{kind=link}

The Monday Asian session started quietly with Japan on holiday and the US and Canada on extended weekends. Market reactions to China’s Minister of Finance press briefing over the weekend have been subdued, as traders await further details regarding China’s anticipated fiscal stimulus. Without specifics, it’s difficult to gauge the broader impact on the country’s economic outlook.

In the currency markets, Dollar is currently leading gains, followed by British Pound and Canadian Dollar. On the downside, New Zealand Dollar is the weakest, followed by Australian Dollar and Swiss Franc. Euro and Japanese Yen are trading in the middle. But most major pairs are just confined within Friday’s narrow trading ranges. The key event of the week will be the anticipated ECB rate cut, while inflation data from the UK, Canada, and New Zealand will also be closely monitored for further policy signals.

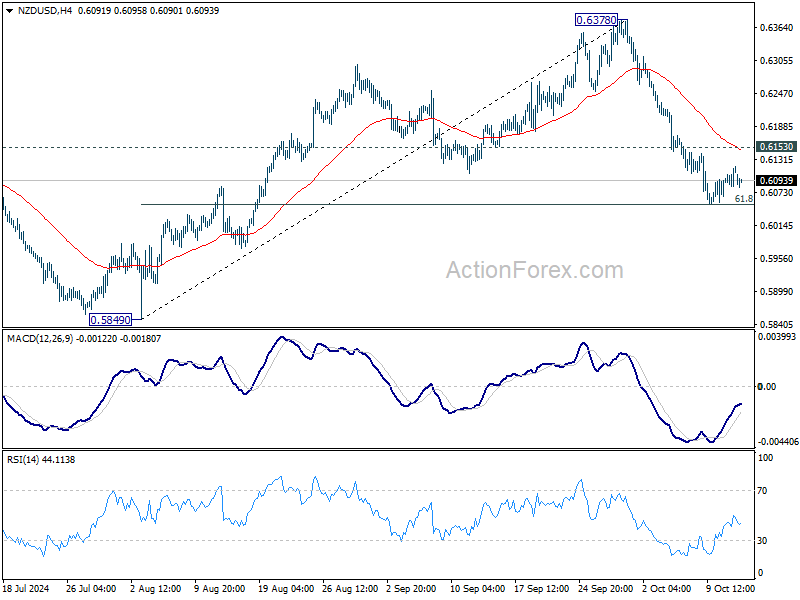

Technically, NZD/USD recovered after touching 61.8% retracement of 0.5849 to 0.6378 at 0.6051. But outlook will stay bearish as long as 0.6153 resistance holds. Decisive break of 0.6051 will bring deeper fall back to 0.5849 support next. The upcoming Q3 CPI data from New Zealand could play a critical role in determining the pair’s next move.

In Asia, at the time of writing, Hong Kong HSI is down -0.10%. China Shanghai SSE is up 1.87%. Singapore Strait Times is up 0.42%. Japan is on holiday.

China’s CPI falls back to 0.4% yoy in Sep, PPI down -2.8% yoy

China’s inflation data for September, released over the weekend, showed continuously weak price momentum.

Headline CPI growth slowed to 0.4% yoy, down from 0.6% yoy in August and missing market expectations of 0.6%. Core CPI, which excludes volatile food and energy prices, rose by just 0.1% yoy, its lowest reading since February 2021. This marked the 20th consecutive month in which core inflation remained below 1.0%, underscoring persistent weak domestic demand and the need for stronger economic stimulus to encourage consumer spending.

Food prices remained a key driver of inflation, with a 3.3% yoy increase. Vegetable prices surged by 22.9% yoy, and pork prices jumped by 16.2% yoy. These spikes in food costs contributed to the overall rise in consumer prices, but price weakness in other areas remains a concern. For instance, prices of new energy vehicles, which face international tariff pressures, fell by -6.9% yoy.

