{kind=link}

- ECB meets with near zero chances for a rate cut

- ECB members continue to disagree about the rates outlook

- A dovish shift looks unlikely as the focus rests with the Fed

- Euro showing unexpected strength despite political unrest

ECB meets but all eyes remain on the US

The ECB is preparing for the last meeting before the summer lull with developments elsewhere making President Lagarde’s job even more challenging. While the world is still digesting last week’s weaker US CPI report, the weekend’s attack on US presidential candidate Donald Trump and the collapse of the rumoured Israeli-Hamas truce, ECB members are scheduled to debate on the progress made since the June 6 gathering.

Euro area economy is suffering from political unrest

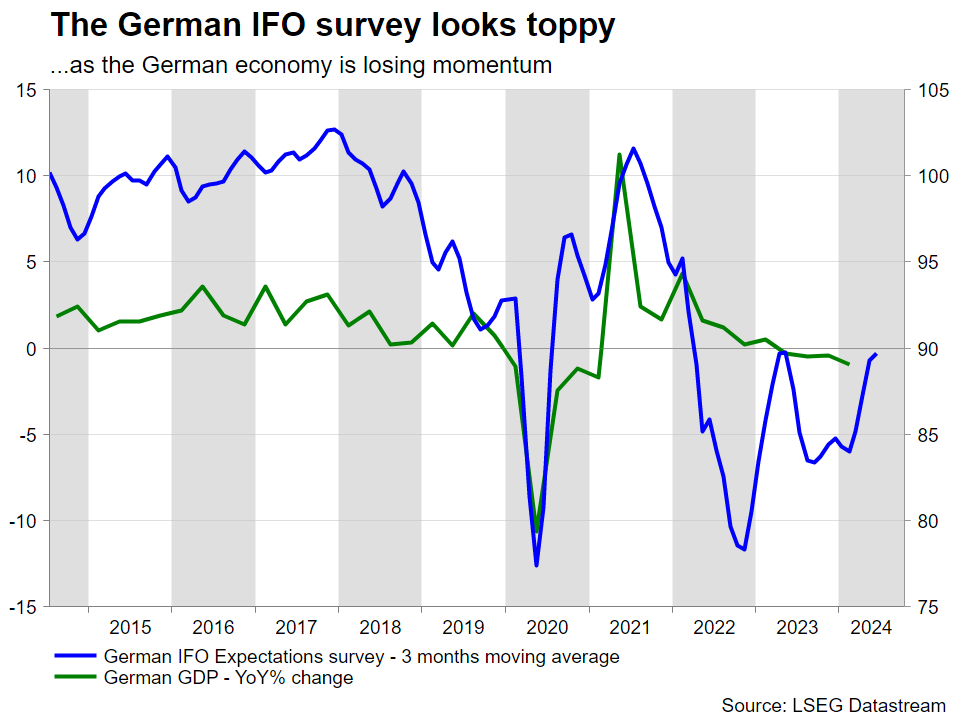

Since early June, the euro area economy appears to be losing momentum. The most recent set of PMI surveys along with the German IFO and ZEW surveys confirm this situation as the economy appears to have been burdened by the latest political developments in the two eurozone heavyweights, Germany and France. The former’s outlook is clouded by the budget shenanigans with the next federal election just 14 months away, while the latter continue the search for a new prime minister, with a caretaker government in place at the moment to ensure the smooth hosting of the Summer Olympics.

