- The CME FedWatch tool has suggested a total of 250 bps Fed funds rate cuts through September next year, to bring the Fed funds rate to 2.75%-3.00%.

- An upbeat BoJ’s monetary policy statement next Friday may trigger another round of JPY strength.

- Watch the key levels of 83.80 and 91.60 on the NZD/JPY.

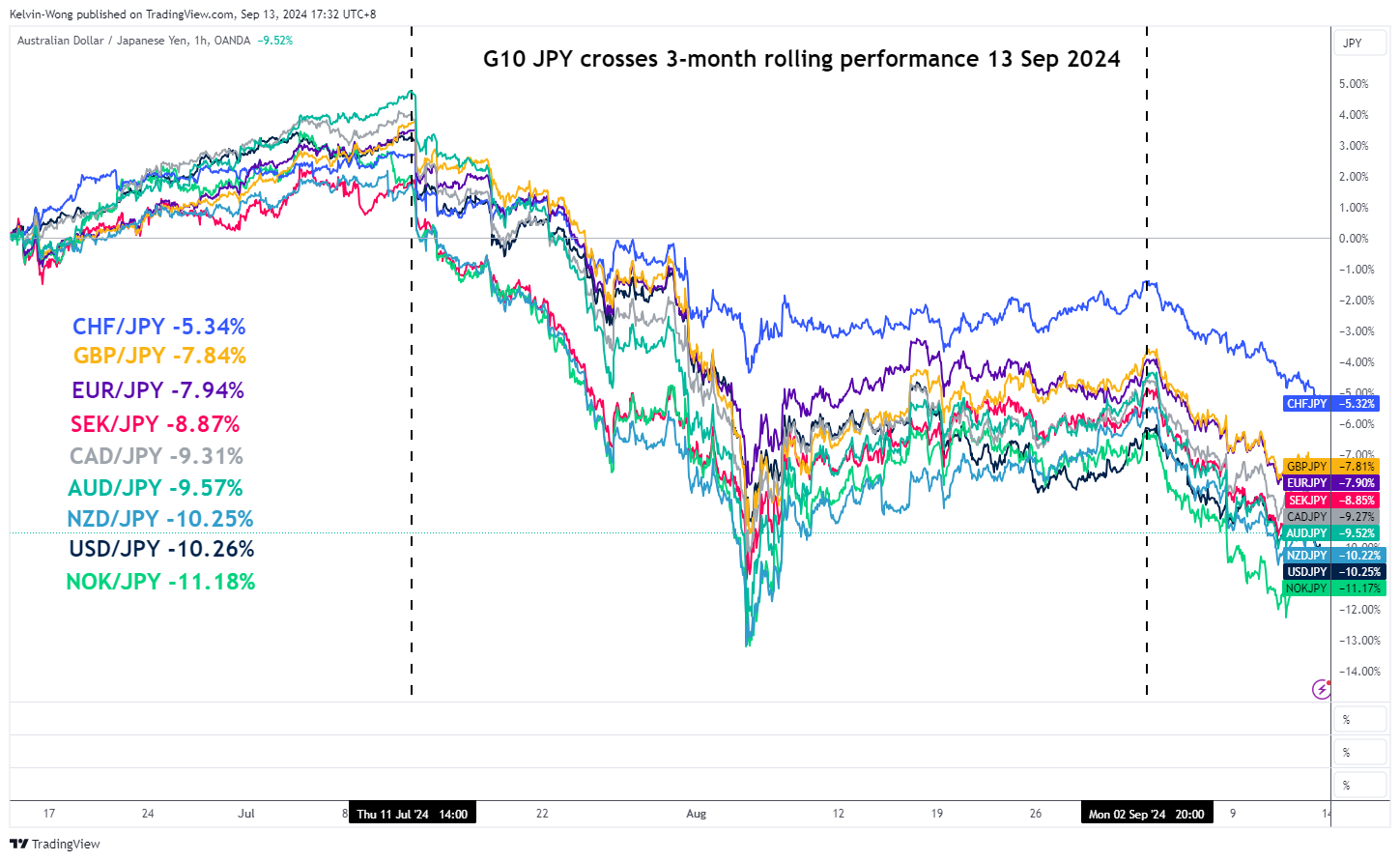

Since our last publication, an equal-weighted basket of Japanese yen crosses Index that consists of the G-10 currencies (AUD, NZD, CAD, SEK, NOK, EUR, GBP, CHF, and USD) continued to tumble and recorded a week-to-date loss of -1.24% at this time of the writing. Also, it is just a whisker away of 1.5% from its key 5 August 2024 swing low.

NZD/JPY is the third worst-performing JPY cross pair

Fig 1: 3-month rolling performances of G-10 JPY crosses as of 13 Sep 2024 (Source: TradingView, click to enlarge chart)

The current leg of the Japanese yen crosses’ weakness has taken form since 2 September. Based on a three-month rolling performance basis as of 13 September, the NZD/JPY is ranked the third worst performer with a loss of 10.25% before USD/JPY (-10.26%), and NOK/JPY (-11.18%) (see Fig 1).

Key pivotal week ahead for global financial markets

Next Wednesday, 18 September, the US Federal Reserve is likely to kickstart its interest rate cut cycle after a pause of close to a year, and the expectations of 25 basis points (bps) cut on Fed funds rate to bring it lower to 5.00%-5.25% has already been fully priced in based on data from CME FedWatch tool.

