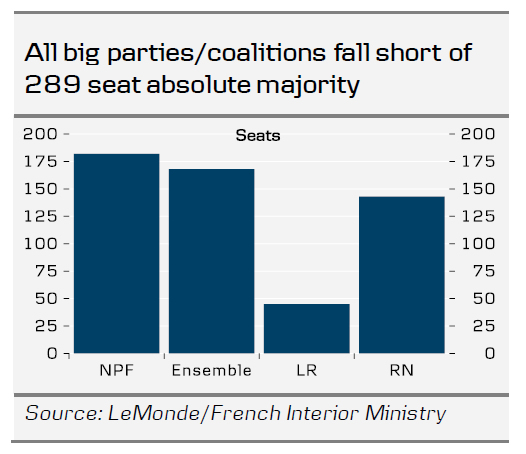

became the largest party, securing 182 seats. Macron's centrist "Ensemble" alliance finished second with 168 seats. The far-right National Rally (RN) has unexpectedly taken third place, garnering 143 seats. A party or coalition needs 289 seats for an absolute majority.){kind=link}

No party secured an absolute majority in the French National Assembly, leaving it highly fractured after the election. The left-wing New Popular Front (NPF) became the largest party, securing 182 seats. Macron’s centrist “Ensemble” alliance finished second with 168 seats. The far-right National Rally (RN) has unexpectedly taken third place, garnering 143 seats. A party or coalition needs 289 seats for an absolute majority.

Uncertainty about what the new government will look like is high, and there is no obvious majority government to be formed. However, if a majority government is somehow formed, it likely must include Macron’s centrist Ensemble alliance to get above the 289-seat threshold. We must now wait some days or weeks before we know more of what the new government will look like, and it could take even longer before an actual government is formed. In all scenarios the new government will be fragile, as it will consist of different parties with vastly different political views or be a minority government. There is also the risk that no government can be formed, and a technocratic government could be installed for the first time in French history. Uncertainty in French politics is set to persist even after a government is formed as there is a higher than usual risk of the government breaking given the fragmentated results of the election.

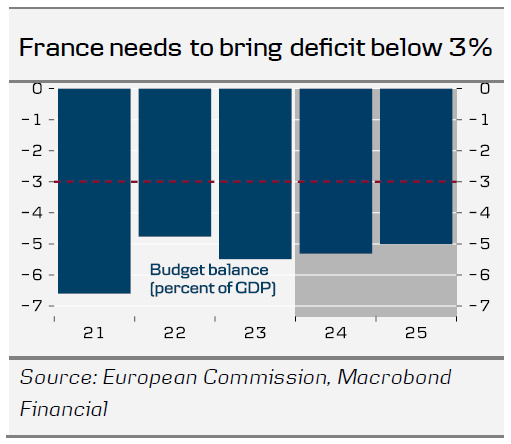

However, some uncertainty has been eliminated from markets by the results, as public spending in France is most likely not set to rise significantly since both the left-wing and far-right fell short of an absolute majority. A possible majority government in a coalition including Ensemble necessitates compromises and favours status quo given the different views on fiscal policies the parties in a broad coalition will have. The same would be true for a minority government. A technocratic government would likely neither be able to implement large changes, as it needs broad support. We thus expect the 10y yield spread between France and Germany will tighten to some 40-60 bp within 3 months.

In the coming days, a key question is whether the left-wing “New Popular Front” (NPF) coalition holds or breaks up. As the NPF fell short of an absolute majority, the most moderate parties (Socialists, Greens, and Communists) could potentially break with the far-left “France Unbowed” and form a government with Macron’s centrist alliance. This would keep “France Unbowed” and their leader, Melancon out of power as he has refused to government with Macron’s alliance, which is import for markets. However, even such a coalition would fall short of an absolute majority by around 10 seats. Importantly for markets is also, that it looks unlikely that Le Pen’s far right National Rally will be part of a new government. Another possible scenario is thus a minority government, but it will be in constant thread of no-confidence votes. A minority government will be even weaker than Macron’s Ensemble that had 250 seats in the outgoing National Assembly and even they struggled to pass new legislation. Hence, France is set for a prolonged period of political paralysis.

The new government will face pressures from the EU on public finances…

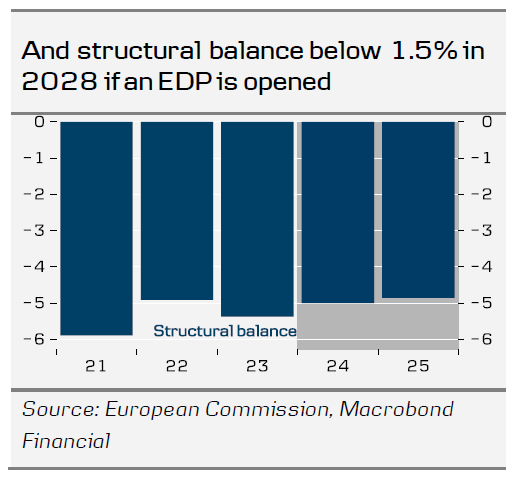

Given the weak public finances in France, the European Commission has officially proposed to open an excessive deficit procedure (EDP) against France together with six other EU countries. The EDP can ultimately result in fines to France of up to 0.05% of GDP to be paid every six months, up to cumulative fines of 0.5% of GDP (EUR 14bn in 2024). Currently it is premature to talk about fines as there is a long political process before it could be actual. The next step is that the new French government will submit budgets and reform proposals on how to correct the deficit in September. If a new government is not formed quickly, the Commission can grant France more time. Then, the Commission will decide whether to officially open an EDP against France. Given the fragmentation in the National Assembly and the fact that a new government will likely be fragile, we expect that it will be difficult for France to come up with structural reforms and spending cuts that can satisfy the commission. Hence, there is a significant chance of the Commission officially opening an EDP against France. Yet, it depends on the new government especially as a technocratic government might have a greater chance of making the unpopular decisions.

… that likely requires fiscal tightening of 0.50% per year.

If the Commission opens an excessive deficit procedure against France, we estimate that the new government will have to show an increase in the structural balance, of around 0.5 percentage points per year. This will be the case if France is granted the 7- year adjustment period while the four-year adjustment period would require an improvement of 0.9 percentage points per year. Given its size and power in the European Council France could most likely negotiate a seven-year adjustment period by committing to investments in EU priorities like the green transition and digitalisation. However, in either of the cases there is no room for much spending.