{kind=link}

Dollar continued its broad-based weakness in Asian session, with selling pressure shifting towards European majors. EUR/USD is approaching its August high as the near-term rebound gathers momentum. This decline in the Dollar is partly attributed to weaker-than-expected US consumer confidence data released overnight, which has intensified market expectations of consecutive 50bps rate cuts by Fed in November.

On the European front, speculation about another 25bps rate cut by ECB in October has been tempered by recent comments from policymakers. It appears that ECB officials are still viewing December as a more suitable time for further monetary adjustments, given that more comprehensive economic data will be available by then.

So far this week, Dollar is the worst-performing major currency, followed by Euro and Japanese Yen. Kiwi leads gains, buoyed by positive risk sentiment, followed by Aussie and Loonie. Sterling and Swiss Franc are trading in the middle range, with attention on Swiss Franc ahead of tomorrow’s SNB rate decision.

Meanwhile, risk-on sentiment continues to dominate Hong Kong and China markets, as supported by yesterday’s stimulus announcement by PBoC. Hong Kong HSI is now eyeing an important medium term resistance level at around 20000 psychological level, with 61.8% projection of 14794.16 to 19706.12 from 17127.25 at 19999.87. Decisive break of this level would confirm that it’s already in a medium term up trend and target 100% projection at 21876.24. That, if realized, would be supportive to Aussie and Kiwi.

In Asia, at the time of writing, Nikkei is up 0.13%. Hong Kong HSI is up 2.01%. China Shanghai SSE is up 1.73%. Singapore Strait Times is down -0.64%. Japan 10-year JGB yield is up 0.005 at 0.816. Overnight, DOW rose 0.20%. S&P 500 rose 0.25%. NASDAQ rose 0.56%. 10-year yield fell -0.003 to 3.736.

Australia’s monthly CPI falls to 2.7%, lowest since 2021

Australia’s monthly CPI slowed from 3.5% yoy to 2.7% yoy in August, marking the lowest reading since August 2021. Core inflation measures also eased, with CPI excluding volatile items and holiday travel declining to 3.0% yoy from 3.7% yoy, and the annual trimmed mean falling to 3.4% yoy from 3.8% yoy. Both underlying inflation indicators are now at their lowest levels in two and a half years.

Significant price increases were observed in Housing (+2.6%), Food and non-alcoholic beverages (+3.4%), and Alcohol and tobacco (+6.6%). These gains were “partly offset” by a -1.1% decrease in Transport costs.

Notably, electricity prices plummeted by -17.9% over the 12 months to August—the largest annual fall since the early 1980s—driven by Commonwealth and State Government rebates that led to a -14.6% drop in August following a -6.4% decline in July. Excluding these rebates, electricity prices would have risen 0.1% in August and 0.9% in July.

BoC’s Macklem signals more rate cuts as inflation progress continue

BoC Governor Tiff Macklem, in a speech overnight, suggested that more interest rate cuts are likely, contingent on incoming economic data. He acknowledged, “With the continued progress we’ve seen on inflation, it is reasonable to expect further cuts in our policy rate.”

However, he emphasized that the timing and pace of such cuts would be determined by the assessment of future inflation and broader economic conditions.

Macklem noted that economic growth had picked up in H1, but some recent indicators suggest it may not be as robust as previously anticipated. “We will be closely watching consumer spending, as well as business hiring and investment,” he said.

He also expressed the need to see core inflation ease further. Shelter cost inflation remains elevated but is beginning to decline, and BoC is looking for this trend to continue. “Continued progress on inflation will be crucial to ensure our policy remains effective,” Macklem added.

ECB’s Knot: Likely to continue rate cuts into H1 2025

In an interview on Dutch television overnight, ECB Governing Council member Klaas Knot emphasized that interest rates across Europe are poised for continued gradual reductions. Knot affirmed that as ECB gains confidence in achieving its 2% inflation target, “interest rates will simply keep falling.”

Looking ahead, “I would expect us to continue to gradually reduce interest rates in the coming time, also in the first half of 2025,” Knot added.

However, he cautioned against expectations of a return to the ultra-low rates seen before the pandemic. Instead, he suggested that rates are likely to settle at a “more natural level” within a range starting with a 2.

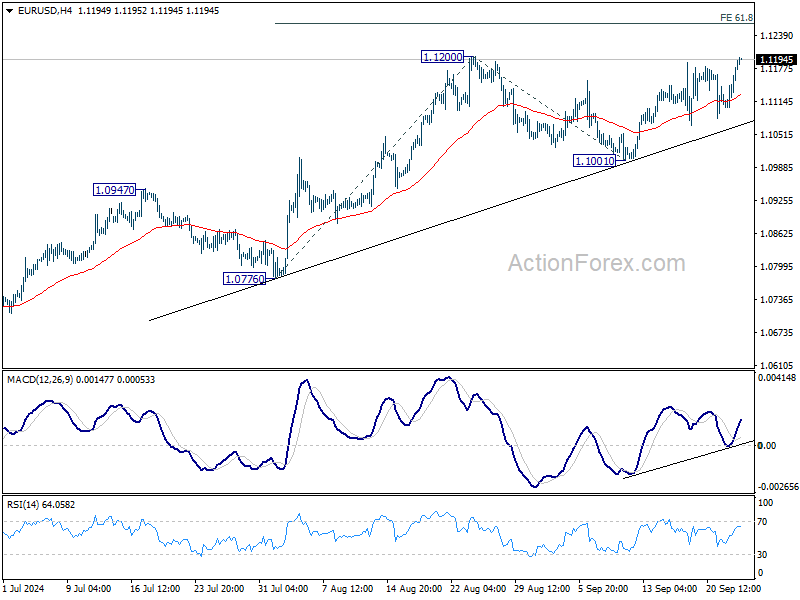

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1128; (P) 1.1155; (R1) 1.1206; More….

Immediate focus is now on 1.1200 resistance as EUR/USD’s rebound from 1.1001 extends today. Break there will resume the rally from 1.0665 to retest 1.1274 high. Firm break there will resume larger up trend. Next near term target will be 100% projection of 1.0776 to 1.1200 from 1.1001 at 1.1425. Rejection by 1.1200 will bring another retreat. But outlook will continue to stay bullish as long as 1.1001 support holds.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 might have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm resumption of whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Aug | 2.70% | 2.70% | 2.80% | 2.70% |

| 01:30 | AUD | Monthly CPI Y/Y Aug | 2.70% | 2.70% | 3.50% | |

| 08:00 | CHF | UBS Economic Expectations Sep | -3.4 | |||

| 14:00 | USD | New Home Sales Aug | 693K | 739K | ||

| 14:30 | USD | Crude Oil Inventories | -1.3M | -1.6M |