Also, the aggregated probabilities calculation from the CME FedWatch tool suggests a likely 50 bps cut each for the next FOMC meeting on 11 November and 12 December to bring the Fed funds rate to 4.00%-4.25% before 2024 ends (a total of 125 bps cut).

In the upcoming year of 2025, another series of potential Fed funds rate cuts are expected to amount to 125 bps from January to September and the Fed funds rate may end at 2.75%-3.00% on the 17 September 2025 FOMC meeting; close to the 2.5% median long run projection pencilled in the previous “dot-plot” released on the June FOMC meeting.

The current pricing odds obtained from the CME FedWatch tool suggest that the 30-day Fed funds futures market is highlighting an increased risk of a recessionary environment in the US, and the Fed may be forced to respond with deeper cuts down the road.

Hence, Fed Chair Powell’s press conference and the latest “dot-plot” of Fed officials’ economic projections on growth, inflation, and Fed funds rate are likely to be scrutinized to decipher the Fed’s current view on the state of the US labour market and other economic growth-related variables such as consumer spending.

Any hints that indirectly point to softness in the US labour market may see another round of sell-off in the US dollar. In contrast, a stamp of “confidence” on the state of the US economy from Fed Chair Powell is likely to trigger some form of short covering on the US dollar where JPY weakness may resurface in the short term.

BoJ is on the horizon as well

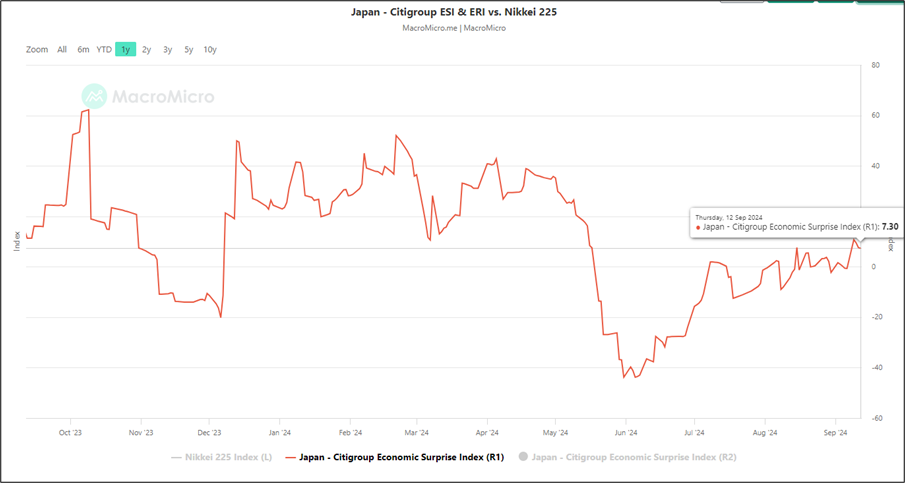

Fig 2: Japan Citigroup Economic Surprise Index of 12 Sep 2024 (Source: MacroMicro, click to enlarge chart)

The Bank of Japan (BoJ) will set its monetary policy decision next Friday, 20 September after the release of the national-wide Japan inflation rate for August on the same day.

Japan’s core inflation rate (excluding fresh food) is expected to inch higher for the fourth consecutive month to 2.8% y/y in August from 2.7% in July.

Also, recent key economic data from Japan has improved (beat expectations on the average) in the past two weeks where the Citigroup Economic Surprise Index has jumped to 7.30 as of 12 September from -2.30 on 30 August, and it is on a steady path of uptrend since Jun 2024 low of -43.80 (see Fig 2).

The consensus forecast is no rate hike by BoJ next Friday but in its monetary policy statement, BoJ may take the opportunity to sound more upbeat on Japan’s economic growth prospects and a firmer inflationary trend in Japan and set the stage for another rate hike in either October or December to bring the overnight policy interest rate to 0.50%.

If such hawkish guidance from the BoJ materializes, the JPY may see another leg of strength which in turn led to more potential weakness in the JPY crosses.

Technical conditions in the NZD/JPY have deteriorated significantly

{kind=link}

Fig 3: NZD/JPY medium-term & major trends as of 13 Sep 2024 (Source: TradingView, click to enlarge chart)

The long-term secular uptrend of the NZD/JPY has been damaged as price actions have retested and traded below the former long-term ascending trendline from the 19 March 2020 pandemic low and the 200-day moving average on 2 September 2024.

The daily RSI momentum indicator has continued to display a bearish momentum reading coupled with the 2-year yield spread of the New Zealand Government Bond and the Japanese Government Bond continued to slip to a new low at 3.5%, below the 5 August print of 3.84% which suggests the attractiveness to use the Japanese yen as a funding currency to invest in New Zealand Government Bonds have been reduced (see Fig 3).

These observations suggest the NZD/JPY may be undergoing a multi-month medium-term downtrend phase. A break below the 83.80 key intermediate support exposes the next medium-term support at 81.00 in the first step.

However, a clearance above 91.60 key medium-term pivotal resistance invalidates the bearish scenario for the next medium-term resistance to come in at 95.40.