{kind=link}

- Almighty dollar awaits PMIs for more signs of Fed cut delays

- Eurozone PMIs also on tap amid speculation of bigger cut by ECB

- Pound could benefit from data pointing to rebound in inflation

- Canadian and Japanese CPI numbers also on the agenda

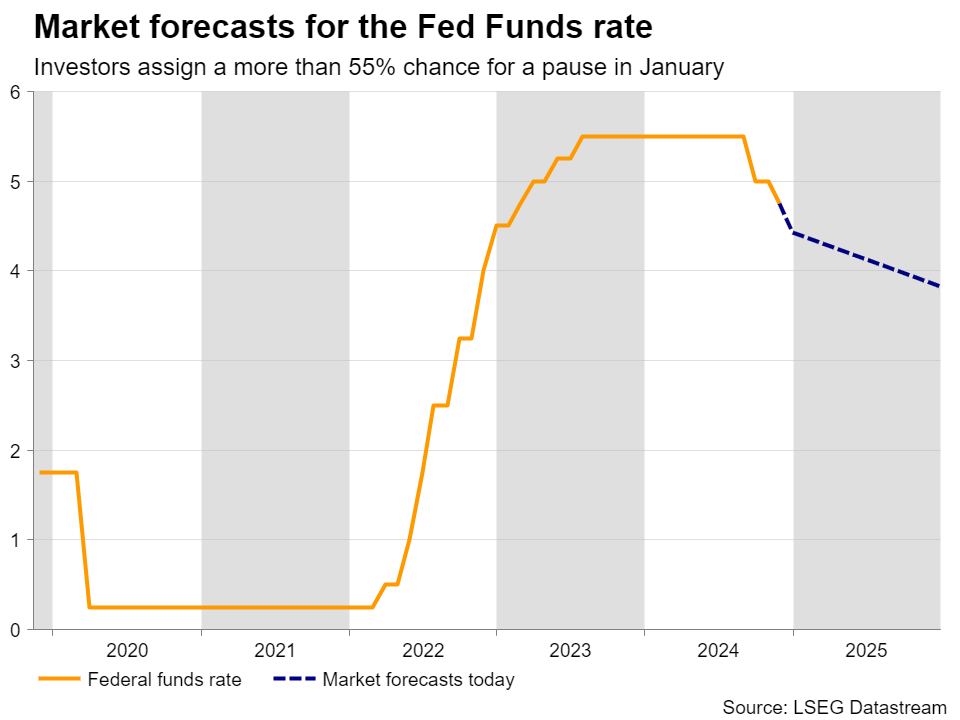

Trump’s election raises bets for a Fed pause

The US dollar continued flexing its muscles for another week, with the so-called ‘Trump trades’ showing no signs of cooling as the president-elect Republican party will control both chambers of the US Congress, which will make it very easy for Donald Trump to turn his pre-election promises into legislation.

The newly elected US president has been advocating for massive corporate tax cuts and tariffs on imported goods from around the globe, especially China, measures that are seen by the financial community as fueling inflation and thereby prompting the Fed to delay future rate reductions.

With the US CPI data already pointing to some stickiness in price pressures during October and Fed Chair Powell noting just yesterday that they do not need to rush in lowering interest rates, more market participants are becoming convinced that the Fed may need to take the sidelines soon. They are assigning a decent 37% chance for this happening in December and a stronger 57% for a January pause.

