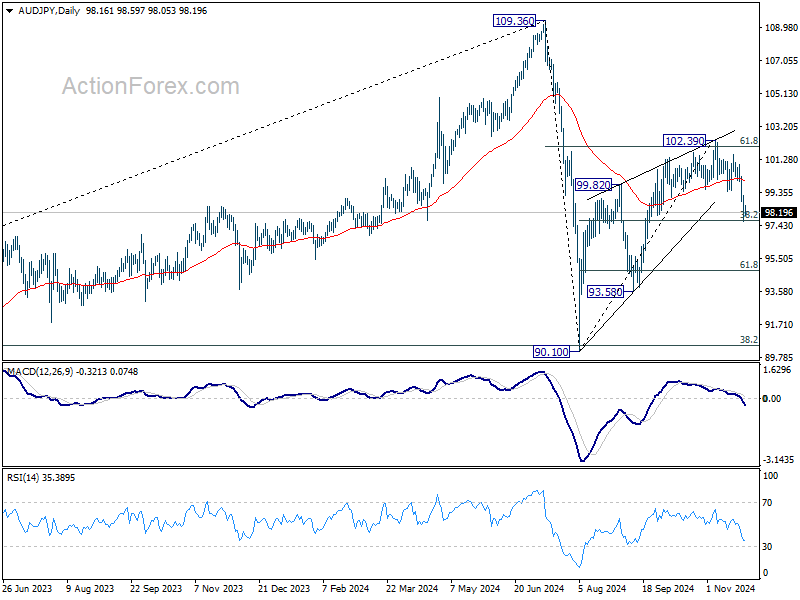

Technically, AUD/JPY is now at a critical juncture, pressing against 38.2% retracement of 90.10 to 102.39 at 97.69. Decisive break below this level would strongly suggest that the corrective rebound from 90.10 has completed with three waves up to 102.39.

In a less bearish scenario, fall from 102.39 could represent the second leg of a medium-term corrective pattern originating at 90.10. However, a more bearish interpretation suggests the decline from 102.39 might be the third leg of a larger correction that began at 109.36.

In either case, firm break of 97.69 would open the door for deeper decline to 61.8% retracement at 94.79.

Also, progression in AUD/JPY’s fall could serve as an early indicator for broader Yen strength across other crosses.

In Asia, at the time of writing, Nikkei is up 0.37%. Hong Kong HSI is down -1.17%. China Shanghai SSE is down -0.08%. Singapore Strait Times is up 0.26%. Japan 10-year JGB yield is down -0.0147 at 1.060. Overnight, DOW fell -031%. S&P 500 fell -0.38%. NASDAQ fell -0.60%. 10-year yield fell -0.060 to 4.242.

RBNZ’s Silk signals slower easing path with potential pauses ahead

Assistant Governor Karen Silk indicated that RBNZ is likely to slow the pace of monetary easing and incorporate pauses into its rate cycle after February.

“There could be pauses built in, but it is definitely a slower track after February,” she noted in an interview with Bloomberg. This aligns with the bank’s updated projections released yesteday.

Silk highlighted the importance of maintaining “mildly restrictive” monetary policy to manage inflationary pressures, particularly as inflation is projected to rise to 2.5% next year.

Looking further ahead, Silk noted that RBNZ expects to be “a little closer” to the long-term neutral rate by the end of 2025. However, she emphasized that current projections do not indicate rates falling “below neutral” at any point during the forecast period.

NZ ANZ business confidence eases to 64.9, outlook continues to brighten

New Zealand’s ANZ Business Confidence dipped marginally in November, falling from 65.7 to 64.9, but it remains at what ANZ describes as an “impressive high” level. Own Activity Outlook, a key forward indicator, rose to a decade high of 48.0 from 45.9, reinforcing optimism about future economic conditions

Inflation related metrics also showed broad improvement, with cost expectations down from 64.2 to 62.9, wage expectations easing from 77.0 to 75.5, and pricing intentions falling from 44.2 to 42.2, marking the first decline in four months. Notably, inflation expectations dropped significantly from 2.83% to 2.53%.

