{kind=link}

Summary

- As expected, the Federal Open Market Committee left the federal funds rate target range unchanged at 5.25-5.50% at the conclusion of its meeting today. Yet the latest Summary of Economic Projections showed most participants continue to expect at least some reduction in the fed funds rate before the year is out.

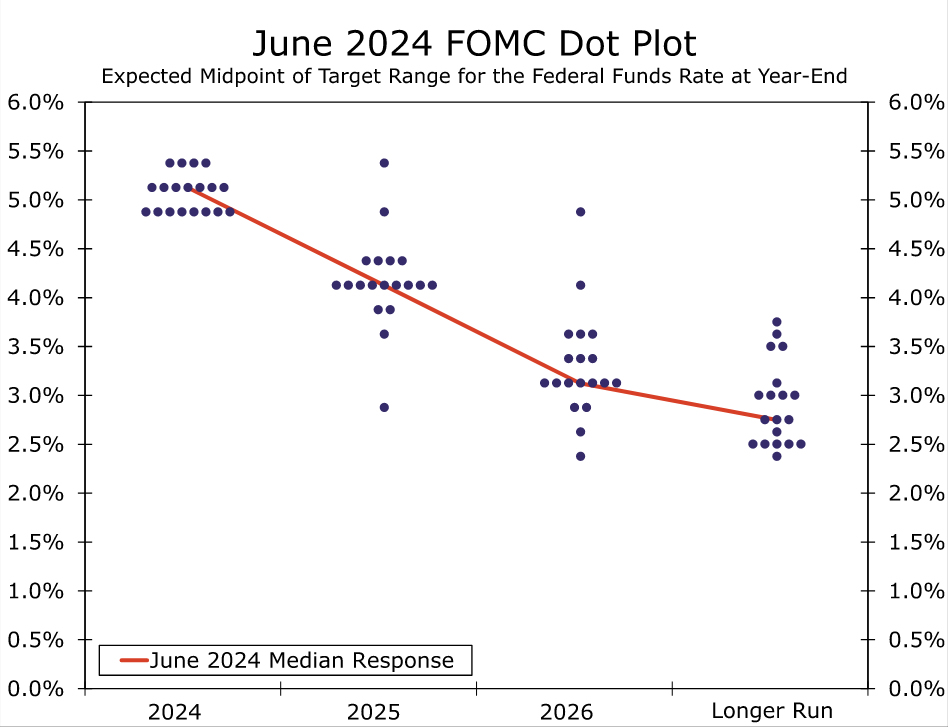

- The median projection for the fed funds rate at year-end was raised to 5.125% from 4.625% in the March SEP, implying only one 25 bps cut before the year. However, the distribution of projections skewed toward more easing, with eight participants expecting two cuts and only four expecting rates to remain unchanged. Participants now see 100 bps of easing over 2025 compared to 75 bps in the prior SEP, which would leave the fed funds target at 4.125%.

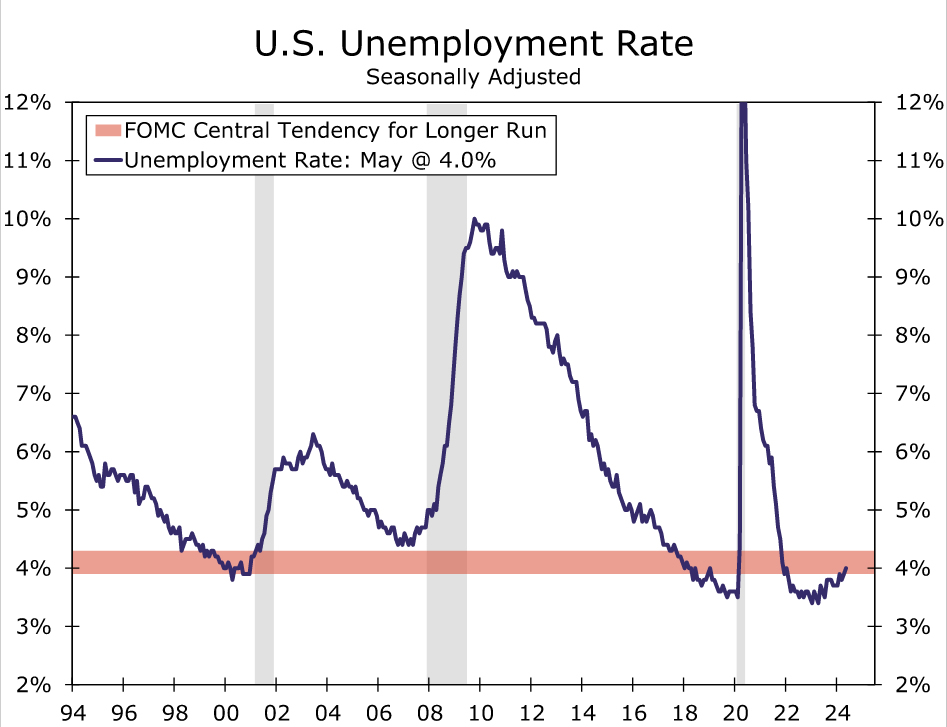

- The delayed start to rate cuts comes as inflation has been stickier this year while economic activity remains “solid.” Participants now see core PCE inflation up 2.8% on a Q4/Q4 basis compared to 2.6% in the March SEP, but GDP growth unchanged at 2.1%—above the Committee’s median estimate of potential—and the unemployment rate holding at its current rate of 4.0%.

