{kind=link}

Canadian Dollar weakens broadly decline in early US session following weaker-than-expected inflation data. The drop in headline CPI, driven primarily by falling gasoline prices, was steeper than anticipated. However, core inflation measures, especially the closely-watched CPI common, remained near 2% level. This further solidifies expectations that BoC would accelerate its policy easing, with a 50bps rate cut likely at the October 23 meeting.

In contrast, British Pound found some support from a mixed set of labor market data. UK unemployment rate unexpectedly fell to 4%, while wage growth slowed to its lowest point in over two years. This data leaves the decision for a BoE rate cut in November finely balanced. However, the market’s focus is now shifting to tomorrow’s UK CPI release, which is expected to carry more weight in shaping BoE’s course of action.

For the day, Yen has surprising emerged as the strongest performer. Many traders are still hesitant to push USD/JPY above 150 psychological level. Sterling follows, while the Swiss Franc also shows strength. Canadian Dollar is the weakest performer so far, followed by Australian and New Zealand Dollars. The continued uncertainty over China’s fiscal policy, despite another upcoming press conference from key ministries, is keeping sentiment subdued for Chinese and Hong Kong stocks, weighing further on the Aussie and Kiwi.

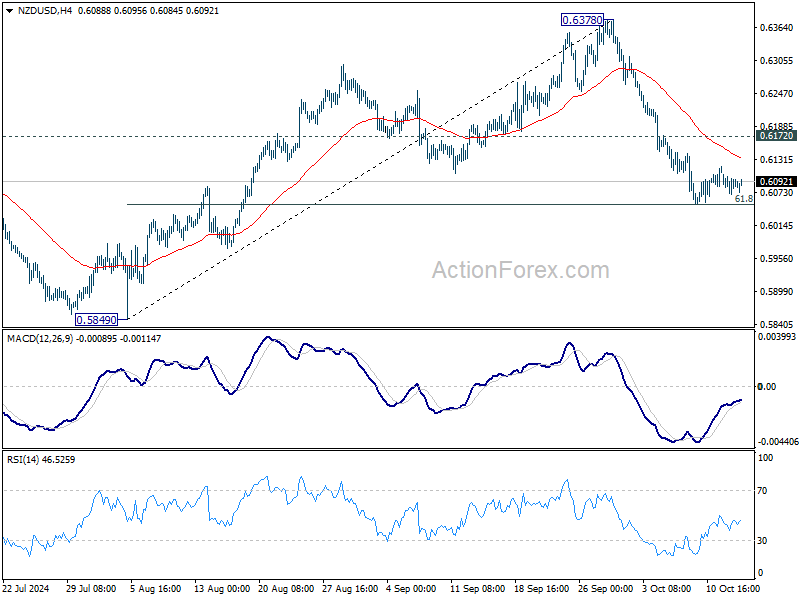

Looking ahead, New Zealand’s CPI data, to be released in the next Asian session, could be pivotal in determining whether the RBNZ will follow through with a second 50bps rate cut in November. Technically, NZD/USD continues to hover in tight range above 61.8% retracement of 0.5849 to 0.6378 at 0.6051. Further decline is expected as long as 0.6172 resistance holds. Firm break of 0.6051 will extend the decline from 0.6378 to 0.5849 support next.

In Europe, at the time of writing, FTSE is down -0.42%. DAX is up 0.30%. CAC Is down -0.91%. UK 10-year yield is down -0.0571 at 4.185. Germany 10-year yield is down -0.049 at 2.232. Earlier in Asia, Nikkei rose 0.77%. Hong Kong HSI fell -3.67%. China Shanghai SSE fell -2.53%. Singapore Strait Times fell -0.01%. Japan 10-year JGB yield rose 0.0241 to 0.976.

Canadian CPI down -0.4% mom in Sep, annual rate slows to 1.6% yoy

Canada’s CPI fell -0.4% mom in September, much worse than expectation of -0.2% mom. Over the 12-month period, CPI slowed from 2.0% yoy to 1.6% yoy, below expectation of 1.8% yoy. That was the lowest figure since February 2021. The main contributor to headline deceleration was lower year-over-year prices for gasoline in September (-10.7%). CPI ex-gasoline was unchanged at 2.2% yoy.

The core measures showed CPI median unchanged at 2.3% yoy. CPI trimmed unchanged at 2.4% yoy. CPI common rose from 1.9% yoy to 2.1% yoy. All matched expectations.

Germany’s ZEW jumps to 13.1 in Oct, driven by optimism on inflation and ECB rate cuts

Germany’s ZEW Economic Sentiment index surged significantly to from 3.6 to 13.1 in October, surpassing market expectations of 10.2. However, Current Situation Index dropped further into negative territory, falling from -84.5 to -86.9, slightly worse than forecast of -85.0.

For the Eurozone, ZEW Economic Sentiment rose from 9.3 to 20.1, beating expectations of 16.9. Current Situation Index, however, saw a small decline, edging lower by -0.4 points to -40.8.

ZEW President Achim Wambach highlighted the mixed signals, noting that despite a very weak current economic situation in Germany, optimism is growing. He cited “stable inflation” expectations and the prospect of “further interest rate cuts” by ECB as key contributors to this improved outlook.

Wambach added that positive signals from key export markets such as the US, China, and the Eurozone also played a role in improving the outlook for Germany’s economy. China’s recent economic stimulus measures have contributed to this optimism too, boosting expectations for Germany’s exports.