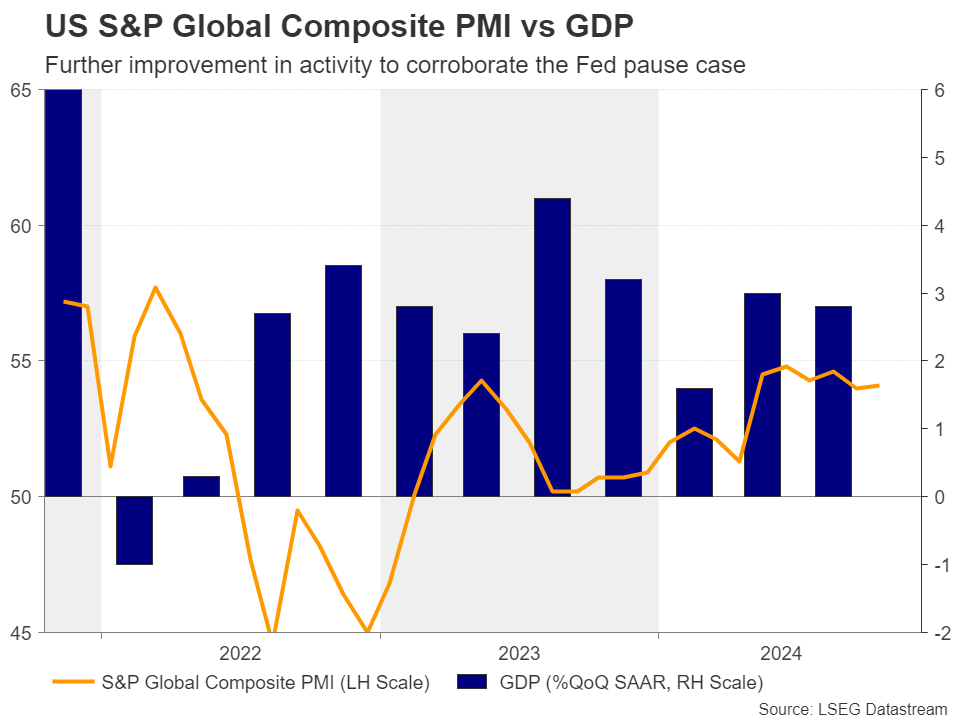

Will the PMIs seal the deal for a Fed pause?

With that in mind, next week, dollar traders may closely monitor the preliminary S&P Global PMI data for the month of November, due out on Friday, for clues as to whether the state of the US economy can indeed allow Fed officials to proceed at a slower pace.

The prices charged subindices may attract special interest as traders may be eager to find out whether the October stickiness rolled over into November. If this is the case, the probability for a January pause may increase further, driving Treasury yields and the US dollar even higher.

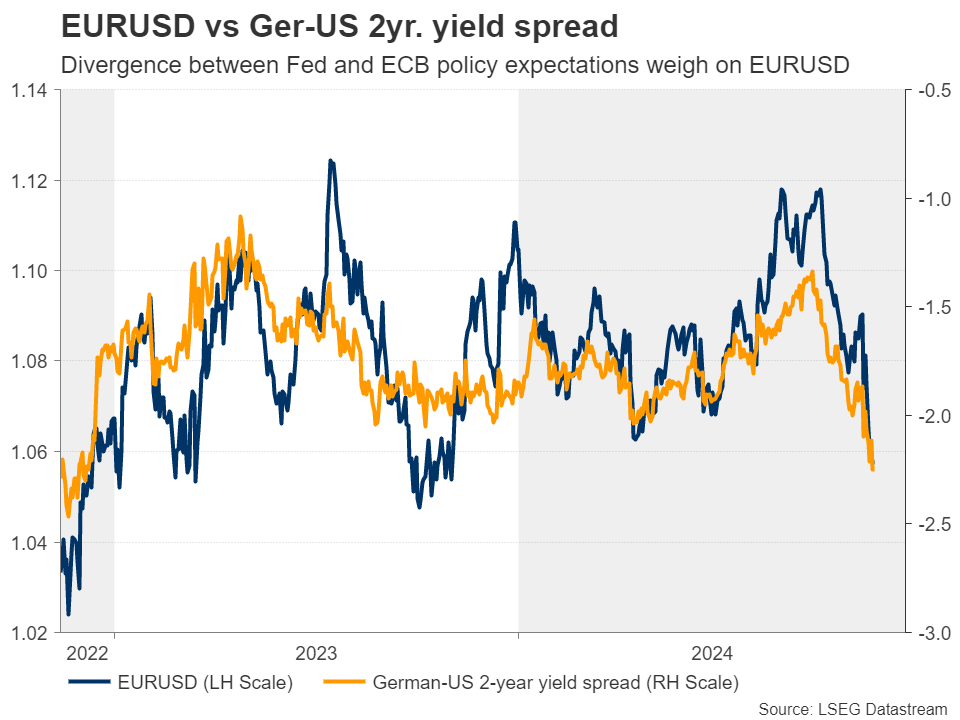

Amidst tariff clouds, euro awaits PMIs as well

On the same day, ahead of the US data, S&P Global will release the Eurozone and UK flash PMIs for November. In the Euro-area, the better-than-expected GDP data for Q3 and the rebound in CPI inflation for October have lessened the likelihood of a 50bps rate cut by the ECB at the upcoming decision.

Nonetheless, concerns that higher tariffs by a Trump-led US government could weigh on the Euro-area economy revived speculation for bold action by the ECB in December, with the euro tumbling to a more-than-one-year low.

Even if the PMIs point to some further improvement in business activity for November, concerns about the impact of Trump’s policies could remain elevated. Therefore, a potential rebound in the euro on the PMIs is likely to stay limited and short-lived.

The uncertainty surrounding Germany’s political scene could also be a headache for euro traders as a lengthy process to form a new coalition government may result in delays in entering negotiations with the US for finding common ground on trade.

