{kind=link}

- US inflation data caused a significant selloff in US mega-cap tech stocks and a shift towards riskier areas of the market.

- The ECB interest rate decision is expected to bring no change, but the bank lending survey may shed light on the impact of higher rates on the economy.

- In the UK, inflation data is due on Wednesday, and while headline CPI dipped below 2% in June, it is expected to rise again in the second half of the year.

- In the US, the market will be quiet, with a speech by Fed Chair Powell being the most notable event.

Week in Review: Rate cut bets weigh on tech stocks as US inflation cools

Another week is over and market participants will undoubtedly have plenty of mixed feelings. The highlight of the week came on Thursday when US inflation data data was lower than expected, which has helped boost the confidence of individual FOMC members that inflation is on track to reach the Federal Reserve’s 2% target.

The headline CPI fell by 0.1% month-on-month instead of rising by 0.1% as predicted, while core CPI increased by 0.1% MoM compared to the 0.2% forecast. Additionally, initial jobless claims dropped by 17,000 to 222,000 and continuing claims remained stable. However, the low CPI number is the main focus, causing the 10-year Treasury yield to fall below 4.20% for the first time since late March.

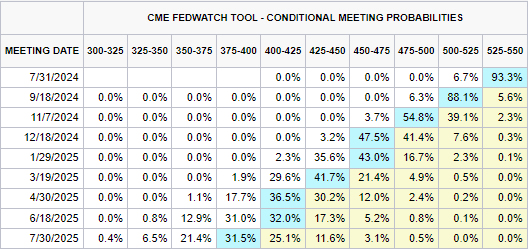

US Interest Rate probabilities have doubled over the past month with market participants now pricing in a 80%+ chance of a rate cut in September and a 60% chance of a cut in November. A stark contrast to two weeks ago and the most recent Fed meeting.

Source: CME Fedwatch Tool

US PPI data released on Friday showed an increase across the board. Market participants hoping for relief were disappointed, as any hopes of a modest US Dollar recovery were dashed by the preliminary Michigan consumer sentiment report. Lower-than-expected consumer sentiment and softer inflation expectations were enough to maintain selling pressure on the US Dollar heading into the weekend.

The most intriguing development following the inflation data release was a significant selloff in US mega-cap tech stocks. The inflation data prompted a notable shift towards riskier areas of the market, with the Russell 2000 emerging as the top performer.

Additionally, another noteworthy development that underscores concerns about the concentration of the S&P 500 in the ‘magnificent 7’ is that the index lost around 0.8% for the day, despite approximately 400 companies ending the day in the green.

The Russell 2000 surged 3.6%, marking its best day in 2024. Homebuilders soared, and banks saw gains ahead of the upcoming earnings season. Given that earnings season is upon us, this could play a crucial role in determining whether the rotation to more smaller stocks will be sustainable or prove to be short-lived.

The Week Ahead – EU, US and ASIA

Europe + UK

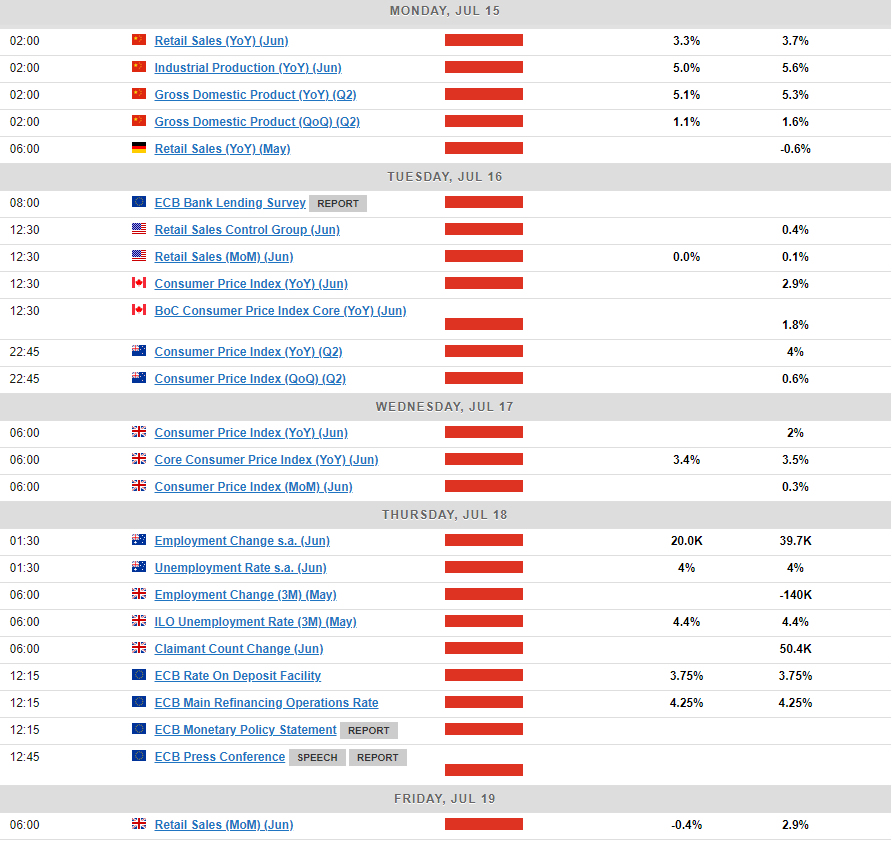

The week ahead brings the European Central Bank (ECB) interest rate decision with market participants expecting no change from the ECB. It would seem that the ECB bank Lending Survey may be more important as it sheds light on the impact higher rates are having on the economy.

In the UK we have inflation data due on Wednesday. Headline CPI dipped slightly below 2% in June, but this is likely the lowest point. Expect it to rise again in the second half of the year, settling between 2-2.5%. Services inflation is a bigger concern for the Bank of England and has been more persistent than expected. We anticipate some minor progress in this area as well. Much of the recent unexpected increase is due to price hikes at the start of the financial year, which the Bank of England believes is likely just noise, not a significant trend.

ASIA PACIFIC

In the Asia Pacific region, the most significant data release next week comes from China on Monday. This includes retail sales, industrial production, and GDP growth data, which will capture the attention of market participants. There is still some uncertainty regarding the Chinese economy, and recent data from the world’s second-largest economy has not alleviated these concerns. Weak data could negatively impact commodity-dependent currencies such as the Australian and New Zealand dollars, as well as the South African Rand.

US

In the US, market participants get a reprieve as we have a quiet week on the calendar. Among the most notable events will be a speech by Fed Chair Powell. It will be interesting to hear what the Fed Chair has to say following the CPI and PPI data and whether the PPI print may weigh on any decisions at the Fed upcoming meetings.

Chart of the Week

The chart I will be focusing on this week is the US Dollar Index (DXY). Following softer inflation data in the US, the DXY has broken through the psychological level of 105.00. The DXY also completed a break of the ascending trendline and both the 100 and 200-day MAs.

Price is resting at the 104.00 support handle heading into next week. I think the big question on the lips of market participants is whether this move will be sustainable. The lack of data next week from the US means the speech by Fed Chair Powell could be key in determining the US Dollar Indexes next move.

Continued weakness in the DXY will likely benefit US Dollar denominated currency pairs as well as commodities like Gold and Silver.

DXY Daily Chart – July 12, 2024

Source:TradingView.Com (click to enlarge)