{kind=link}

As US session commences, Swiss Franc and Japanese Yen are trading as the day’s strongest currencies, fueled by risk aversion in US markets. While major European indices exhibit only modest fluctuations, US futures indicate notably lower opens, reinforcing the cautious sentiment among investors.

Swiss Franc’s additional strength can be traced to comments made by outgoing SNB Chairman Thomas Jordan overnight, who pointed to its depreciation as a catalyst for unexpected inflationary pressures in Switzerland. In response, Jordan highlighted the possibility of the SNB intervening in the currency market by selling foreign currencies to stabilize the Franc.

Contrary to typical market behavior during periods of uncertainty, Dollar is underperforming, marked as the weakest performer of the day. Nevertheless, it’s still maintaining its ground above last week’s lows against most counterparts—excluding Swiss Franc. There is no significant momentum suggesting an imminent breakthrough. Dollar’s next decisive move may hinge on the forthcoming US PCE data tomorrow.

Elsewhere in the currency markets, New Zealand Dollar trails behind Dollar as the second weakest, followed by Canadian Dollar. Australian Dollar ranks as the third strongest. The Euro and British Pound are positioned in the middle.

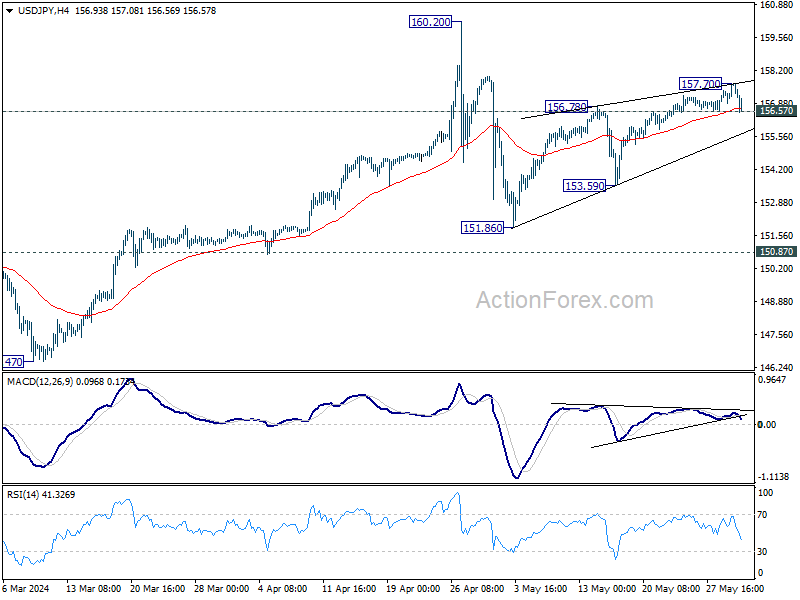

Technically, immediate focus on 156.57 minor support in USD/JPY. Decisive break there should confirm short term topping at 157.70. More important, that will argue that rebound from 151.86 has completed with three waves up to 157.70. Fall from there could then be developing into the third leg of the corrective pattern from 160.20. In this, case deeper decline would be seen to 153.59 support next.

In Europe, at the time of writing, FTSE is up 0.36%. DAX is up 0.15%. CAC is up 0.35%. UK 10-year yield is down -0.0394 at 4.371. Germany 10-year yield is down -0.017 at 2.676. Earlier in Asia, Nikkei fell -1.30%. Hong Kong HSI fell -1.34%. China Shanghai SSE fell -0.62% Singapore Strait Times rose 0.01%. Japan 10-year JGB yield fell -0.0206 to 1.060.

US initial jobless claims rises to 219k, slightly above expectation

US initial jobless claims rose 3k to 219k in the week ending May 25, slightly above expectation of 218k. Four-week moving average of initial claims rose 2.5k to 222.5k.

Continuing claims rose 4k to 1791k in the week ending May 18. Four-week moving average of continuing claims rose 6k to 1786k.

Eurozone economic sentiment rises to 96, EU up to 96.5

Eurozone Economic Sentiment Indicator ticked up from 95.6 to 96.0 in May, matched expectations. Employment Expectations Indicator fell -0.3 pts to 101.3. EU ESI rose 0.3 pts to 0.6.5. EU EEI fell -0.4 to 101.2.