- Changes to the post-meeting statement were minimal. The Committee gave a nod to the somewhat better run of inflation data since its May 1 meeting by noting that there has been some “modest further progress” on the inflation front instead of a “lack of further progress.” But, the statement reiterated that inflation remains “elevated” and the FOMC is “strongly committed” to its 2% inflation objective.

- While the May CPI report released earlier today was encouraging for the inflation outlook, the FOMC clearly needs to see more benign prints before a consensus emerges that a reduction in the fed funds rate is warranted. With few signs of that consensus emerging yet, we continue to believe that the earliest the FOMC would reduce the fed funds rate would be at its September 18 meeting, when it will have three more months of inflation and employment data in hand.

- It will be a close call between one or two 25 bps rate cuts, and the Committee seems evenly split between the two outcomes. Our base case forecast since early April has looked for a 25 bps rate cut at each of the September and December FOMC meetings. For now, our forecast remains two cuts this year and another 100 bps of easing in 2025. We will publish our standard monthly economic forecast update on Friday morning.

FOMC Still Playing the Waiting Game

As was universally expected, the Federal Open Market Committee voted unanimously to keep the target range for the fed funds rate unchanged at 5.25-5.50% at the conclusion of its meeting today. With inflation remaining elevated and economic growth still sturdy, the Committee has now held the fed funds rate steady for seven consecutive meetings. Yet an update to the Summary of Economic Projections (SEP) showed that most FOMC participants continue to expect at least some reduction in the fed funds target before the year is out.

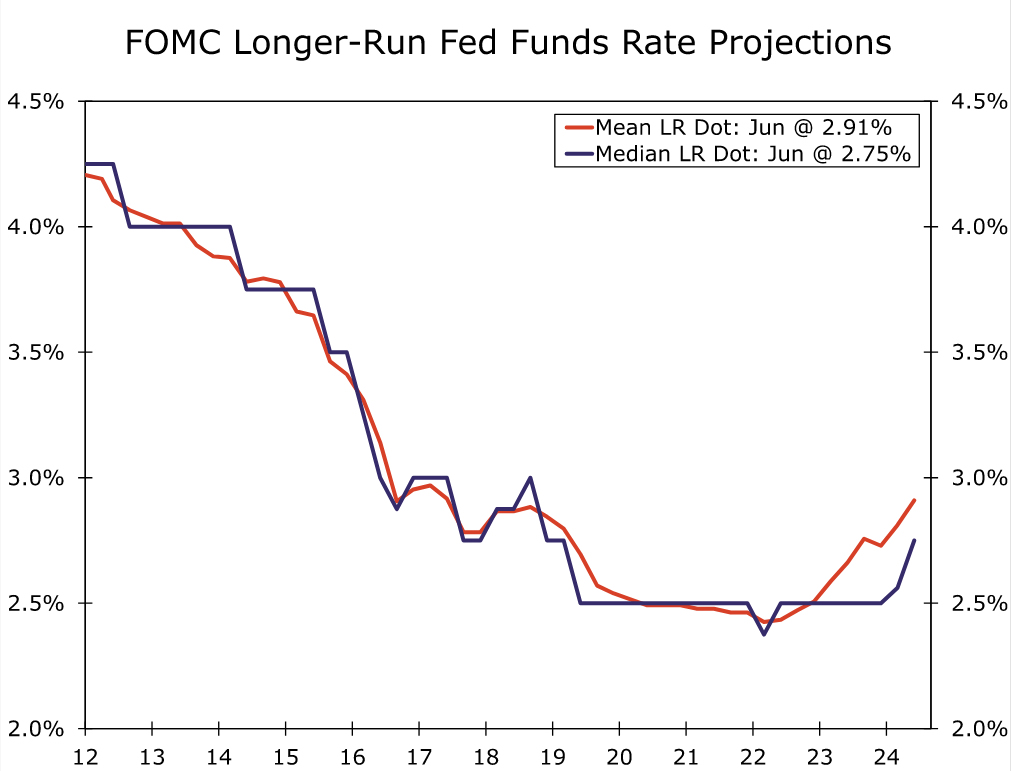

The median Committee participant penciled in one 25 bps rate cut by year-end, down from 75 bps projected in the March SEP. The distribution of the 2024 dots had a clear downward bias. Eight participants anticipated 50 bps of easing by year-end, while just four participants expected the fed funds rate to be unchanged through the end of this year (Figure 1). No participants projected the fed funds rate would rise later this year. Looking to 2025, the median dot is 4.125%, which if realized would be 100 bps of easing in addition to the 25 bps expected this year. The median longer-run dot continued to tick higher, climbing to 2.75%, the highest reading since March 2019 (Figure 2).

