, bolstering former President Trump’s position.){kind=link}

- This week, markets were influenced by trade war fears, US political developments, and a global cyber outage.

- In Asia, the Japanese yen weakened, and Chinese authorities remained silent on economic goals despite weak data.

- Next week, US PCE and GDP data, along with Euro Area and UK PMI data, and potential Chinese economic measures will be key drivers of market volatility.

- The Nasdaq 100’s weekly chart shows a potential evening star candlestick pattern, hinting at further downside.

Week in Review: Trade War Fears and Softening US Data

The week is concluding on an intriguing note, with markets grappling with several issues. Early in the week, news that the US was considering additional sanctions on chip makers doing business with China reignited trade war fears. Meanwhile, the US Presidential election gained momentum with the Republican National Convention (RNC), bolstering former President Trump’s position.

Positive earnings reports from chipmakers were dampened by trade war concerns and weakening US data. Additionally, a global cyber outage on Friday disrupted banks, airports, and many companies. The outage, apparently caused by an update to a product from CrowdStrike, the cybersecurity firm, impacted customers using Windows operating systems.

The outage also affected trading, which was evident during the early hours of the UK session as liquidity seemed thin. However, markets picked up as the US session began, experiencing significant volatility. Gold saw an aggressive selloff due to a strengthening US dollar and rising US yields.

*The chart shows the drop off in volatility during the market outage in the early hours of Friday.

CBOE Volatility Index – Daily Chart

Source: LSEG

In Asia, the Japanese yen weakened further as authorities failed to confirm whether FX intervention occurred this week, benefiting the US dollar. Market participants were also frustrated by the lack of clarity from Chinese authorities after the plenum concluded on Thursday. Despite weak data released on Monday, officials remained tight-lipped about the steps to achieve economic goals.

US indices faced challenges despite some positive earnings updates. At the time of writing, both the S&P 500 and Nasdaq 100 were attempting a recovery but were still on track to end the week in the red. The rotation out of mega-cap tech stocks continued, particularly affecting the tech-heavy Nasdaq, which was down 3.1% at the time of writing.

The Week Ahead: US Inflation, GDP and Company Earnings to Drive Volatility

US

Looking ahead to next week, there is a lot happening globally which could have an impact on financial markets. Market participants will no doubt be hoping for a soft US PCE print and signs of strong growth from the GDP number. The combination should keep current rate cut expectations in place with any surprises likely to stoke some short term volatility.

The core PCE deflator is expected to increase by 0.2% month-on-month, although there’s a chance it could be lower. The core CPI recently rose by just 0.1% month-on-month, but some elements of the PPI that feed into the PCE deflator, like portfolio fees and transport costs, support the 0.2% estimate. Even with this increase, it would align with the annual rate needed to achieve 2% inflation over time, which should maintain expectations for interest rate cuts.

Europe + UK

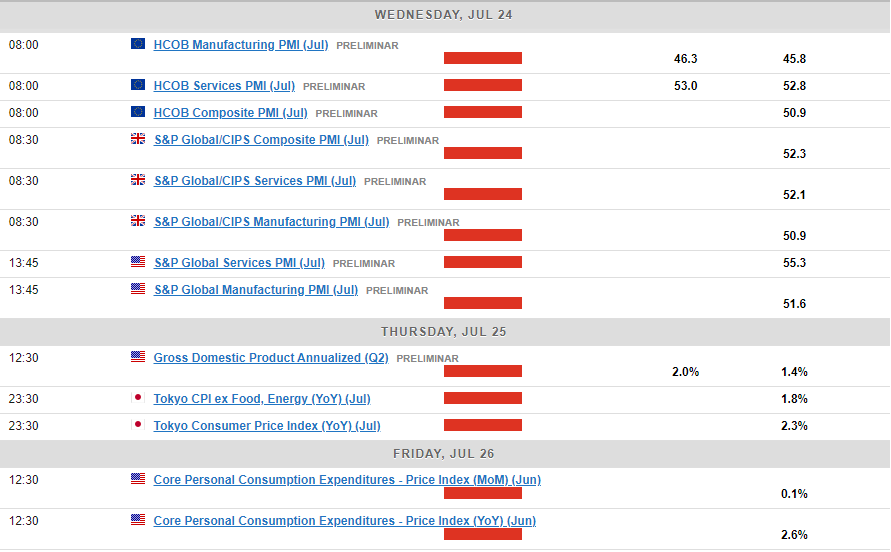

The Euro Area and the UK will both release the HCOB and S&P Global PMI data. The manufacturing and services numbers will give us further insights into the performance of the two economies. The Euro Area and UK composite PMI hit a three-month low in June with market participants keeping an eye on whether this was a once-off or the start of a broader slowdown.

Asian Markets

The People’s Bank of China is set to announce the 1-year and 5-year loan prime rates on Monday, with expectations that the rates will stay unchanged following no adjustments to the MLF this month. No significant data releases are anticipated from China next week.

Japan will have a quiet week, but following recent volatility, it may be worthwhile to pay attention to any further comments or signs of FX intervention. This may prove difficult given the authorities refusal to confirm either way. There is Tokyo CPI data but it is unlikely to have material impact on the yen given that inflation is not the main concern for the Bank of Japan, unlike its G7 counterparts.

Two additional factors that could influence markets in the coming week are geopolitical tensions in the Middle East following a drone attack on Tel Aviv, Israel, just before the weekend. Any indications of escalating tensions or progress toward a peace agreement could have contrasting effects on market sentiment. Market participants will also be watching for any signs or statements from Chinese authorities regarding potential steps to achieve their economic targets.

Chart of the Week

This week, my chart focus is on the Nasdaq 100. After last week’s selloff, the weekly chart is set to form an evening star candlestick pattern, suggesting more downside ahead. The ascending trendline, which has been in play since late April, might finally be retested. This will likely provoke an intriguing reaction considering all the factors that could impact the Nasdaq and broader markets in the coming week.

Nasdaq 100 Daily Chart – June 28, 2024

Key Levels to Consider:

Support:

- 19000

- 18500

- 18000

Resistance:

- 19650

- 20000

- 20480