have started to show signs of fatigue despite a string of record highs reached in the past four weeks.){kind=link}

- Trump’s trade war 2.0 narrative & steep sell-off in ASML spooked the performances of the major US stock indices on Tuesday, 15 October.

- Implied volatility in the US stock market, measured by the VIX tends to be highest in October based on data during past US presidential election years since 1992.

- VIX/MOVE ratio has started to show outperformance of VIX.

- The S&P 500’on-going 4-week rally has flashed out exhaustion conditions.

The S&P 500 shed 0.75% on Tuesday, 15 October after it printed its 46th record high for 2024 on Monday.

Yesterday’s daily loss of 0.75% was the largest seen in the past two weeks and attributed to the underperformance of the artificial intelligence (AI) juggernaut, Nvidia (second largest market cap stock in the S&P 500) which tumbled by 4.68% after a related bellwether semiconductor chip-making equipment firm, ASML issued a downgrade to its revenue guidance for 2025 that saw its share price plummeted by 16%, its worst daily performance since 12 June 1998.

In addition, an adverse macro factor also attributed to yesterday’s weakness inflicted in all the major US stock indices except for the Russell 2000 which closed almost unchanged; Nasdaq 100 (-1.37%) and Dow Jones Industrial Average (-0.75%).

US trade tensions with China narrative is now back on the radar of market participants after US Republican presidential nominee Donald Trump reaffirmed his preference for higher tariffs on China and the rest of the world’s exports to the US as he remarked that “tariffs are the most beautiful word in the dictionary” during yesterday’s live in-person interview with Bloomberg News organized by The Economic Club of Chicago.

With less than four weeks to go before the 5 November US presidential election day, betting markets are now indicating Trump has a lead of 56% over Democratic presidential nominee Harris (43%) according to betting average data as of 15 October compiled by Real Clear Politics.

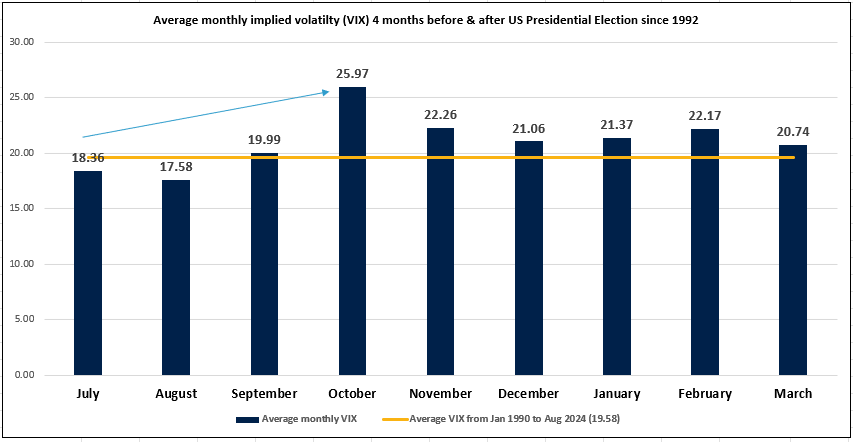

October recorded the highest level of VIX during past US presidential election years

Fig 1: Average monthly VIX during US presidential election years since 1992 as of 2 Aug 2024 (Source: TradingView)

Regardless of who wins the White House race, based on past data during US presidential election years since 1992, the VIX, a measurement of the implied volatility of the US S&P 500 has increased in the four months (July to October) before the election month of November; a jump of around 40 percent, and reach an average monthly high of 25.97 in October (see Fig 1).

Hence, the S&P 500 now faces an increased risk of a jump in the VIX which in turn may spark a multi-week risk-off episode in the global financial markets.

VIX is now showing outperformance conditions over the MOVE Index

Fig 2: Major trends of MOVE Index, VIX & VIX/MOVE ratio as of 16 Oct 2024 (Source: TradingView)

The Merrill Lynch Option Volatility Estimate (MOVE) Index reflects the level of volatility in U.S. Treasury futures. The index is considered a proxy for term premiums of U.S. Treasury bonds (the yield spread between long-term and short-term bonds).

The movement of the MOVE Index has a strong direct correlation with VIX (implied volatility of the US stock market; S&P 500) since 2018 (see Fig 2).

Since the week of 16 September 2024, the MOVE Index has surged upwards significantly and cleared above a key medium-term resistance of 112.80.

The VIX has tagged along as well but has yet to break above its key medium-term resistance of 23.38 (currently trading at 20.80).

Interestingly, the ratio of VIX/MOVE has printed a series of “higher lows” and staged a bullish breakout from a major descending trendline resistance on the week of 15 July 2024 which suggests outperformance conditions of the VIX over MOVE Index have surfaced.

All these observations suggest a potential imminent jump in the VIX.

Watch the 5,930 key resistance on the S&P 500

Fig 3: Medium-term & major trends of the US S&P 500 CFD Index as of 16 Oct 2024 (Source: TradingView)

In the lens of technical analysis, the price actions of the US S&P 500 CFD Index (a proxy of the S&P 500 E-mini futures) have started to show signs of fatigue despite a string of record highs reached in the past four weeks.

Since 22 August 2024, the US S&P 500 CFD Index has evolved into a bearish “Ascending Wedge” configuration coupled with a bearish divergence condition sighted on the MACD Histogram in the same period which suggests its medium-term upside momentum has started to wane.

5,930 key medium-term pivotal resistance on the Index and a break below 5,675 key intermediate support (also the 50-day moving average) is likely to trigger a medium-term (multi-week) corrective decline sequence to expose the next medium-term supports of 5,390 (close to the 200-day moving average) and 5,100 (see Fig 3).

On the flip side, a daily close and a clearance above 5,930 invalidate the bearish scenario for a continuation of the impulsive upmove for the next medium-term resistances to come in at 6,110/130 and 6,390 (also the upper boundary of the major ascending channel in place since March 2020 pandemic low).