Elsewhere, there were few notable changes in the SEP. The median projections for real GDP growth were completely unchanged, while the median projections for the unemployment rate ticked higher by a tenth in 2025 and 2026 in what was likely a nod to the gradual upward trend in the unemployment rate (Figure 3). Headline and core PCE inflation projections were higher by two tenths in 2024 and one tenth in 2025, in line with our expectations headed into the meeting. Participants had the opportunity to adjust their projections in light of this morning’s CPI report, although they did not have to make changes, and some may have elected not to given that the May data for the PCE deflator remain uncertain. Powell shared in the press conference that “most” officials do not update SEP submissions on days like this.

Back in December, the median Committee member was expecting 2.4% core PCE inflation and 75 bps of rate cuts in 2024. Today’s projections look for 2.8% core PCE inflation this year and just 25 bps of cuts. The downward trend in inflation remains in place, but the bumpy path and slow-going and have led the FOMC to be more patient at this stage of the cycle.

There was only one material change to the post-meeting statement. The statement now gives a nod to the somewhat improved inflation picture since the Committee’s May 1 meeting. Instead of noting that there has been a “lack of further progress” toward the Committee’s 2% inflation goal, the FOMC recognized “modest further progress” in lowering inflation. Other than that, the only other change in the statement was the removal of the Committee’s announcement to slow the pace of quantitative tightening, a process that began on June 1.

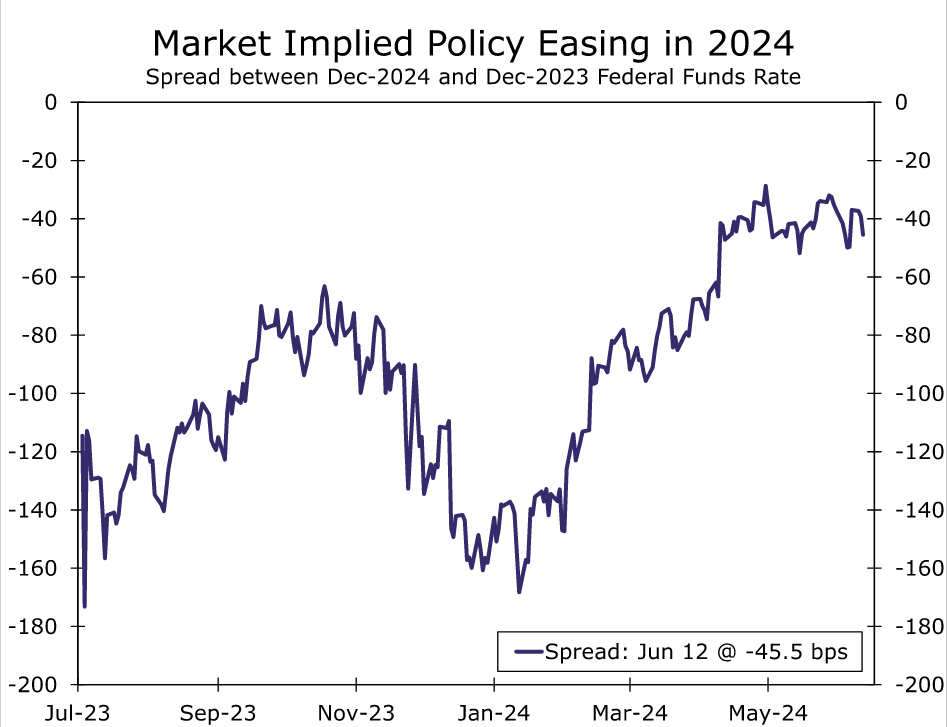

On balance, we remain confident that the FOMC will begin reducing the federal funds rate before the year is out. As we wrote in response to this morning’s CPI report, we see inflation pressures continuing to subside as the year progresses. It will be a close call between one or two 25 bps rate cuts, and the Committee seems evenly split between the two outcomes. Financial market pricing also suggests a clear openness to more than one cut this year (Figure 4). Our base case forecast since early April has looked for a 25 bps rate cuts at each of the September and December FOMC meetings. For now, our forecast remains two cuts this year and another 100 bps of easing in 2025. We will publish our standard monthly economic forecast update on Friday morning.