ANZ attributed the robust activity outlook to the impact of interest rate cuts, which are “changing actual behavior, not just expectations.” While the economy remains fragile, ANZ highlighted that “things are starting to turn higher,” with improving activity suggesting early signs of recovery.

RBNZ is likely to take comfort in these trends, as “sufficient domestic disinflation pressure” appears to be in the pipeline, even if growth rebounds faster than expected. However, the survey tempered expectations for aggressive rate cuts, indicating that “large emergency cuts” may not be necessary.

Looking ahead

Germany CPI flash and Eurozone M3 money supply will be released in European session. Canada will release current account. US is on holiday.

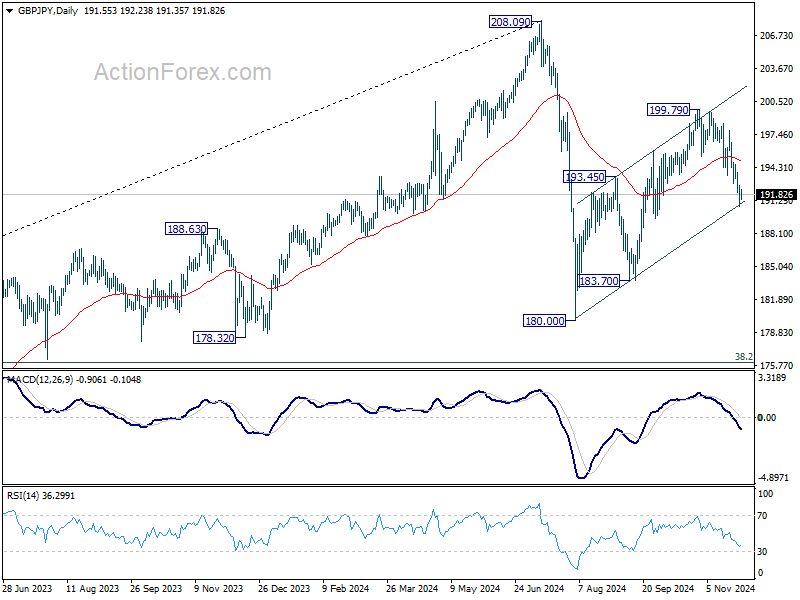

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.66; (P) 191.64; (R1) 192.60; More…

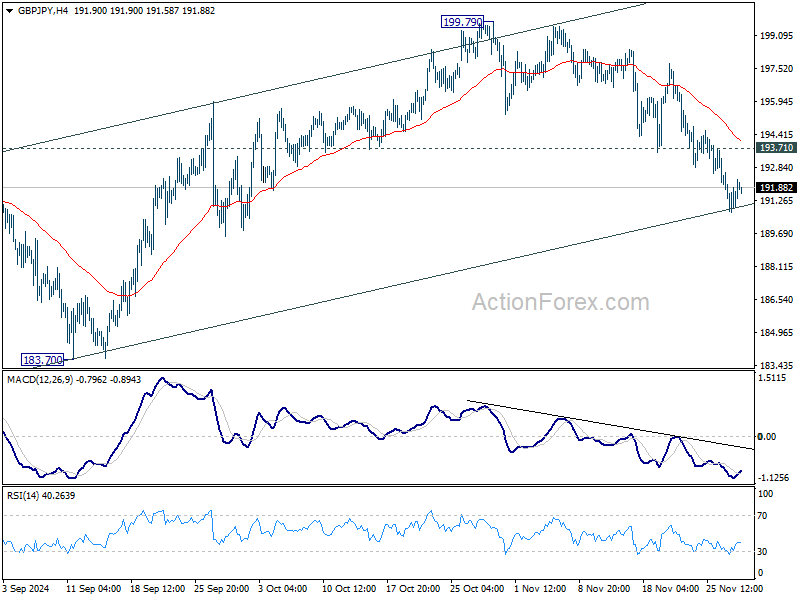

Intraday bias in GBP/JPY remains on the downside as fall from 199.79 is in progress. As noted before, corrective rise from 180.00 could have completed with three waves up to 199.79. Deeper decline would be seen to 183.70 support next. On the upside, above 193.71 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.