{kind=link}

- Lack of concrete fiscal stimulus measures ex-post China NPC Standing Committee meeting.

- Deflationary and liquidity trap risks are now back in the forefront that may trigger a medium-term negative feedback loop into the Hong Kong & China stocks.

- Watch the 19,700 key support on the Hang Seng Index.

Since hitting a 52-week high of 23,242 on 7 October, the Hang Seng Index has failed to revive its prior bullish momentum that took shape in September on the backdrop of anticipated “more forceful” fiscal stimulus measures to accompany an expansionary monetary policy as China’s central bank, PBoC has cut its policy interest rates and injected more liquidity in the past two months.

After a month of lacklustre performance in October where the Hang Seng Index recorded a monthly loss of 3.9%, the slide failed to reverse and started to gain downside momentum on Monday as it gapped down and shed 1.45% on Monday, 11 November.

The current weakness seen in the Hong Kong stock market has been attributed to the lack of details of the promised fiscal stimulus measures from China to negate the ongoing deflationary spiral that is at high risk of being entrenched in the behaviours of Chinese consumers and businesses.

After a week-long economic-related meeting helmed by the National People’s Congress Standing Committee, China’s policymakers have announced the expected and approved 10 trillion yuan of debt swaps to allow local governments to reduce off-balance sheet hidden debt on late Friday afternoon, 8 November.

However, it stopped short of unleashing new fiscal stimulus to counter a potential increase in trade tariffs towards China goods and services from incoming US President-elect Trump’s White House administration.

Hence, financial market participants have started to lose confidence and patience in the timing and willingness of China’s top policymakers to enact “whatever it takes” bazooka-liked fiscal stimulus measures to jumpstart consumer confidence and spending, which in turn, relay negative feedback loops back into the Hong Kong and China stock markets.

Heightened deflationary spiral and liquidity trap risks

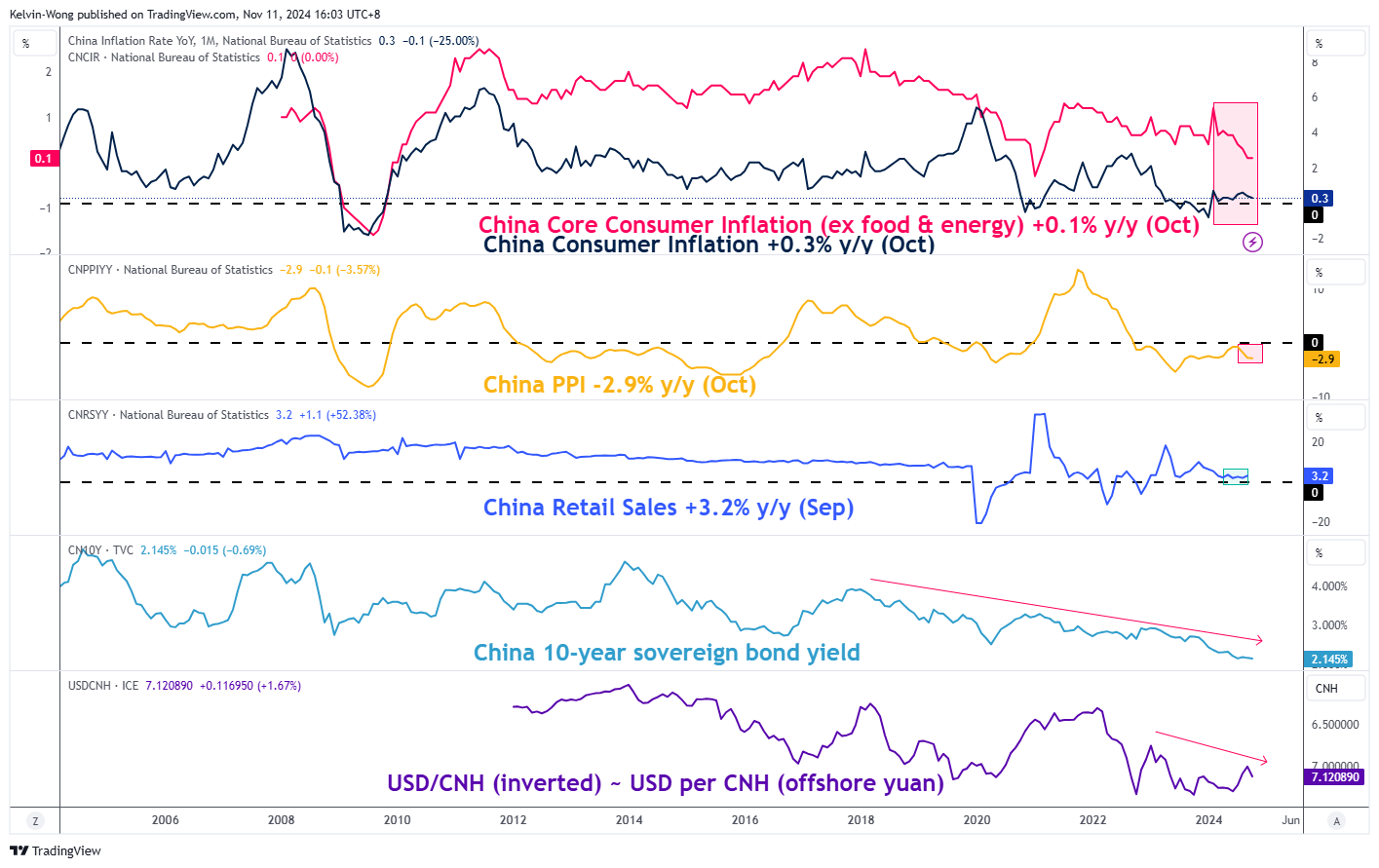

Fig 1: China’s inflation data, 10-year sovereign bond yield & CNH/USD trends as of 31October 2024 (Source: TradingView, click to enlarge chart)

Despite China’s central bank, PBoC’s slew of interest rate cuts and liquidity injections in the past two months, there is still a lack of confidence to trigger a boost in internal demand, and it can be seen apparently in the data of core consumer inflation and producers’ inflation (factory gate prices) that continued to decelerate in October and came in below expectations.

The deceleration of factory gate prices continued to be the main culprit of the ongoing heightened risk of a deflationary spiral unfolding in China. It continued to decline since July, and it fell further to -2.9% y/y in October from -2.8% in September (see Fig 1).

The resultant effect is a continuation of a major impulsive downtrend sequence of the China 10-year sovereign bond yield that led to a total wipeout of the gains seen in the offshore yuan against the US dollar in September, induced by the first US Federal Reserve’s interest rate cut.

Overall, a resurgence of a major weakening trend of the offshore yuan is likely to trigger a negative double whammy for Hong Kong and China stocks.

Watch the 19,700 support on the Hang Seng Index

Fig 2: Hang Seng Index medium-term & major trends as of 12 Nov 2024 (Source: TradingView, click to enlarge chart)

The Hang Seng Index ended Tuesday, 12 November session on a weak footing as it declined by 2.8% and hit a six-month low despite a positive news flow that reported that China authorities are likely to cut home buying taxes soon to as low as 1% from the current level of 3%.

The daily RSI momentum has just staged a bearish breakdown below a parallel ascending trendline support and inched below the 50 level which suggests a potential resurgence of medium-term bearish momentum.

A break with a daily close below 19,700 key medium-term pivotal support (also the 50-day moving average) may see further weakness to expose the next medium-term supports at 17,900 (also the 200-day moving average) and 16,610 (see Fig 2).

Clearance above the 21,420 intermediate resistance may dissipate the bearish tone for the medium-term resistance to come in at 22,690 in the first step.