For the largest EU economies, the ESI improved significantly for France (+1.5) and the Netherlands (+1.1) and more moderately for Germany (+0.8) and Italy (+0.8), while it deteriorated markedly for Spain (-3.2) and Poland (-1.5).

Eurozone unemployment rate falls to 6.4%, EU steady at 6.0%

Eurozone unemployment rate fell from 6.5% to 6.4% in April, below expectation of 6.5%. EU unemployment rate was unchanged at 6.0%.

Eurostat estimates that 13.149 million persons in the EU, of whom 10.998 million in Eurozone, were unemployed in April 2024.

Swiss GDP grows 0.3% in Q1, services sector Leads

Switzerland’s GDP, adjusted for sporting events, grew by 0.3% qoq in Q1, meeting expectations.

The industrial sector’s overall value added stagnated. Manufacturing declined slightly by -0.2%, and chemical and pharmaceutical industries fell by -0.9%. Construction industry grew modestly by 0.3%, while energy sector saw solid growth of 2.1%.

Services sector drove GDP growth despite uneven performance. Financial services declined by -0.2%, and business-related services contracted by -0.3%. Transport and communication sector was flat.

However, accommodation and food services sector grew by 1.3%, health and social care services increased by 0.8%, and public administration rose by 0.2%. Retail sector grew strongly by 1.4%, leading to a 1.3% overall increase in trade.

Swiss KOF falls to 100.3, signals modest economic momentum

Swiss KOF Economic Barometer fell from 101.9 to 100.3 in May, falling short of expectations of 102.2. This year, the barometer has managed to stay only slightly above its medium-term average. KOF noted, “Although the Swiss economy is robust, it is not showing much vigour beyond that.”

Indicators for manufacturing, financial and insurance services, and foreign demand all slowed down after positive developments in the previous month. However, indicators for private consumption and the construction industry helped cushion the decline with increases.

RBA’s Hunter cautious on persistent inflation despite wage trends

At a conference today, RBA Chief Economist Sarah Hunter highlighted the central bank’s intense focus on inflation, which continues to exceed the target band.

Discussing the latest CPI data, Hunter noted, “Yesterday’s data did confirm that there’s still strength in a number of categories that we’ve seen up until this point that’s still there.” The latest CPI figures, which show a slight increase from 3.5% to 3.6% in April, underline ongoing inflationary pressures across various sectors.

“So clearly there’s still some strength in inflation, and that’s a key consideration for the board in their decision-making,” Hunter added.

While wage growth appears to have peaked, Hunter expressed concerns about productivity which remains weak: “We can see some components of wages growth coming off already, particularly individual agreements,” she said. However, she also pointed out, “But equally, we are seeing that there’s a bit of a productivity challenge over the last few years.”

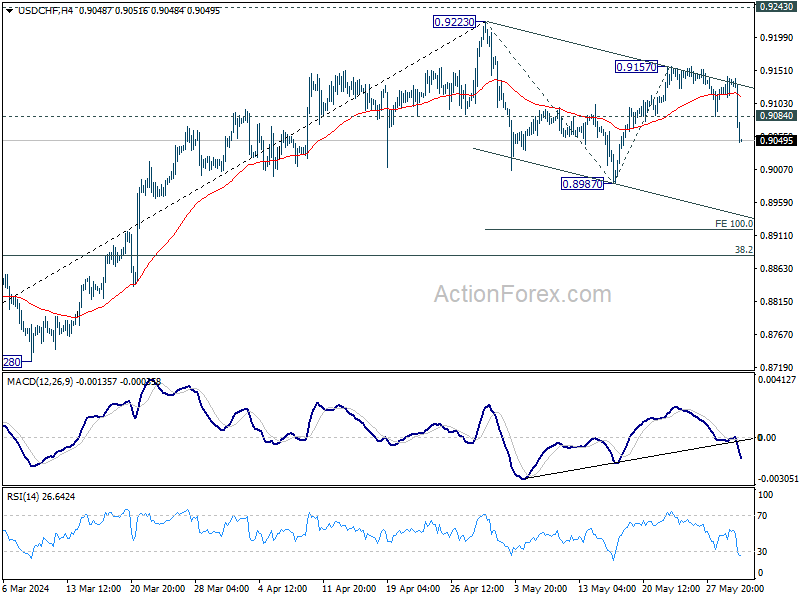

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9116; (P) 0.9130; (R1) 0.9147; More….

