. Activity in France is deflating from a temporary summer uptick due to the Olympic games (47.4 from 53.1). Before September, a sharp contraction in EMU manufacturing was compensated for by ongoing growth in services.){kind=link}

Markets

Its going from bad to worse with the EMU economy. According to the Flash PMI, activity contracted in September for the first time since February. The headline composite index slipped from 51 to 48.9 , substantially below the 50.5 expected. Germany fell further in contraction territory (47.2 from 48.4). Activity in France is deflating from a temporary summer uptick due to the Olympic games (47.4 from 53.1). Before September, a sharp contraction in EMU manufacturing was compensated for by ongoing growth in services. Contraction in manufacturing is becoming ever deeper (44.8 from 45.8). Services growth remains positive) except for France (48.3 from 55.0), but also nears a standstill (50.5 from 52.9). According to S&P global, the decline in overall activity comes amid a sustained reduction new orders. New business decreased at the sharpest pace since January. With new orders and volumes of outstanding business falling at sharper rates and business confidence at a ten-month low, companies scaled back workforce numbers for the second month running. Demand weakness resulted in slower inflation of both input costs and output prices

From a market point of view, the key question is what this awful PMI means for a data-dependent ECB. A brief inter-meeting period with few data releases between the September and October decisions and slightly upward revisions to its (core) inflation forecasts (2024 & 25), suggested a high bar to accelerate the pace of rate cuts. After the PMI’s, markets are raising the odds that the ECB will (have to) make a Fed-like move and give more priority to supporting growth. German/EMU yields declined sharply after the release but currently are trading off the intra-day lows. German yields cede between 5.5 bps (2-y) and 1 bp (30-y). EMU money markets see about a 40% chance of an October ECB rate cut. Maybe a bit surprising, EMU equities quite easily reversed a post-PMI dip (Eurostoxx 50 +0.4%). Similar story for the euro. EUR/USD swiftly tumbled from the 1.116 area to test the 1.1085 area, but currently again trades near 1.113. The damage could have been much bigger. Underlying USD weakness clearly still is at work. Sterling in the meantime continues its outperformance on a better PMI (cf infra) , especially against the euro. At 0.8345, EUR/GBP now trades now well below the 0.8383 previous low

US PMI’s mostly are not as influential for US markets as they are for EMU. At the time of finishing this report, the US PMI’s are reported to have held up very well (composite 54.4 from 54.6). In a first reaction, US yields gained modest ground with yields rising between 1.5 bps (2-y) and 3.2 bps (30-y). The dollar still hardly profits.

News & Views

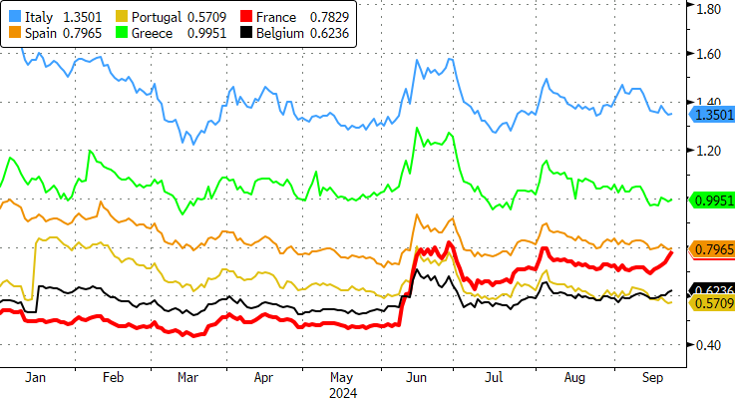

The French spread vs Germany’s 10-yr yield touched the highest level since the June snap election announcement (80 bps). OAT underperformance followed very weak French PMIs compounded with the announcement of a new French cabinet over the weekend. It’s a mixture of conservatives and centrists who haven’t always been on the best terms with each other. In addition, opposition blocs to both the left and the right have threatened to topple the fresh government through a vote of no confidence. This would plunge the country in renewed political uncertainty. The government coalition falls far short of the votes needed to prevent that from happening. The lift-wing NFP party said it’ll call for one at the earliest occasion. That would be October 1, when PM Barnier is due to address the parliament. It still needs the backing of the right-wing to do so, though. The right-wing Front National’s VP said its decision to support a no-confidence bill depends on the budget and Barnier’s approach.

UK PMI’s eased more than expected in September. The composite gauge fell from 53.8 to 52.9 on weaker readings in both manufacturing (51.5 vs 52.2 expected) and services (52.8 vs 53.5). Still, Output in both sectors rose thanks to rising customer demand and improving domestic economic conditions. Employment grew at the weakest pace since June. A marginal increase in services was counterbalanced by renewed job cuts in manufacturing. Cost burdens picked up from a 45-month low on higher container shipping costs and rising salary payments. Prices charged went the other way and rose at the slowest pace since February 2021. Business activity expectations remained upbeat and even picked up from last month, though firms cited lingering autumn budget-related uncertainty.

Graphs

Intra-EMU spreads: France (red) underperforms the region as political uncertainty still prevents budget consolidation.

2-y German yield testing recent low as markets reconsider chances for ECB October rate cut post very weak PMI’s.

EUR/USD holding up rather well despite EMU economy heading to contraction territory.

Cable: Sterling outperforms both euro- and USD weakness.