Eurozone industrial production rises 1.8% mom in Aug, driven by capital goods

Eurozone industrial production increased by 1.8% mom in August, meeting market expectations. This growth was supported primarily by a significant 3.7% rise in capital goods production. Durable consumer goods also saw a notable rise of 1.7%, while energy production edged up by 0.4%. However, intermediate goods saw a contraction of -0.3%, and non-durable consumer goods posted a modest gain of 0.2%.

Across the broader European Union, industrial production rose by 1.3% mom. Ireland led the gains with a robust 4.5% rise, followed by Germany and Lithuania, which both saw increases of 3.3%. Malta also posted solid growth of 2.7%. On the downside, Luxembourg experienced a sharp decline of -9.2%, while Croatia and Denmark saw drops of -4.6% and -4.5%, respectively.

UK payrolled employment falls -15k in Sep, unemployment rate dips to 4% in Aug

In September, UK payrolled employment decreased -15k or -0.0% mom, but increased by 113k or 0.4% yoy, to 30.3m. Median monthly pay rose 5.3% yoy, down from prior 6.0% yoy, but stays well above June’s 3.8% yoy. Claimant count rose 27.9k to 1.797m, above expectation of 20.2k.

In the three months to August, unemployment rate fell from 4.1% to 4.0%, below expectation of 4.0%. Average regular earnings excluding bonuses rose 4.9% yoy, down from prior 5.1% yoy, below expectation of 5.0% yoy. Average regular earnings including bonuses rose 3.8% yoy, down from prior 4.0% yoy, matched expectations.

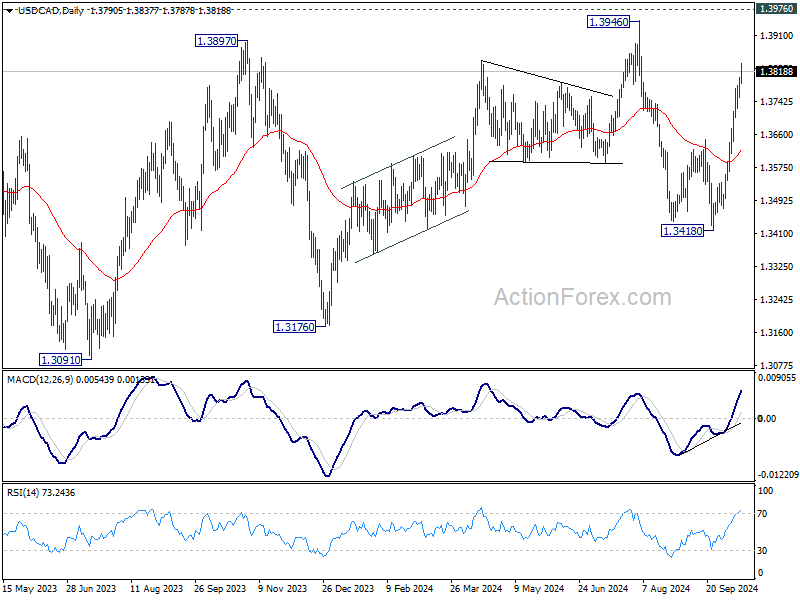

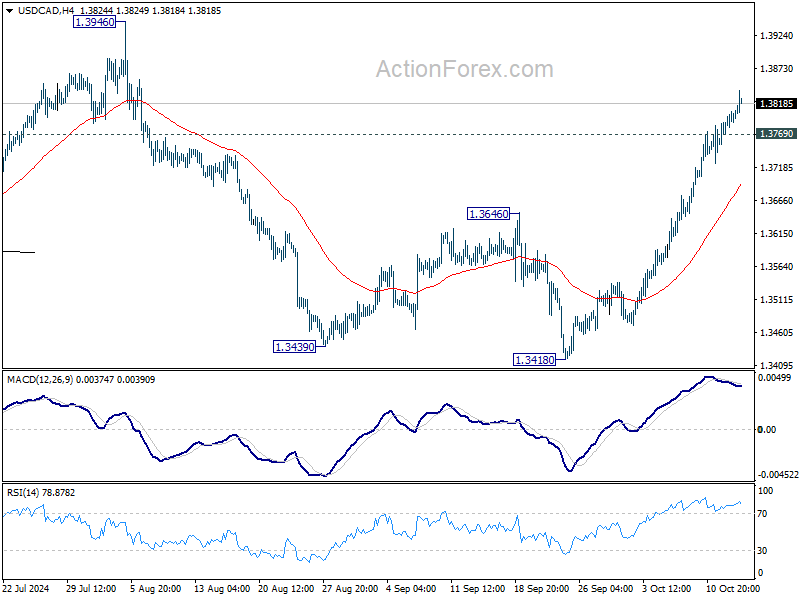

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3768; (P) 1.3786; (R1) 1.3816; More…

Intraday bias in USD/CAD remains on the upside as rise from 1.3418 is in progress. Next target is a test on 1.3946/76 key resistance zone. On the downside, 1.3769 minor support will turn intraday bias neutral first. But further rally will be expected as long as 1.3646 resistance turned support holds, in case of retreat.

In the bigger picture, sideway consolidation pattern from 1.3976 (2022 high) might still extend further. While another decline cannot be ruled out, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.