USD/CHF’s fall from 0.9157 accelerates lower today, and the development suggests that rebound from 0.8987 has completed already. Fall from 0.9157 is now seen as the third leg of the pattern from 0.9223. Intraday bias is back on the downside for 0.8987 support first. Break will target 100% projection of 0.9223 to 0.8987 from 0.9157 at 0.8921. On the upside, above 0.8904 minor resistance will turn intraday bias neutral first.

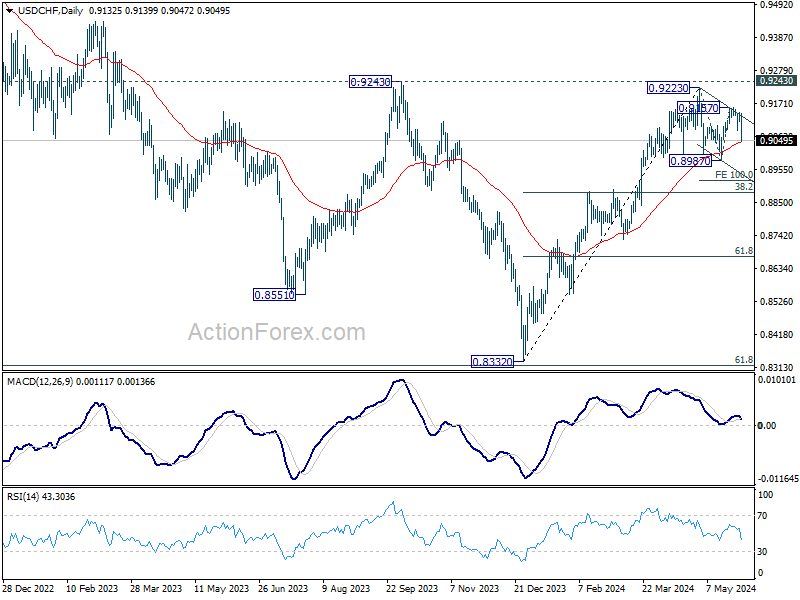

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Apr | -1.90% | -0.20% | ||

| 01:30 | AUD | Private Capital Expenditure Q1 | 1.00% | 0.60% | 0.80% | |

| 06:00 | CHF | Trade Balance (CHF) Apr | 4.32B | 3.98B | 3.54B | 3.77B |

| 07:00 | CHF | KOF Economic Barometer May | 100.3 | 102.2 | 101.8 | 101.9 |

| 07:00 | CHF | GDP Q/Q Q1 | 0.30% | 0.30% | 0.30% | |

| 08:00 | EUR | Italy Unemployment Apr | 6.90% | 7.30% | 7.20% | 7.10% |

| 09:00 | EUR | Eurozone Unemployment Rate Apr | 6.40% | 6.50% | 6.50% | |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator May | 96 | 96 | 95.6 | |

| 09:00 | EUR | Eurozone Industrial Confidence May | -9.9 | -9.4 | -10.5 | -10.4 |

| 09:00 | EUR | Eurozone Services Sentiment May | 6.5 | 6.5 | 6 | 6.1 |

| 09:00 | EUR | Eurozone Consumer Confidence May F | -14.3 | -14.3 | -14.3 | |

| 12:30 | CAD | Current Account (CAD) Q1 | -5.4B | -5.5B | -1.6B | -4.5B |

| 12:30 | USD | Initial Jobless Claims (May 24) | 219K | 218K | 215K | 216K |

| 12:30 | USD | GDP Annualized Q1 P | 1.30% | 1.50% | 1.60% | |

| 12:30 | USD | GDP Price Index Q1 P | 3.00% | 3.10% | 3.10% | |

| 12:30 | USD | Goods Trade Balance (USD) Apr P | -99.4B | -91.8B | -91.8B | -92.3B |

| 12:30 | USD | Wholesale Inventories Apr P | 0.20% | -0.10% | -0.40% | |

| 14:00 | USD | Pending Home Sales M/M Apr | -0.60% | 3.40% | ||

| 14:30 | USD | Natural Gas Storage | 77B | 78B | ||

| 15:00 | USD | Crude Oil Inventories | -2.0M | 1.8M |