{kind=link}

In the largely uneventful Asian and European sessions today, major currencies remained within familiar ranges, as the absence of key economic data releases kept markets subdued. Central bank commentary continued to dominate the narrative, particularly from ECB officials, who maintained their dovish stance. However, this comes as little surprise, with expectations largely baked in that ECB is likely to reduce rates again in December unless a sharp improvement in economic activity or inflation data emerges.

On the currency front, Swiss Franc and Dollar are the stronger performers, followed by Euro. Yen, however, turned under pressure as the weakest currency today, with Aussie and Sterling also facing losses. Canadian Dollar and New Zealand Dollar are positioned in the middle. But overall, major pairs and crosses remain range-bound, with today’s moves offering little insight into underlying trends.

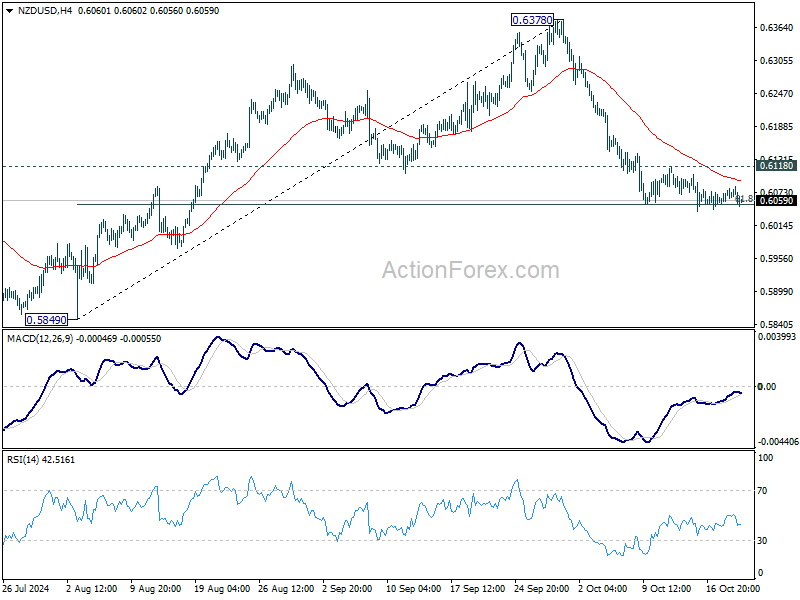

Technically, NZD/USD continues to press 61.8% retracement of 0.5849 to 0.6378 at 0.6051, and it should be about time for a breakout from the tight range. Decisive break of 0.6051 would resume the fall from 06378 towards 0.5849 support Nevertheless, strong bounce from current level, followed by break of 0.6118 resistance will argue that the fall has completed an bring stronger rebound towards 0.6378 instead.

In Europe, at the time of writing, FTSE is down -0.29%. DAX is down -0.78%. CAC is down -0.75%. UK 10-year yield is up 0.064 at 4.118. Germany 10-year yield is up 0.081 at 2.272 Earlier in Asia, Nikkei fell -0.07%. Hong Kong HSI fell -1.57%. China Shanghai SSE rose 0.20%. Singapore Strait Times fell -0.70%. Japan 10-year JGB yield fell -0.0086 to 0.962.

ECB’s Kazimir: Disinflation progress encouraging, but further proof needed

ECB Governing Council member Peter Kazimir expressed growing confidence in the disinflation trend, stating in a blog post today that the path to lower inflation appears to be on “solid footing”.

Kazimir added that if upcoming data continues to confirm accelerated disinflation, the ECB would be in a “strong and comfortable position to continue the easing cycle.”

However, he noted that wage growth and services inflation, two critical elements, have yet to show the expected decline. He added, “If new information points toward higher inflation, we can still slow down the pace at which we remove restrictions in the coming meetings.”

ECB’s Simkus: Rates to move toward neutral as disinflation stays on track

ECB Governing Council member Gediminas Simkus commented today that the disinflationary trend is progressing steadily, though he acknowledged that services inflation remains elevated.

Simkus expects monetary policy to gradually become less restrictive, with the central bank lowering interest rates toward a “natural” level, estimated to be between 2-3%.

However, he emphasized that if the disinflation process becomes deeply “entrenched”, rates could potentially fall below the natural level.

RBA’s Hauser signals no early rate cuts as inflation remains too high

RBA Deputy Governor Andrew Hauser emphasized today that inflation remains “too high” for the central bank to consider immediate rate cuts.

Recent strong employment data led markets to push back the expected timing for the first rate cut from February to April. Hauser refrained from commenting on the market’s pricing, but noted, “the response of rates to the data does seem to be quite encouraging.”

While acknowledging the importance of data, Hauser stressed that RBA is “data-dependent but not data-obsessed,” noting that broader economic conditions also factor into policy decisions.