Economy is weaker but Lagarde’s main problem is the ECB hawks

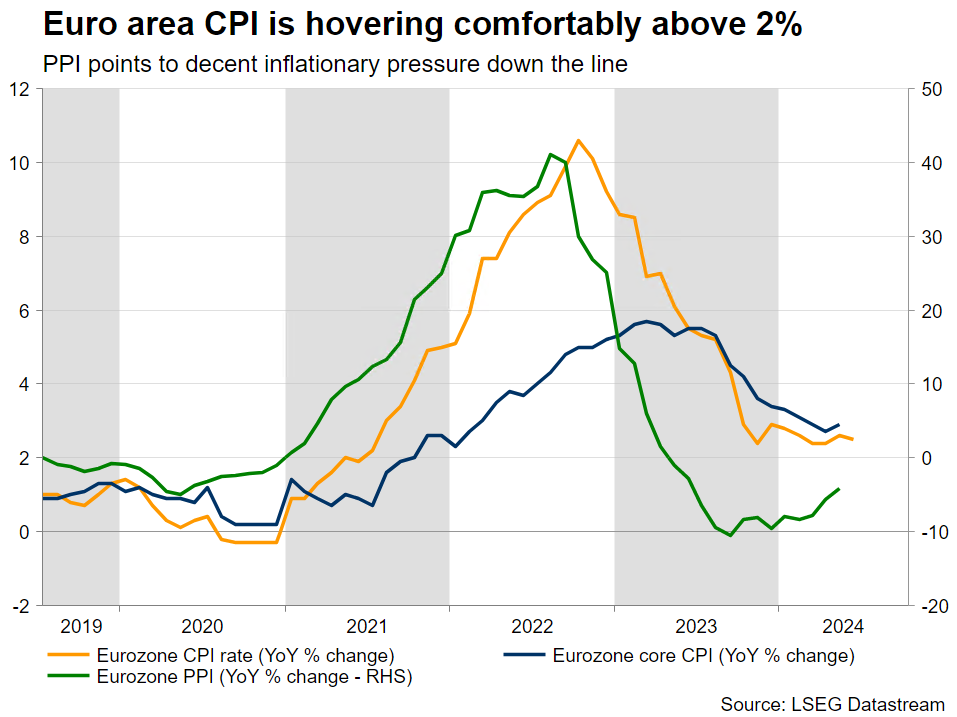

Despite the continued stickiness in inflation, based on the recent data prints, a July rate cut would have been the baseline scenario for this meeting, if the ECB hadn’t rushed into cutting in June. However, President Lagarde was probably too eager to start easing the ECB’s monetary policy stance and she possibly mishandled the June rate decision. The hawks were forced to agree to a 25bps rate cut to save ECB’s face, but they continue to feel betrayed.

The minutes from the June gathering were quite telling about the behind-the-door discussions. As a result, the bar for another rate cut has increased substantially since then. ECB hawks are looking for stronger evidence that inflation will converge to the 2% target by 2025, especially as wage growth remains potent. Until their confidence about the inflation outlook increases considerably, they are unlikely to support any rate moves.

What does this mean for Thursday’s meeting?

The market does not expect a surprise interest rate change on Thursday. It is probably too early for another rate cut, considering the volatile conditions both in the euro area and abroad, with the ECB doves possibly deciding to shift their focus to September. However, with the market pricing in an 80% probability for a September rate cut, could Thursday’s meeting lay the groundwork for such a move?

This looks somewhat unlikely at this stage. At the scheduled press conference, President Lagarde could emphasize the loss of economic momentum, but the stickiness in inflation, especially in the services sector, the strong wage growth and the external environment would probably stop her from making a dovish shift. For the sake of cohesion within the Governing Council, Lagarde might deem it necessary to strike a more balanced approach at the press conference.

More importantly, ECB hawks have been quite clear that they will not tolerate any pre-commitment talk and that the ECB should be truly data dependent. This sounds sensible considering the next ECB meeting will come in two months, on September 12, and by then the Fed’s rate cut intentions would probably be much clearer.

Could the euro benefit from the lack of a dovish shift?

