markets’ positioning in any profound way (> 90% chance of a 25 bps cut in November and slightly less than 50% chance on an additional step in December). The unemployment rate declined to 4% from 4.1%. Employment growth in the 3M to August accelerated to 373k (from 265k), but a preliminary figure for September (payrolled employees) shows signs of a slowdown (-15k). Average weekly earnings (ex-bonus) as expected eased to 4.9% from 5.1%, but this is probably still too high to sustainably return inflation back to 2%. Tomorrow’s price data and/or Friday’s retail sales could still provide a more straightforward narrative. UK bond yields basically follow the broader decline in US Treasuries and Bunds. Sterling again outperforms (cable 1.3085; EUR/GBP 0.8335, nearing the October 01 correction low of 0.831).){kind=link}

Markets

The release of labour market data kicked off a triptych of key UK data that should help clarify whether the time is right for the BoE to move to a ‘more activist approach’ when it comes to reducing policy restriction. The employment report didn’t change (money) markets’ positioning in any profound way (> 90% chance of a 25 bps cut in November and slightly less than 50% chance on an additional step in December). The unemployment rate declined to 4% from 4.1%. Employment growth in the 3M to August accelerated to 373k (from 265k), but a preliminary figure for September (payrolled employees) shows signs of a slowdown (-15k). Average weekly earnings (ex-bonus) as expected eased to 4.9% from 5.1%, but this is probably still too high to sustainably return inflation back to 2%. Tomorrow’s price data and/or Friday’s retail sales could still provide a more straightforward narrative. UK bond yields basically follow the broader decline in US Treasuries and Bunds. Sterling again outperforms (cable 1.3085; EUR/GBP 0.8335, nearing the October 01 correction low of 0.831).

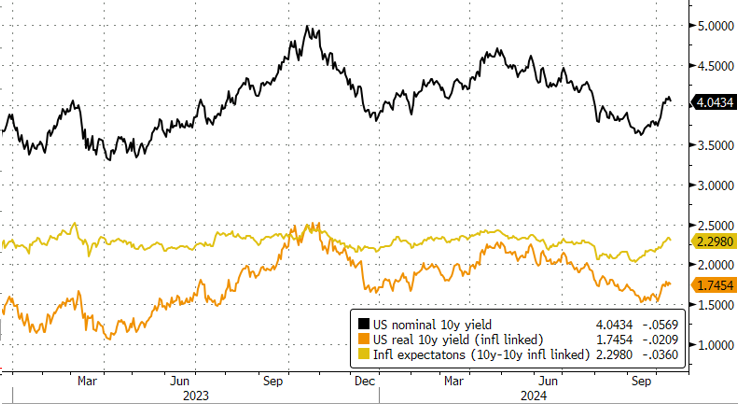

US interest rate markets reopened after the Columbus Day holiday. Yesterday’s sharp drop in oil prices limited any tentative further upside pressure in inflation expectations and in US (and other core) yields. A weak NY Fed Empire Manufacturing survey (-11.9 from +11.5 vs 3 expected) pointed in the same direction. For now, the ‘hawkish’ repricing after stronger than expected early month US data has run its course. US yields decline between 3 bps (2-y) and 6.5 bps (30-y). German Bund yields are easing 4 to 5 bps across the curve. The expectations index of ZEW German investor sentiment improved slightly more than expected from 3.6 to 13.1, but understandably had hardly any impact on market pricing. After yesterday’s record levels for the Dow and the S&P 500, US equities show no clear trend even as US banks’ earnings published today mostly beat market expectations. After yesterday’s setback, Brent holds below $75/b. Lower core yields also prevent the dollar from building on its recent uptrend. DXY eases slightly (103.05) as nearby resistance (103.34, 50% retracement on April-September decline) is in play. The comparable level in EUR/USD (1.0907) looked like being broken this morning, but EUR/USD intraday also got some reprieve from lower US yields (1.0915 currently). Still the picture remains fragile.

News & Views

Canadian inflation just missed the bar in September. Headline prices dropped 0.4% m/m (-0.3% expected), bringing Y/Y reading down from 2% to 1.6%. That’s below the 1.8% estimate and the lowest since February 2021, after which the post-pandemic inflation surge began to materialize. Core readings (ex gasoline, median, trimmed) matched the August readings of 2.2-2.4%, compared with expectations for a slight acceleration in one of the three key metrics. Statistics Canada attributed the sharp drop of the headline Y/Y figure to energy (gasoline, -7.1% m/m following a 2.6% decline in August). Shelter price rises decelerated from 0.4% to 0.1% m/m. Clothing & footwear (+0.9% m/m) and health & personal care (+0.5%) printed some of the largest monthly gains. In sectoral terms, goods prices dropped for a second month straight by 0.6%, joined by a second consecutive easing in services prices (-0.2%). The CPI news comes after last week’s solid labour market report. In the end, it didn’t change much to market expectations (+/- 50%) of the Bank of Canada moving ahead in bigger steps, something governor Macklem didn’t rule out in September. Conviction grows today to more than 75% of a 50 bps move on October 23. The Canadian Loonie is headed for a tenth day of losses. USD/CAD pushes beyond 1.38(3).

The Polish government today launched a dual EUR-denominated bond sale. Its return to the FX bond market after several months of silence comes after the draft 2025 budget showed a jump in bond sales (net borrowing needs rise from PLN 215.7bn to PLN 366.9bn) in that presidential pre-election year. By tapping the international bond market, the Ministry of Finance seeks to further diversify funding. Poland successfully raised €1.75bn at MS+85 bps for its 7-yr (Oct 22, 2031) bond and €1.25bn for the 15-yr one (Oct 22, 2039) at MS+140. Books ran above €8.9bn for the former and €6.5bn for the latter. The sale follows the biggest EUR-denominated one (dual-tranche) ever in early January, tapping a combined €3.75bn. It raised $8bn from a sale in US dollars back in March.

Graphs

USD/CAD: Loonie stays in the defensive as markets see growing chance of 50 bps BoC rate cut

EUR/GBP nears YTD low as UK data provide ‘final input’ for November 07 BoE meeting.

US 10-y yields: decline in oil prices caps rebound in inflation expectations (yellow).

S&P 500 continues record race on combinaition of solid US growth and hoped for easing of financial conditions.