{kind=link}

Dollar trades broadly higher today as sentiments are supported by hope on tax cuts in US. In particular, EUR/USD breaks 1.1574 support to resume recent decline from 1.2091 high. Nonetheless, commodity currencies are trading as the weakest ones. In particular, Aussie is under some pressure after the non-eventful RBA rate decision. Economic calendar is lightly today and the main focuses for the rest of the day will be on speeches by BoC Governor Stephen Poloz and Fed Chair Janet Yellen.

ECB Lautenschlaeger wants to see clear stimulus exit

ECB Executive Board Member Sabine Lautenschlaeger said there is a "strong growth momentum" in the Eurozone. And the region has grown for "17 consecutive quarters" while "the labor market has a solid recovery, sentiment factors are positive, the financial conditions for firms and households are very favorable." And she is "very confident that inflation rate will pick up". Therefore, ECB’s decision to half monthly asset purchase to EUR 30b starting January was "correct". And she added that "I would have liked to see a clear exit".

Separately, ECB President Mario Draghi urged a join efforts by "banks, supervisors, regulators and national authorities" to address non-performing loans. He called that the "most important issue" at a conference. ECB’s plan to adopt tougher measures on non-performing loans by Eurozone financial institutions was endorsed by Eurogroup head Jeroen Dijsselbloem. However, it’s criticized by European Banking Federation Chief Executive Wim Mijs as having "ill-defined scope". And, Mijs said " the stricter requirements put European banks with exposure in (the) non-euro zone area at a competitive disadvantage vis-a-vis local banks."

Released from Eurozone, retail sales rose 0.7% mom in September, retail PMI dropped to 51.1 in October. German industrial production dropped -1.6% mom in September. Separately, Swiss Foreign currency reserves rose to CHF 742b in October, up from CHF 724b. That’s also the highest level on record.

UK Halifax: BoE hike wont’ be barrier to house purchase

In UK, Halifax house price rose 4.5% yoy in the August-October quarter, accelerated from 4.0% in the quarter to September. That was in line with market expectation. Halifax noted that "increasing pressure on household finances and continuing affordability concerns are some of the factors likely to dampen buyer demand". However, the increase in BoE’s Based Rate will not result in "a barrier to buying a house".

Also from UK, BRC retail sales monitor dropped -10% yoy in October.

China foreign exchange reserves rose for 9 straight months

In China, foreign exchange reserves rose USD 7.03b to USD 3.1092T. That followed a again of USD 16.98b back in September. The rise in reserves in September was below market expectation of USD 9.5b. Nonetheless, that’s the ninth consecutive month of growth, first since June 2014. Meanwhile, value of gold reserves dropped to USD 75.248b, down from September’s USD 76.005b.

RBA stands pat, likely to stay on hold ahead

As widely anticipated, RBA left the cash rate unchanged at 1.5% today. As we await Friday’ Statement of Monetary Policy, policymakers revealed at the statement that the macroeconomic guidance has stayed largely unchanged. In short, policymakers remained upbeat about the growth outlook, although they expressed concerns over household spending and soft inflation.

Despite recent weakness in the Australian dollar, RBA reiterated the warning that higher exchange rate would lead to slower growth and inflation. Given the overall unchanged tone of the central bank, we retain the view that RBA would keep the policy rate unchanged at least until 1H18.

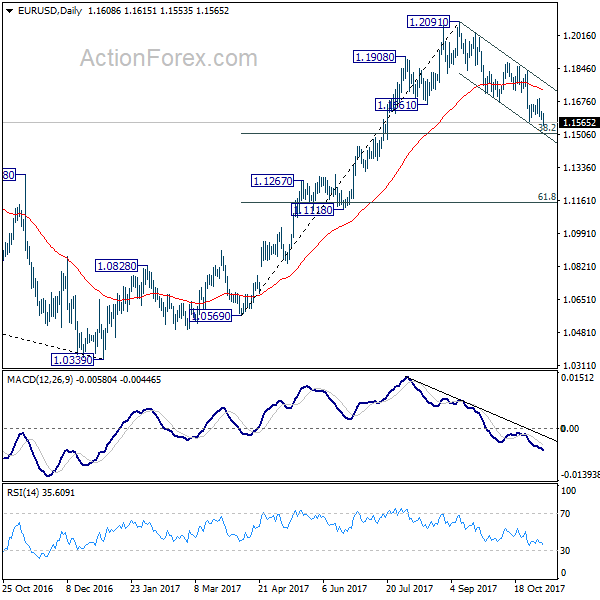

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1585; (P) 1.1604 (R1) 1.1629; More…

EUR/USD’s break of 1.1574 indicates that recent decline from 1.2091 has resumed. Intraday bias is back on the downside for 38.2% retracement of 1.0569 to 1.2091 at 1.1510. We’d be cautious on strong support from there to bring rebound. But sustained break of 1.1510 will pave the way to next support zone at 1.1118/1267. On the upside, break of 1.1689 resistance is needed to confirm short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we’d be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | JPY | Labor Cash Earnings Y/Y Sep | 0.90% | 0.50% | 0.90% | 0.70% |

| 0:01 | GBP | BRC Retail Sales Monitor Y/Y Oct | -1.00% | 0.90% | 1.90% | |

| 3:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 7:00 | EUR | German Industrial Production M/M Sep | -1.60% | -0.80% | 2.60% | |

| 8:00 | CHF | Foreign Currency Reserves (CHF) Oct | 742B | 724B | ||

| 9:10 | EUR | Eurozone Retail PMI Oct | 51.1 | 52.3 | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Sep | 0.70% | 0.60% | -0.50% | -0.10% |