{kind=link}

After suffering steep selloff yesterday on political uncertainties, Sterling stabilized and recovers mildly today. But focus will set to stay in the UK with CPI featured in the economic calendar. For the moment, GBP/USD and EUR/GBP are still holding in range. Thus, we’re treating the selloff in the Pound as part of a corrective pattern first. Meanwhile, the calendar is getting busy today with Eurozone set to release GDP, industrial production as well as German ZEW economic sentiment. Some volatility could be seen in EUR/GBP. US will also release PPI later today which gives the market a glimpse of the inflation outlook, and as a prelude to Wednesday’s CPI release. The greenback is generally staying in consolidation mode and needs fresh inspiration for a breakout.

Treasury Mnuchin: Trump will not accept corporate tax at more than 20%

In the US, Treasury Secretary Steven Mnuchin warned that President Donald Trump’s administration will not accept nor support any tax plan with a corporate tax rate of more than 20%. This is in regards to the negotiations between the House and the Senate for reconciliations of their passed bills. The House version of the tax bill will comes to floor later this week. Debate will begin on Thursday. Chairman of the tax-writing Ways and Means Committee Kevin Brady expressed his confidence for passage. Senate Finance Committee started debating their tax bill yesterday. And there could be significant revisions to be announced this week.

Brexit Davis: Parliament will have final vote on Brexit deal

Brexit Secretary David Davis announced in the House of Commons that he will introduce legislation for the parliament to vote on the final Brexit agreement with EU. He noted that "it is clear that we need to take further steps to provide clarity and certainty both in the negotiations and at home regarding the implementation of any agreement into United Kingdom law." And he emphasized that "this agreement will only hold if parliament approves it." The "principal policy aim" will be read by October 2018, which should give enough time for debate and vote before the Brexit date on March 29, 2019. However, under the move, the Parliament will have no say in case of a no-deal, not be able to reverse the decision, and not even be able to reopen talks.

ECB Constancio: Stimulus program "highly successful"

ECB Vice President Vitor Constancio hailed the central bank’s massive monetary stimulus as "highly successful" in driving recovery. He pointed out that "the euro-area economy is experiencing a broad-based, robust and resilient recovery." Nonetheless, he maintained a cautious tone and emphasized "we know that this process still relies significantly on our monetary policy support. It is not yet self-sustained and therefore we must be patient and persistent." Meanwhile he also defended the monetary policy measures and emphasized they "were not an ‘experiment’" but " in line with the policies previously adopted by other major central banks." Also, despite concerns "about possible collateral consequences of our policy, such concerns have however not materialized in real facts and we can now underline the appropriateness of our monetary policy stance."

BoJ Kuroda to persist with "powerful monetary easing"

BoJ Governor Haruhiko Kuroda reiterated his pledge to persist with "powerful monetary easing". He said in a speech at the University of Zurich in Switzerland that this powerful monetary easing "has been producing remarkable effects." And Japan is "no longer in deflation". He noted "going forward, with the output gap improving steadily, firms’ stance is likely to gradually shift toward raising wages and prices." And he’s optimistic that "if further price rises come to be widespread, inflation expectations are likely to rise steadily." Therefore, he emphasized that "the Bank will continue to persist with powerful monetary easing to ensure that such positive developments are not cut short."

NAB: Better than expected performance for the economy ahead

In Australia, NAB business conditions jumped 7 points to 21 in October, hitting the highest level the series began back in 1997. It’s also nearly four times the historical average. Business confidence, on the other hand, was unchanged at 8. NAB chief economist Alan Oster noted that "this is an extremely strong result and of itself would suggest a better than expected performance for the economy." However, he also warned that "it is unclear just how long conditions can remain at these record levels given that the result was driven by a surprise jump in manufacturing, while some of the leading indicators such as forward orders – which have been giving a more accurate read on the strength of the economy – have actually softened a little in recent months."

China data disappoint

From China, retail sales rose 10.0% yoy in October, below expectation of 10.5% and slowed from prior 10.3% yoy. Fixed asset investment rose 7.3% yoy, inline with expectation but slowed from prior 7.5% yoy. Industrial production rose 6.2% yoy, meeting consensus but also slowed from prior 6.6 yoy.