On the industrial front, PPI fell by -2.8% yoy in September, deeper than the -1.8% yoy decline in August and missing expectations of a -2.5% yoy drop. This marked the 24th consecutive month of negative PPI readings

New Zealand BNZ services unchanged at 457, stuck in contraction

New Zealand’s BusinessNZ Performance of Services Index was unchanged at 45.7 in September, marking the seventh consecutive month in contraction and remaining well below the long-term average of 53.1.

Katherine Rich, CEO of BusinessNZ, noted that the services sector appears to be “stuck in a rut” and is struggling to get out of contraction.

The detailed data reflects mixed performance across key components. While activity/sales edged slightly higher from 44.3 to 45.6, employment saw a sharp decline, dropping from 49.4 to 45.7—reflecting further weakness in job creation. New orders/business also ticked down marginally from 46.9 to 46.7, while supplier deliveries dipped further to 43.2 from 43.5.

One small positive came from a reduction in the proportion of negative comments from respondents, which fell to 58.5% in September, compared to 60.8% in August and 67.0% in June and July. However, a significant number of businesses still cited the broader economic environment as a key negative factor impacting their performance.

ECB to Cut Rates, CPI Reports from UK, Canada, and New Zealand Awaited

ECB is at the forefront this week and is set to deliver a widely expected rate cut. Meanwhile, key inflation data from several major economies, including the UK, Canada, and New Zealand, will offer crucial insights into their central banks’ next moves

ECB is widely expected to lower the deposit rate by 25bps to 3.25% . This marks a significant shift from its previous stance, driven by increasing concerns about economic stagnation and faster-than-expected decline in inflation across the Eurozone. Supporting this expectation, a recent Reuters poll indicated that 70 out of 75 economists surveyed anticipate the 25bps rate cut, a dramatic change from the mere 12% who predicted such a move just a month ago. Looking ahead, 68 of these economists also foresee an additional 25bps reduction, bringing the deposit rate down to 3.00%.

Inflation data will be in sharp focus this week too, with CPI releases from the United Kingdom, Canada, New Zealand, and Japan drawing significant attention.

In the UK, headline inflation is projected to decline to 1.9% in September, below BoE’s 2% target after two months of slight rebounds. However, core CPI is expected to remain relatively high at 3.4%, only a slight decrease from 3.6%. BoE’s MPC is notably divided on the future path of monetary policy. Recently, Governor Andrew Bailey suggested that more aggressive easing could be an option, while Chief Economist Huw Pill urged caution. Consequently, every piece of incoming data will be critical ahead of the November meeting. Additionally, the UK is set to release employment figures and retail sales data.

In Canada, CPI for September might show a slight increase but is expected to remain close to BoC’s target, with core measures holding steady. This situation has led to growing calls for BoC to expedite its policy easing and return interest rates to a neutral setting more swiftly to prevent inflation from falling below target. Should CPI data reveal any downside surprises this week, it could prompt the BoC towards a more substantial 50bps rate cut at its meeting on October 23.

Turning to New Zealand, Q3 CPI is anticipated to show a sharp slowdown from 3.3% to 2.3%, reinforcing RBNZ significant 50bps cut last week. There is speculation that RBNZ may follow up with another 50bps reduction on November 27 to conclude the year, especially since the next meeting isn’t scheduled until mid-February next year. Should this week’s CPI data support the case for further easing, RBNZ may feel compelled to act preemptively once again.

Other important economic indicators to monitor this week include Germany’s ZEW Economic Sentiment Index, Australia’s employment statistics, Japan’s CPI figures, and China’s GDP report.

Here are some highlights for the week:

- Monday: New Zealand BNZ services; China trade balance; Swiss PPI.

- Tuesday: UK employment; Germany ZEW; Eurozone industrial production; Canada CPI, wholesale sales; US Empire State manufacturing.

- Wednesday: New Zealand CPI; UK CPI; Canada housing starts, manufacturing sales; US import prices.

- Thursday: Japan trade balance, tertiary industry index; Australia employment, NAB quarterly business confidence; Eurozone CPI final, trade balance, ECB rate decision; US retail sales, jobless claims, Philly Fed survey, industrial production, business inventories, NAHB housing index.