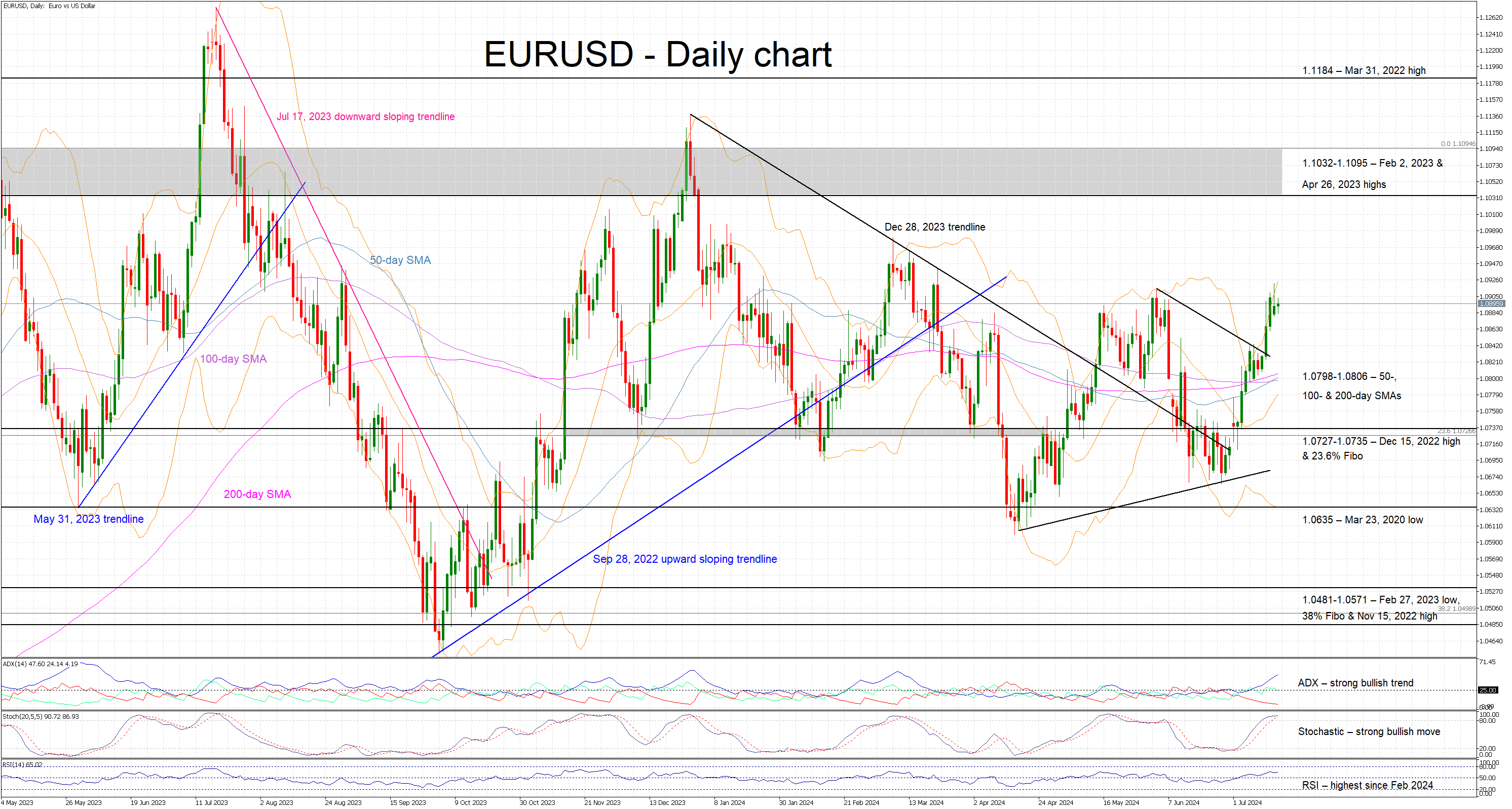

The euro has taken advantage of the widespread US dollar weakness, which has been suffering due to the increased chances for a September rate cut, erasing the recent correction and now testing the early June highs. Technically, the continued convergence of the simple moving averages points to higher volatility going forward, which could be triggered by Thursday’s ECB meeting.

Since the market is fixated on a September ECB rate cut, a dovish shift on Thursday could play into its hand and hence cause euro/dollar to surrender part of its recent gains. Interestingly, a hawkish show on Thursday could largely be ignored as the market will probably see this response as a strategic move from President Lagarde to please the hawks, and not a realistic shift to a more hawkish stance.