.){kind=link}

- Initial projections, alongside statements from Macron and Melenchon on Sunday, indicate that the most probable outcome is that no party will achieve an absolute majority, resulting in a ‘hung parliament’. Hence, public spending in France is not set to rise significantly (see scenario 1, page 2).

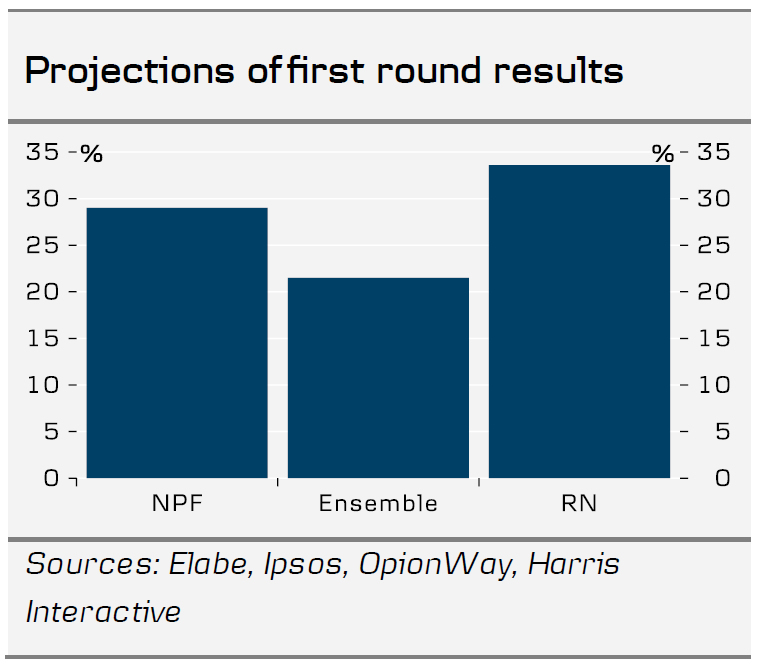

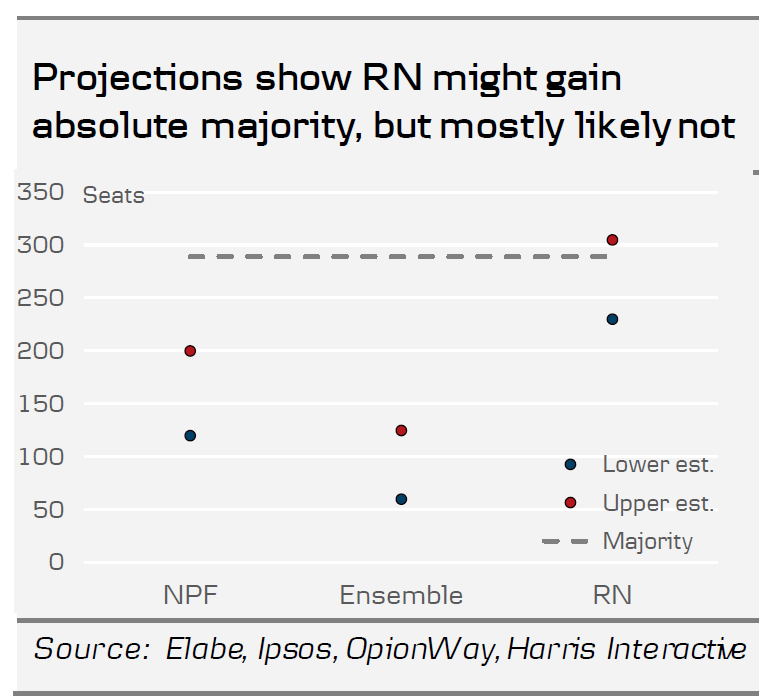

- Projections indicate that National Rally (RN) won the first round with around 33.5% of the votes, which translates to 230-305 seats in the National Assembly. A party needs 289 to gain an absolute majority. The left-wing New Popular Front (NPF) came second with around 28.9% (120-200 seats) and Macron’s centrist alliance (Ensemble) third with around 21.4% (60-125 seats). The final result is determined on Sunday 7 July.