- Friday: Japan CPI; China GDP, industrial production, retail sales, fixed asset investment; UK retail sales; Eurozone current account; US building permits and housing starts.

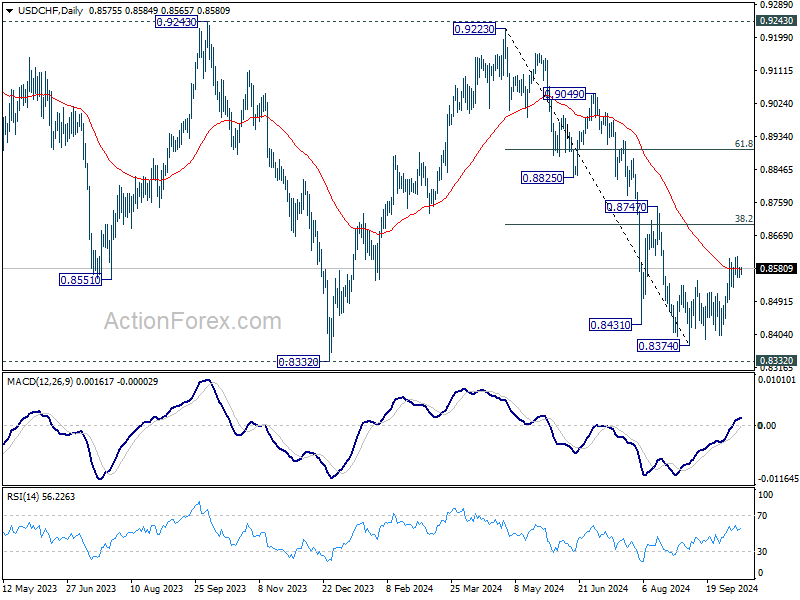

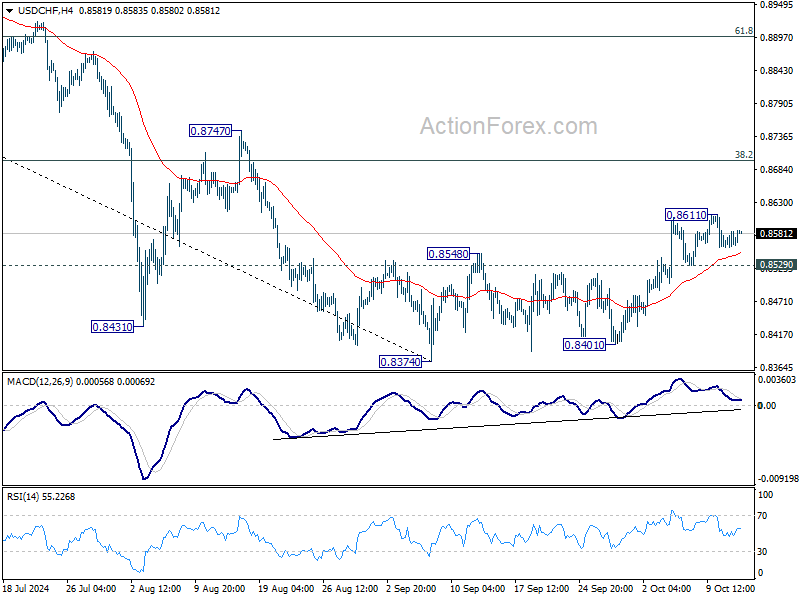

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8557; (P) 0.8573; (R1) 0.8590; More…

USD/CHF trades mildly higher in Asian session but stays below 0.8611 temporary top. Intraday bias remains neutral First. further rally is expected as long as 0.8529 minor support holds. Above 0.8611 will resume the rebound from 0.8374 short term bottom to 38.2% retracement of 0.9223 to 0.8374 at 0.8698. However, firm break of 0.8529 will turn bias back to the downside for retesting 0.8374 low instead.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).