rose at fastest pace in about two years. Shelter prices, known for their stickiness, only rose by 0.2%, matching June’s low print which was in turn the slowest advance since August 2021.){kind=link}

Markets

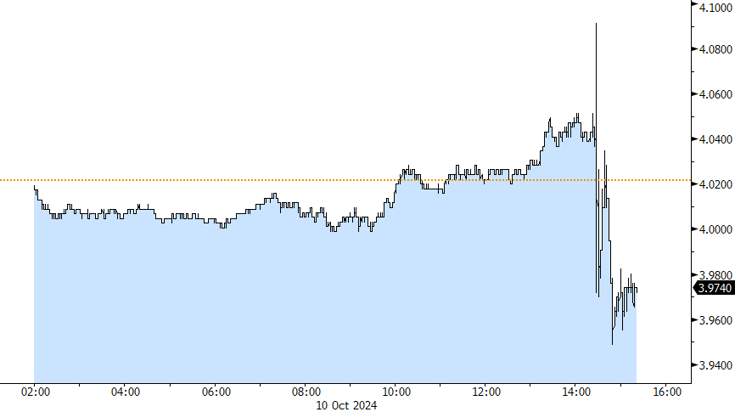

Data dependency = volatility. Today was a textbook example. The US economic agenda featured September CPI figures and the weekly jobless claims. The former came in at the topside of expectations with headline and core coming in at 0.2% and 0.3% m/m respectively, beating the consensus view by 0.1 ppt each. The yearly print as a result eased a little less than hoped-for in headline terms, from 2.5% to 2.4% and unexpectedly accelerated in the underlying gauge to 3.3%. Energy prices were a drag last month, falling almost 2% on a monthly basis, but food prices (0.4%) rose at fastest pace in about two years. Shelter prices, known for their stickiness, only rose by 0.2%, matching June’s low print which was in turn the slowest advance since August 2021. Offsetting this, however, is the quickening in core services ex housing inflation, a metric watched closely by the Fed. With the 0.4% m/m outcome, the annualized 3mMA is nearing 4% again. The broader services inflation gauge stood at 0.4% and 4.7% y/y. Bond yields’ first reaction was to extend previous daily gains with the 2-yr yield spiking to the highest level since mid-August. Enter weekly jobless claims. A big jump from 225k to 258k crushed expectations for a much more modest rise to 230k. States including Florida and North Carolina printed some of the biggest increases, revealing an impact from hurricane Helene. The upcoming readings may be affected similarly (hurricane Milton). The jury’s still out whether it turns out to be a temporary effect but since the Fed is now laser-focused on the labour market it does dictate the market reaction. Front-end yields in the US swapped intraday gains of as much as 7 bps for losses around 4 bps. But that’s nowhere near enough to table the idea of a 50 bps Fed cut in November again though. Current pricing still doesn’t fully discount a 25 bps move, even after today’s repositioning. Swings at the long end of the US curve were much more muted. The likes of the 10-yr trade flat. European/German yields pared earlier gains of 2-3 bps to around 1 bp. The dollar’s intraday volatility eventually ended up in small losses. EUR/USD rebounded from a 1.0910 low to 1.0948 currently. DXY’s trip above 103 ended quickly (102.83).

News & Views

Prices in the Czech Republic declined -0.4% M/M, its statistical office published today. KBC expected a decline of 0.6 M/M. Due to an even sharper decline last year (base effects) the monthly decline still raised the Y/Y measure from 2.2% in August to 2.6% September. The monthly decline in prices was, amongst others, driven by a 20.9% decline in the prices for package holiday. Prices of fuels for personal transport also declined 4.9% M/M. Monthly prices rises mainly came from higher food prices (0.8%) and of costs related to education (+10.6% M/M). Y/Y goods and services prices went up by respectively 1.2% and 5.0%. The September outcome was 0.3% higher than the CNB summer forecast, but in a brief comment today, CNB indicated that core inflation was slightly below the forecast. Still, today’s report suggests that headline inflation might move to/or even above the 3.0% CNB tolerance band by the end of the year, before easing again in early 2025. KBC maintains a scenario of gradual easing (25 bps steps) from 4.25% currently to 3.50% in February 2025. The policy rate then might stay at that ‘new equilibrium level’ for a longer period. The koruna trades little changed near EUR/CZK 25.32.

Hungarian inflation slowed more than expected by -0.1% M/M and 3.0% Y/Y (from 3.4%). Headline inflation returned to the MNB 3.0% target for the first time since January 2021. Analysis of the MNB tells that inflation of tradables declined 0.7% M/M to ease to 1.6% Y/Y. Market services prices increased 0.1% M/M holding the Y/Y-measure at 9.6%. Core inflation measures showed a mixed picture (core ex indirect taxes 4.8% from 4.6%, CPI ex processed food 5.5% from 5.8%, sticky price CPI 5.4% from 5.8%). After a pause in August, the MNB again eased the policy rate by 25 bps (to 6.5%) in September. We expect the MNB will (have to) stick to a cautious approach. Both core and inflation are expected to turn higher again toward the end of the year. As the forint weakened north of EUR/HUF 400, financial stability concerns will again get a bigger weight in the MNB assessment. In this respect deputy Governor Virag earlier this week indicated that chances of a skip at the October 22 meeting have grown. Lingering political tensions with the EU and market concerns on fiscal consolidation also don’t help the forint. The Hungarian currency declined from the EUR/HUF 399 area this morning to 400.6 currently.

Graphs

US 2-yr yield whipsawed on simultaneous release of stronger-than-expected CPI and surge in jobless claims

EUR/CZK: Czech koruna trades unchanged vs opening levels. September CPI won’t alter CNB’s gradual approach

EUR/HUF: below-consensus CPI doesn’t pave the way for further easing with forint again in the defensive

EUR/NOK: Easing Norwegian core inflation to nudge Norges Bank a bit further towards inaugural December cut?