“Activity has been weak, very weak, and we haven’t seen the inflation number for the third quarter yet,” he added.

The RBA’s cautious approach contrasts with other central banks that have already begun easing, highlighting Australia’s persistent inflationary pressures. The market will be closely watching the third-quarter inflation data to gauge the timing and magnitude of future policy changes.

PBoC slashes loan prime rates

People’s Bank of China lowered its one-year loan prime rate to 3.1% and trimmed the five-year LPR to 3.6%, as anticipated by market watchers. This move, at the upper end of the 20-25 basis point range suggested by Governor Pan Gongsheng during a Beijing forum last Friday, impacts a broad spectrum of loans in China. The one-year LPR directly influences corporate and household loans, while the five-year LPR serves as a benchmark for mortgage rates.

While this rate cut signifies some level of monetary stimulus, analysts continue to stress that China’s core issue is not the supply of credit, but rather a lack of demand. Many argue that without substantial fiscal stimulus, the impact of these rate adjustments will remain muted.

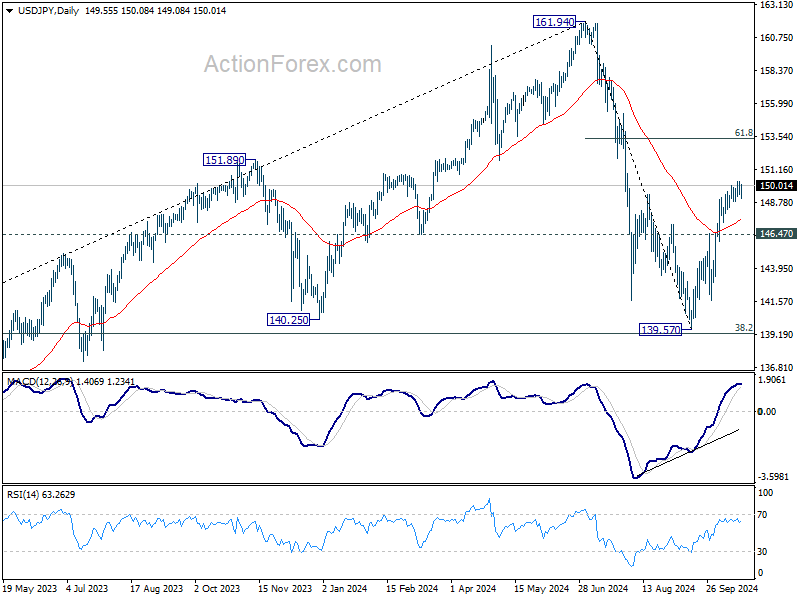

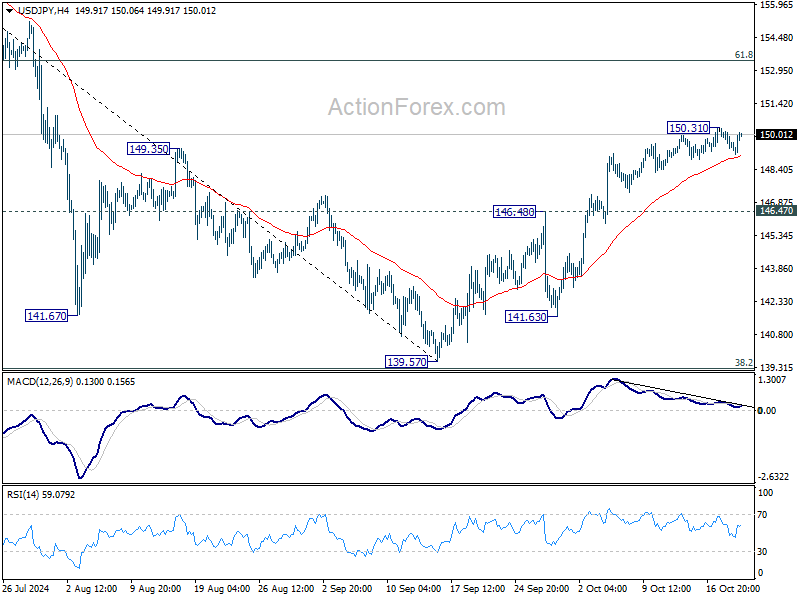

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.19; (P) 149.74; (R1) 150.10; More…

USD/JPY recovered mildly ahead of 4H MACD, but stays below 150.31 temporary top. Intraday bias remains neutral first. Further rally is expected as long as 146.47 resistance turned support holds. Above 150.31 will resume the rebound from 139.57 to 61.8% retracement of 161.94 to 139.57 at 153.39. However, break of 146.48 resistance turned support will indicate that rebound from 139.57 has already completed.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should now be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.