{kind=link}

U.S. Highlights

- Inflation and the labor market are cooling off, but the economy has not yet hit a wall. Despite what markets may be fearing.

- The ISM services survey showed broad based improvements in July, while falling longer term interest rates are easing financial conditions.

- Next week’s inflation report and the Jackson Hole summit in a couple of weeks are two big events to keep an eye on.

Canadian Highlights

- Canada’s labour market continues to bend, but not break. A slight decline in both employment and labour force growth has kept the unemployment rate steady.

- We have shifted our expectations for the path of interest rates, where we expect Bank of Canada to deliver three quarter-point cuts over the remainder of 2024.

- Trade data released this week is firming up expectations that economic growth may overshoot the Bank of Canada’s estimates in the second quarter, while also providing a strong hand off into the third quarter.

U.S. – Bumps in the Road

After last Friday’s disappointing payrolls report sent equities tumbling and bonds flying, markets have taken a bit of a breather this week. The U.S. 10-year treasury yield is back to 3.9%, within basis points of where it was last Thursday, while equities have retraced roughly half of their losses since Friday – although they are still well off their mid-July highs

The payrolls data set off alarm bells and traders piled into bets of impending rate cuts and a steep slowdown in economic activity. Fed funds futures are pricing 100 basis points of rate cuts from the Fed through the end of 2024. Importantly, with only three meetings to go, this suggests a 50-basis point cut could come as early as September.

We think this is a tad overdone. To be sure, rate relief is on the way, however our expectation is that the Fed will deliver three more cuts through December. The difference is slight but reflects the fact that we still see an economy that’s gradually gearing down, rather than one where the bottom is falling out.

For instance, take last week’s jobs report. Job growth slowed sharply to 114k jobs from 179k the month prior, with the services sector kicking its smallest addition of the post-pandemic recovery. On the face of it, the second consecutive month of decelerating job growth reflects waning momentum. However, job growth needed to cool to tame inflation and from this lens, the average of 170k jobs gained over the past three months, combined with a cooling in inflation, is a pace the Fed would be happy to accept.

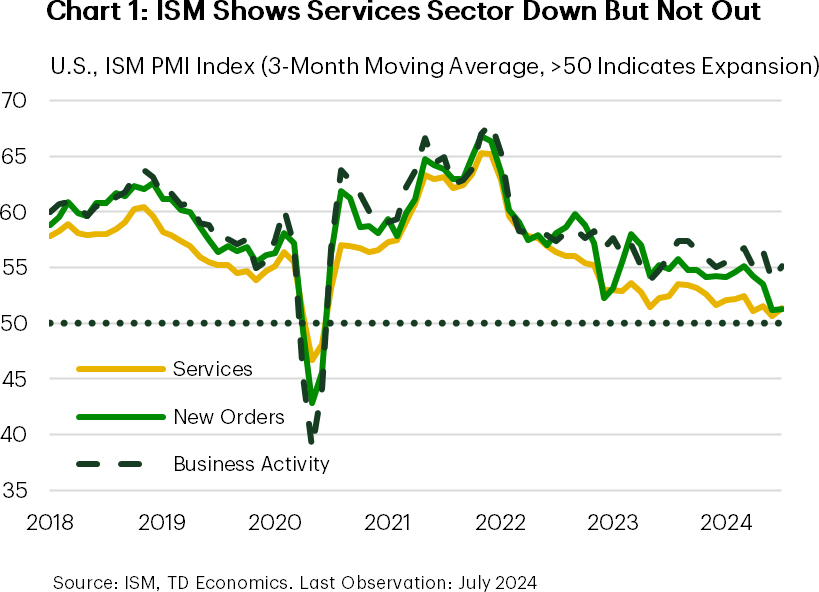

Beyond the labor market, there are signs that economic activity is holding up. This week the ISM services index surprised to the upside, showing the sector regained some momentum to continue expanding. The details of the report were solid with new orders, overall activity and even employment all showing gains (Chart 1).

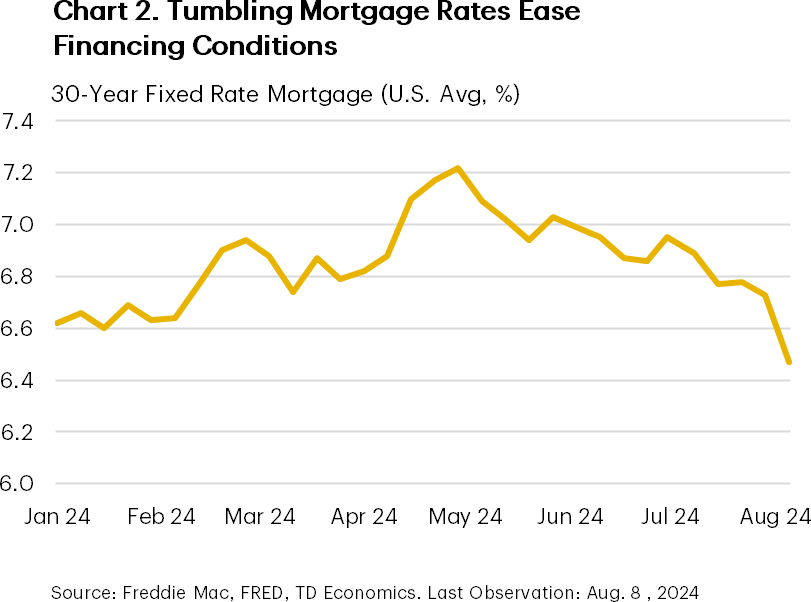

Moreover, falling bond yields are helping ease financial conditions. Thirty-year mortgage rates are down below 6.5%, from 6.9% a month ago (Chart 2). Data from the National Association of Realtors showed June’s pending home sales up nearly 5% month-on-month (m/m), and with a further drawdown in financing costs in July, further recovery in actual sales could be in the offing.