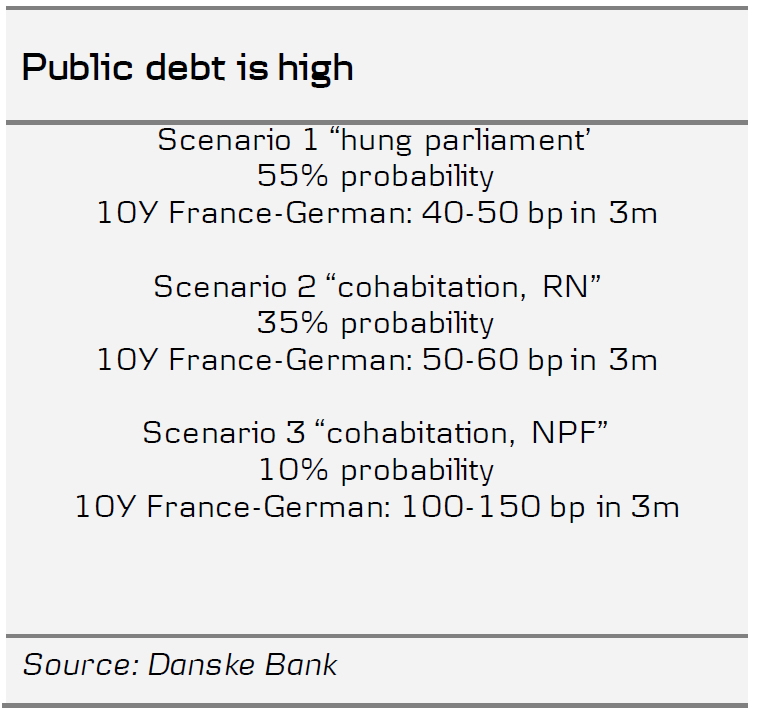

- The most likely scenario (55% probability) is a ‘hung parliament’ in the National Assembly after the second round. In this main scenario, we thus expect the 10y yield spread between France and Germany to tighten by some 30bp to 40-60 bp within 3 months as fears over spending increases fade.

- Due to record-high voter turnout, approximately 300 constituencies will have three candidates in the final round. However, both Macron and left-wing leader Melenchon have pledged to withdraw candidates within the next 48 hours to defeat the RN.

- In the “cohabitation” scenario (35% probability) where Le Pen’s party, Rassemblement National (RN), wins an absolute majority and Jordan Bardella becomes the next prime minister, we also expect the 10y yield spread between France and Germany to tighten, albeit to a less extend and trade between 50-60 bp within 3 months.

The first round of the election makes ‘hung parliament’ most likely

Initial projections, alongside statements from Macron and Melenchon on Sunday, indicate that the most probable outcome is that no party will achieve an absolute majority, resulting in a ‘hung parliament’. Hence, public spending in France is not set to rise significantly (see scenario 1, page 2). The second most likely scenario is an absolute majority for the National Rally, especially if third candidates from the NPF and Ensemble do not withdraw as previously stated. Notably for the markets, the scenario where the left-wing NPF secures an absolute majority is considered the least likely, so the worst fears of spending increases should fade.

The most updated projections from four pollsters’ show that the National Rally (RN) won the first round with around 33.5% of the votes, which translates to 230-305 seats in the National Assembly. Gaining an absolute majority requires a party to secure 289 seats, and while it is uncertain if National Rally (RN) has achieved this, it appears most likely that they have not. The left-wing New Popular Front (NPF) came second with around 28.9% (120-200 seats) and Macron’s centrist alliance (Ensemble) third with around 21.4% (60-125 seats). The projection is not the actual result of the first-round, but it indicates that RN had a slightly worse result than polls suggested and Ensemble and NPF a slightly better result.