Will the UK CPIs reveal early signs of rebound?

In the UK, there are more important releases for pound traders coming in ahead of Friday’s PMIs. On Wednesday, the CPI data for October are coming out, while on Friday, ahead of the PMIs, retail sales are due.

At its latest gathering, the BoE cut interest rates by 25bps but signaled it will proceed with caution on the pace of further easing, prompting market participants to push back their rate cut expectations. There is only an 18% chance for another reduction in December, with a quarter-point cut being fully penciled in for March 2025.

And this is despite the headline inflation rate dropping to 1.7% y/y in September. Perhaps investors have taken into account the still-elevated core rate and the upward revisions of the BoE itself. Just for the record, the Bank has raised its inflation forecast for 2025 to 2.7% y/y from 2.2%.

If Wednesday’s CPI data indeed show early signs of a rebound in price pressures, investors could push further back the timing of the next interest rate cut, something that could prove positive for the pound, especially if Friday’s retail sales come in on the bright side as well.

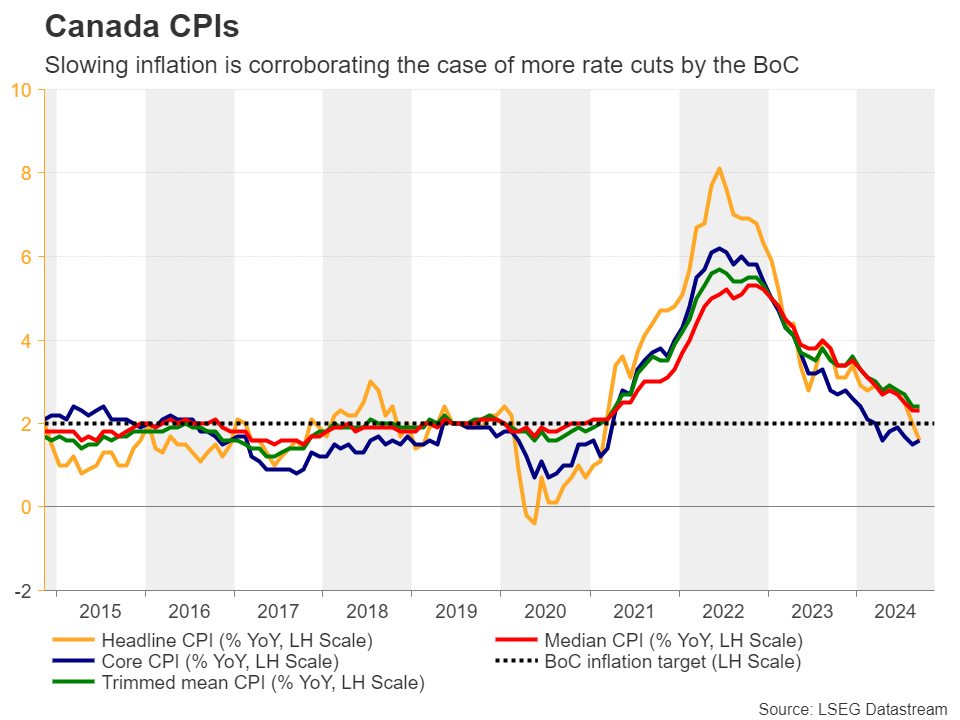

Canadian and Japanese inflation numbers also on tap

More CPI numbers are coming out next week. On Tuesday, the inflation chorus will start with the Canadian numbers, while on Friday, it will end with Japan’s Natonwide CPI data.

In Canada, there is a decent 35% chance for the BoC to deliver a back-to-back 50bps rate cut in December. The jobs data for October have been on the mixed side, with the unemployment rate holding steady at 6.5%, instead of rising to 6.6% as expected, but with the net change in employment slowing more than expected.

The report was not enough to stop the loonie from tumbling against the almighty US dollar, with dollar/loonie now trading at levels last seen in May 2020. Both the headline and core CPI rates stood at 1.6% y/y in October, while the closely watched trimmed CPI held steady at 2.4%. Further cooling may corroborate the notion that there are no upside inflation risks in Canada and may convince more traders to bet on a 50bps reduction in December, thereby pushing the loonie even lower.

In Japan, the BoJ kept interest rates untouched on October 31, but signaled that the conditions for raising rates again are falling into place. This and the latest slide in the yen convinced market participants that Japanese policymakers could hike again at the turn of the year, seeing rates 13bps higher in December and 20 in January.

Having said that though, even if Friday’s CPI data corroborates the view of higher rates soon, any yen recovery is likely to stay limited and short-lived due to further potential strength in the US dollar and due to the hikes being already priced in.