{kind=link}

Markets

The ECB kept its key policy rates unchanged today in an unanimous decision. In its policy statement, the central bank repeats that it doesn’t pre-commit to a particular rate path. They follow a meeting-by-meeting and data-dependent approach to determining the appropriate level and duration of restriction. Unlike at the April meeting, there’s no clear hint that a new policy rate cut is granted for the September meeting. The April reference said: “if the Governing Council’s updated assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission were to further increase its confidence that inflation is converging to the target in a sustained manner, it would be appropriate to reduce the current level of monetary policy restriction.” ECB President Lagarde kept her cards close to her chest during the Q&A session with the press as well. The ECB’s key concern is the strengthening of underlying core (and more specifically services) inflation. Also headline inflation is likely to remain above the target well into next year. The question of what the central bank does in September is wide open and will be based on all info they’ll receive in between. Also on this guidance, there seems to have been some kind of unanimity on the board. Recall that the ECB earlier this year announced that they would nonetheless close the gap between the deposit rate and the main refinancing rate from 50 bps currently to 15 bps. The spread between the MRO and the penalty lending rate will stay unchanged at 25 bps. The market reaction to the ECB meeting was muted. Daily changes on the German yield curve range between -1 bp (2-yr) and +2 bps (30-yr). The ECB not committing to the September meeting isn’t seen as skipping the opportunity for now. Money markets stick to their path of quarterly rate cuts in September, December, March and June. The euro trades a tad softer at EUR/USD 1.0919. EUR/GBP changes hands at 0.8410. This morning’s UK labour market data (just like yesterday inflation) don’t rule out one scenario or the other (hold or cut) at the August 1st Bank of England policy meeting. US eco data were mixed with weekly jobless claims rising more than forecast, from 222k to 243k, matching the highest level since August 2023. The Philly Fed business outlook beat consensus, rising from 1.3 to 13.9, the second best level since April 2022. Details showed a huge boost in new orders, shipments and employment with firms being more optimistic on these components six months ahead as well. Firms still have quite some pricing power with prices received accelerating to a YTD high while prices paid slightly decelerated.

News & Views

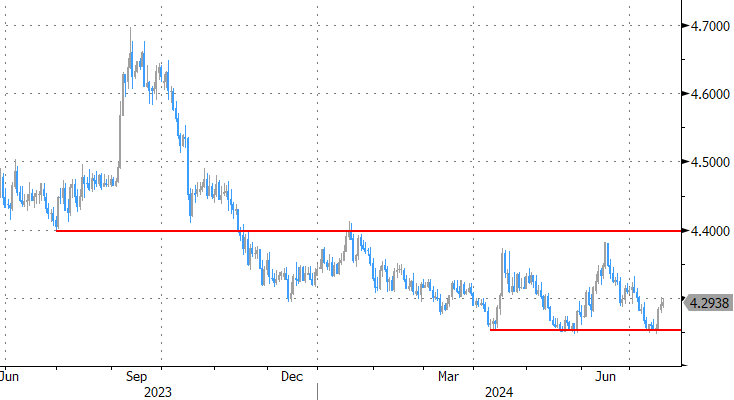

A series of June data published by Statistics Poland painted a mixed picture. Employment in the enterprise sector was unchanged from May but declined 0.4% Y/Y. Despite this consolidation in employment, wages and salaries growth in the enterprise sector remained elevated, increasing 1.8% M/M due to the payment of bonuses, awards and overtime pays. This put gross wages 11% higher compared to the same month last year. In this respect, Statistics Poland mentions that in January 2024, the statutory minimum salary for work was by 17.8% compared previous level set in July 2023, which also affected changes in gross wages and salaries in the enterprise sector. Producer price inflation remains very subdued at 0.1% M/M with prices 6.1% lower Y/Y. Yearly price declines in mining (-5.5%), manufacturing (-5.2%) and electricity and gas (-15.3%) were partially compensated by higher prices in water (2.5%) and construction (6.0%). Industrial production in June rebounded by 3.2% M/M after a 4.5% decline in May, bringing Y/Y growth back in positive territory (0.3%). YTD production growth is also marginally positive (0.1%). The data published today probably won’t change the assessment of the National Bank of Poland to leave its policy rate unchanged at least for this year and probably also going into 2025 as it focuses on the impact of ‘administered price hikes’ and on potential demand pressures due to strong (real) wage growth. After solid gains in June, the zloty (EUR/PLN 4.2975) recently fell prey to profit taking with EUR/PLN rebounding off the 4.25 support area.

The Chinese Communist Party today published a statement at the end of the ‘Third plenum’ meeting. The statement is seen as advocating continuity rather than a big U-turn even as the country tries to implement fundamental changes. Amongst others, the communiqué reiterated policy aims to support new productive forces, to put in place a policy of expanding domestic demand, to prevent and resolve risks in the real estate sector and to reform taxation and the financial system. A more detailed plan is expected to be published in the coming days.

Graphs

DXY (trade-weighted dollar): trying to avoid a drop below neckline of double top formation into this week’s close

USD/CNY: no change of heart at Chinese Communist Party after Third Plenum meeting

EUR/PLN: zloty bounced off strongest levels YTD even as the NBP sticks to forward guidance

Vix volatility index: correction on stock markets just the beginning?