In the second round on Sunday, July 7, there will be runoffs between the two candidates who received the most votes along with any third or fourth candidate who garnered more than 12.5% of all eligible votes. Due to the record high voter turnout, it is estimated that around 300 constituencies will feature three candidates. This situation presents a clear advantage for the National Rally, as votes will be split between the centre and the left. However, the left-wing NPF leader, Melenchon, has encouraged all third-placed candidates from his group to withdraw in an effort to unite against the sRN along with Macron’s Ensemble. Macron himself has called for “a broad, clearly democratic and republican alliance for the second round.” He stated that they would withdraw candidates where they placed third to support those who uphold “the values of the republic” in defeating the National Rally. Candidates now have 48 hours to withdraw in what promises to be a period of intense negotiations that is crucial to monitor.

Three scenarios for the second-round result and their impact on markets

The most likely scenario (scenario 1, probability: 55%) is a ‘hung parliament’ where no group or party obtains an absolute majority in the National Assembly. In this scenario, the new government will need to seek ad-hoc support for legislation, necessitating compromise. Given the division in the French parliament we find it unlikely that the new government can find support for any larger increases in spending. As the government needs to use the so-called article 49.3 to pass legislation (including the budget) through without a majority, we find large changes in policies unlikely as it then requires that the government survives a “no confidence” vote. Consequently, we should expect a status quo in France and its public finances. In this main scenario, we thus expect the 10y yield spread between France and Germany will tighten to 40-50 bp within 3 months as fears over spending increases fade.

In the “cohabitation” scenario (scenario 2, probability 35%) where Le Pen’s party, National Rally (RN), wins an absolute majority and Jordan Bardella becomes the next prime minister, we expect only a gradual implementation of the party programme and no large immediate increases in public spending. This is supported by the fact that RN has rolled back the costliest initiatives from the previous campaign. Bardella, who is the prime minister candidate has particularly softened his rhetoric’s on EU and public spending and in a recent FT interview Bardella said that “I do not intend to go to war with Brussels” and that the EU fiscal rules of a maximum deficit of 3% of GDP “remains an objective” and that “it will require me to prioritise”. Moreover, Bardella said he will undertake an audit of French public finances before deciding on spending priorities in the autumn. However, we note that his first priority will be to cut the VAT on energy and petrol, which will cost EUR12bn a year (0.4% of GDP) which he intends to fund this by raising various taxes, cutting tax loopholes and the France’s contribution to the EU budget. Yet, we assess that ambitions of turning the fiscal policy substantially more expansionary will be dampened by the risk of exclusion from EU/ECB support programmes or possible punishment in financial markets. Hence, in the scenario where Le Pen’s party wins an absolute majority, we also expect the 10y yield spread between France and Germany to tighten to 50-60 bp within 3 months.

In the third scenario, also a “cohabitation” situation, the left-wing New Popular Front (NPF) coalition secures an absolute majority (scenario 3, probability: 10%). Here, we anticipate an increase in public spending and potential confrontations with the EU. Unlike Bardella and RN, the left-wing alliance has maintained a firm stance in its communications recently. They want to increase spending by some €EUR150bn (5% of GDP) by 2026-2027, lower the pension age from 64 to 60, and at the same time increase taxes similarly in order not to increase the deficit. However, as details on funding are sparse and the risk of anti-establishment increases, we expect the immediate reaction in this scenario will likely be a significant increase in the spread between France and Germany to 100-150 bp within 3 months. Whether the government then will be able to work together in such a scenario is very uncertain though as the NPF coalition consists of four very different parties with contrasting views on topics such as Russia and Israel. Especially, it is important to note, that the left-wing coalition includes a more modest party like the socialist party with former president François Hollande, and we do not think they would tolerate market turmoil going this badly for a prolonged period, as they would lose all credibility of them being fit to govern in the future.