These indicators suggest an economy that continues to mosey along, slower than before, but not yet hitting a wall. And remember, the Fed remains data dependent, so for a sense of how the Fed will respond in September, two upcoming events will be in focus. First up, next week’s release of July’s Consumer Price Index (CPI). We are looking for a firming in core CPI (ex. food and energy) to 0.2% month-on-month. While this implies an annual figure of 3.2%, it would sink the three- and six-month percent changes in core CPI to roughly 1.6% and 2.9% annualized, respectively, comfortably extending the cooling in price gains.

The update on inflation then lays the groundwork for the next big event, the Fed’s Jackson Hole Economic Symposium on August 22-24th. Chairman Powell is slated to speak, so markets will be closely parsing his statements for any insights into the Fed’s read of recent events.

Canada – Keep Calm, Carry On

Canadian markets spent the holiday-shortened week digesting the rapid shift in market sentiment stemming from growth worries south of the border. Recent events in the U.S. and Japan have created volatile market conditions that have spilt over to Canadian markets. Yields whipsawed, with front-end yields rising 15 basis points, partially reversing the 30 bps rally the week prior. The Canadian dollar also caught a bid, up just over a tenth of a cent to 0.728/USD. Despite the external noise, we’d argue the economic outlook for Canada is stable and there isn’t a need to ring the alarm bells just yet.

With a soft U.S. payrolls print last week spurring knee-jerk reactions, Canada’s job market updates were being watched with an even closer eye. Like our southern counterparts, Canada disappointed against expectations, with virtually no job growth recorded in July. But unlike the past several months, labour force growth pulled back which helped keep the unemployment rate steady at 6.4%.Meanwhile, wages as measured by the Labour Force Survey are still growing at 5.0%, which will continue to be on the Bank of Canada’s (BoC) radar (Chart 1). The labour market has no doubt lost steam, but it is holding up relatively well and is evolving roughly in line with what we’d expect from past economic cycles.

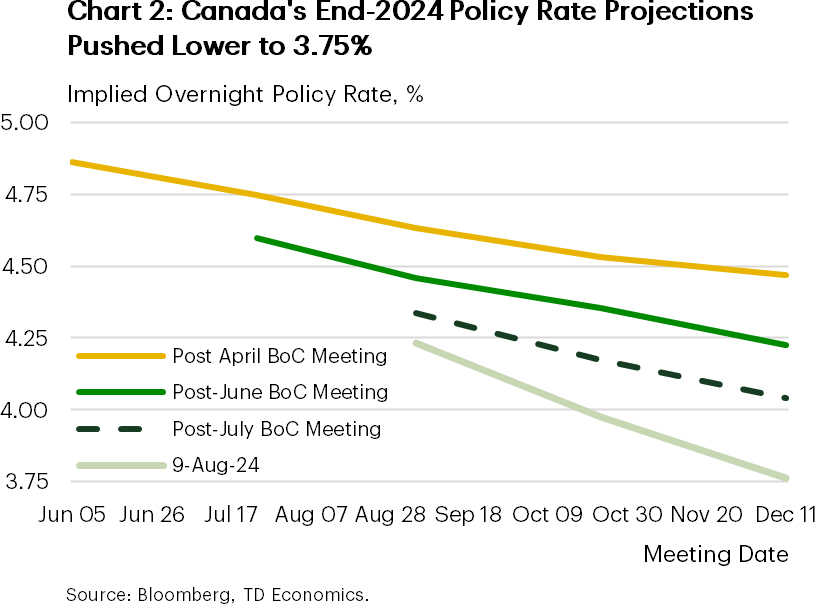

The Bank of Canada will use the labour data as a marker in their next policy decision. The Bank has firmly entered their rate easing cycle and so the question becomes how the path for policy rates looks over the rest of the year. Governor Macklem’s dovish tilt at last month’s meeting had markets re-jigging their rate cut expectations for the remaining three announcements this year, to now see Canada’s policy rate at 3.75% at year-end (Chart 2). This aligns with our thinking as it keeps interest rates on a slowly declining path and balances the objectives of supporting growth without reigniting inflation.

The BoC’s Summary of Deliberations also released this week reiterated an important shift in the BoC’s thinking from last meeting. New in their messaging was the emphasis on the downside risks to inflation via excess supply and how it has taken on an increased weight in monetary policy discussions. This is an important shift in sentiment, as it’s indicative of a central bank concerned that the still high level of the policy rate may be exerting too much slowing in the economy.

Economic growth in Canada’s economy is by no means advancing at breakneck speed, but we don’t foresee a deterioration–or a recession–on the horizon. Domestically, the Canadian consumer bounced back in the first quarter of this year with contributions from spending expected to remain in coming quarters. Further, Canada’s trade picture is firming up as the recently operational Trans Mountain Pipeline expansion boosts energy exports, a theme we expect to persist of the coming months. At this stage, the BoC has enough confidence to gradually deliver rate relief to the economy with a soft-landing scenario still being the likely outcome.