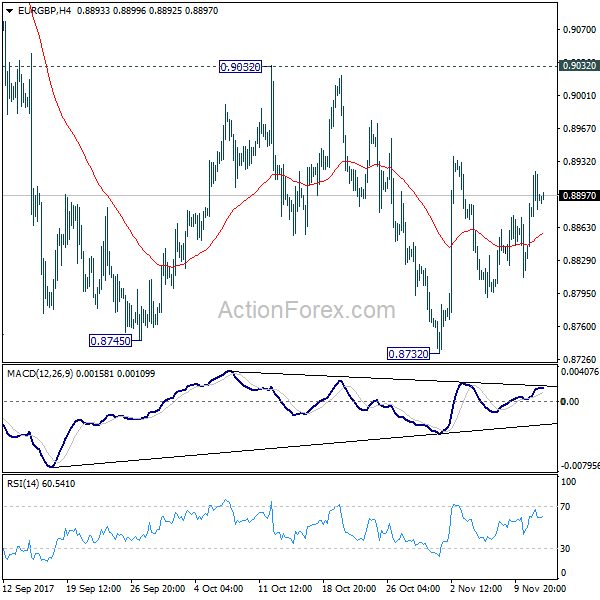

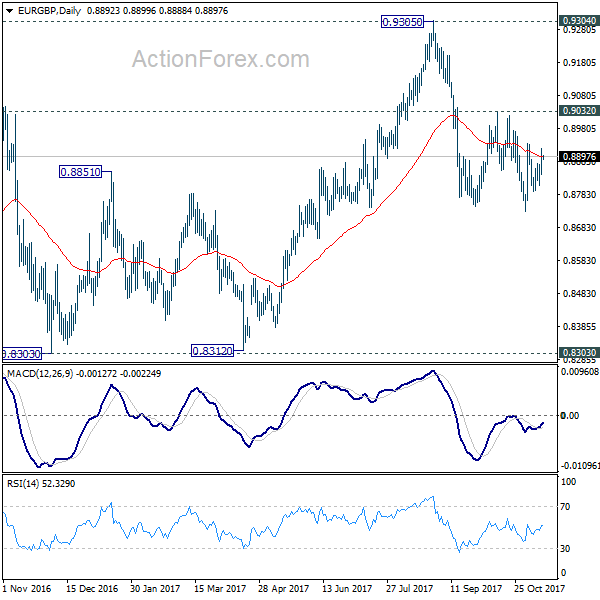

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8792; (P) 0.8840; (R1) 0.8889; More…

EUR/GBP is still bounded in range of 08732/9032 and intraday bias remains neutral. With 0.9032 resistance intact, deeper decline is mildly in favor in the cross. Break of 0.8732 will resume the decline from 0.9305 and target 0.8303 key support level. However, on the upside, decisive break of 0.9032 will confirm completion of the decline from 0.9305. In such case, intraday bias will be turned back to the upside for retesting 0.9305 key resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we’d expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | AUD | NAB Business Confidence Oct | 8 | 7 | 8 | |

| 2:00 | CNY | Retail Sales Y/Y Oct | 10.00% | 10.50% | 10.30% | |

| 2:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Oct | 7.30% | 7.30% | 7.50% | |

| 2:00 | CNY | Industrial Production Y/Y Oct | 6.20% | 6.20% | 6.60% | |

| 7:00 | EUR | German GDP Q/Q Q3 P | 0.60% | 0.60% | ||

| 7:00 | EUR | German CPI M/M Oct F | 0.00% | 0.00% | ||

| 7:00 | EUR | German CPI Y/Y Oct F | 1.60% | 1.60% | ||

| 8:15 | CHF | Producer & Import Prices M/M Oct | 0.50% | |||

| 8:15 | CHF | Producer & Import Prices Y/Y Oct | 0.80% | |||

| 9:00 | EUR | Italian GDP Q/Q Q3 P | 0.50% | 0.40% | ||

| 9:30 | GBP | CPI M/M Oct | 0.20% | 0.30% | ||

| 9:30 | GBP | CPI Y/Y Oct | 3.10% | 3.00% | ||

| 9:30 | GBP | Core CPI Y/Y Oct | 2.80% | 2.70% | ||

| 9:30 | GBP | RPI M/M Oct | 0.20% | 0.10% | ||

| 9:30 | GBP | RPI Y/Y Oct | 4.10% | 3.90% | ||

| 9:30 | GBP | PPI Input M/M Oct | 0.80% | 0.40% | ||

| 9:30 | GBP | PPI Input Y/Y Oct | 4.70% | 8.40% | ||

| 9:30 | GBP | PPI Output M/M Oct | 0.30% | 0.20% | ||

| 9:30 | GBP | PPI Output Y/Y Oct | 2.90% | 3.30% | ||

| 9:30 | GBP | PPI Output Core M/M Oct | 0.20% | 0.00% | ||

| 9:30 | GBP | PPI Output Core Y/Y Oct | 2.20% | 2.50% | ||

| 9:30 | GBP | House Price Index Y/Y Sep | 5.20% | 5.00% | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Sep | -0.60% | 1.40% | ||

| 10:00 | EUR | German ZEW Economic Sentiment Nov | 19.5 | 17.6 | ||

| 10:00 | EUR | German ZEW Current Situation Nov | 88 | 87 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Nov | 29.3 | 26.7 | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | 0.60% | 0.60% | ||

| 13:30 | USD | PPI M/M Oct | 0.10% | 0.40% | ||

| 13:30 | USD | PPI Y/Y Oct | 2.30% | 2.60% | ||

| 13:30 | USD | PPI Core M/M Oct | 0.20% | 0.40% | ||

| 13:30 | USD | PPI Core Y/Y Oct | 2.20% | 2.20% |